Some key take aways from AR 22

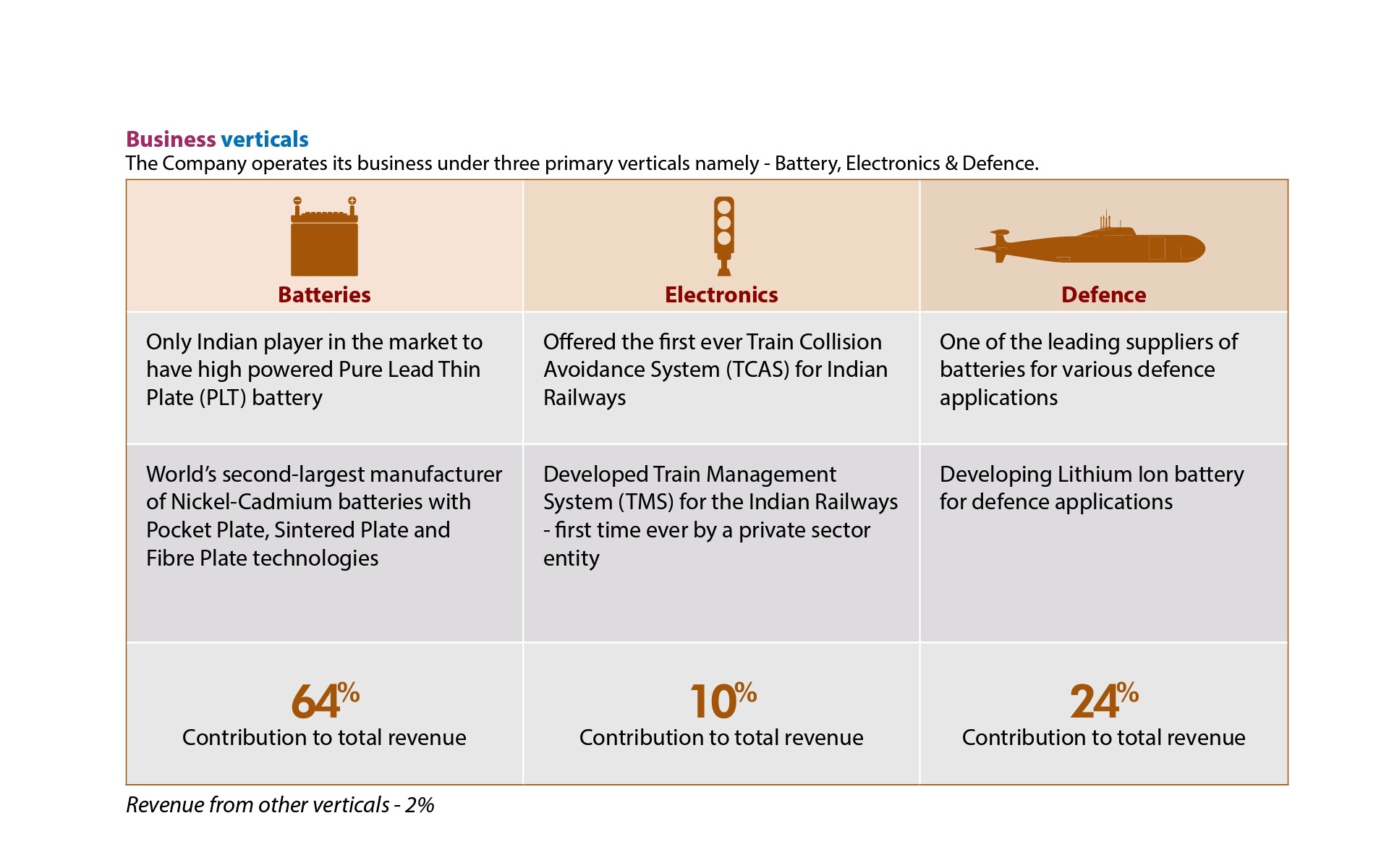

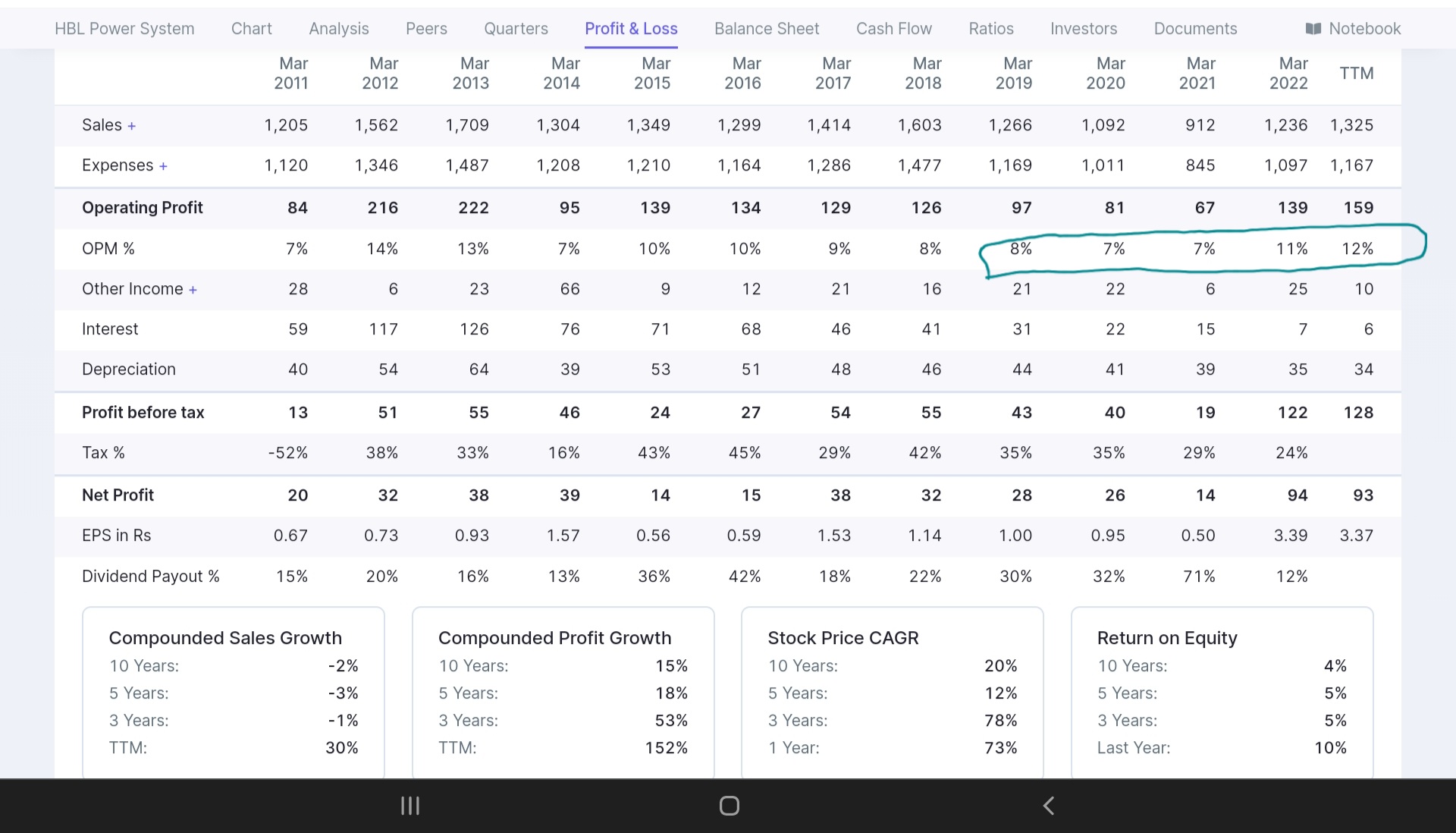

Its an improving product mix thus margins case( low margin battery majority to High margin electronics + defense + battery mix improvement , supported by end sector solid demand tailwind. Being debt free helps further.

Given FY 22 electronic was at 10% of revenue and defense at 24%, 120 cr type railways & 300 cr from defense and margins are nearing low/early teen with.

Looking at recent wins of 700cr+ from Railways ( TCAS + TMS and across corridors as well as Vande bharat coach factory) – 20%+ from railways share is possibile even if 1/3rd order book is executed this year. Defense commentary is strong as well. Together a meaningful higher contribution with growth trajectory, hopefully mgmt gives more details in AGM.

Technicals and newsflow on 700 cr+ Railways bid wins are supporting the case

Given Railways and defense are one of key growth areas and govt push is visible in recent times. Op margins are validation of improving mix.

Thanks @Anant for wonderful insights in thread, including key aspects of R&D success vs R&D conversion to commercial success attribute as key monitorable.

initial positions and studying

| Subscribe To Our Free Newsletter |