RHI Magnesita’s Annual Report this year gives considerable insights into the refractory sector in general and the company in particular. Some highlights are given below:

1. Industry outlook:

India’s crude steel production grew 18% y-o-y to 120.10 million ton during the year. World Steel Association expects India’s steel demand to rise 7.5% in CY 2022 followed by 6% in CY 2023. The growing steel industry, along with elevating infrastructure development, is augmenting the demand for refractory materials. The widespread adoption of unshaped refractories for several construction applications, as also growing popularity of refractories in sectors such as infrastructure, aerospace, automotive, medical, and electrical is anticipated to drive the market. Additionally, the high prevalence of recycling refractory materials for steel production is also augmenting market growth.

Refractory is a consumable and does not face commodity-like volatility. Historically, refractory companies have been steady revenue compounders with stable margins, net cash balance sheets and superior return ratios, a remarkable contrast to its customer steel sector, thereby largely obviating the severe cyclicity of commodity companies. New steel capacity worth ~38mn tonnes in the next 4 years will also drive additional demand for refractories. Strong export demand for Indian steel due to production curbs by China will further accelerate refractory demand. Historically, revenue growth of refractory players has been ~1.5 times of growth in steel production and therefore we expect at least 12% Compound Annual Growth Rate revenue growth for refractory manufacturers over FY 2021-24.

2. RHIM Business outlook:

The Company produces nearly 140,000 tons of refractory per annum including customized products. Other than this, RHIM imports significant value of refractory products which are used for full line service contracts in steel industries. The refractory products are mainly used in high temperature manufacturing processes in iron and steel industry, metal smelters, cement, glass industry and for other industrial products. The company gets support from its global market forecasting and supply chain management capabilities of the parent company. During the year, the company was able to pass on high raw material and freight costs to the customers and protect its margins.

3. Operations:

Company has three manufacturing facilities viz. Vizag, Bhiwadi (Rajasthan) and Cuttack.

Vizag: This facility is specialized in manufacturing of High Alumina products and pre-casts. It supplies to 84+ countries and has a capacity of 73,049 TPA. During the year, capacity was enhanced by 30%.

Bhiwadi: This facility is specialized in development and manufacturing of world-class Flow Control products. During the year, a world-class R&D centre has been operationalized at Bhiwadi. The centre works in close collaboration with RHI Magnesita global R&D network to provide faster localized support to customers in India and service the product development needs of their plants. Bhiwadi facility supplies to 84 countries and has annual capacity of 69,445 TPA

Cuttack: This facility is specialized in the production of Magnesia Carbon Bricks. It has a capacity of 18,000 TPA. Here capacity expansion is in progress and is expected to be completed over the next two years. Once completed, it will help in Chinese import substitution.

4. Future plans:

The company has set a strategic business goal of doubling the production capacity to 300,000 TPA and revenue by FY 2025-26 as compared to 2020-21. This will be achieved through organic and inorganic means. For this, a phased capex investment of Rs. 400 crores (upto 2025-26) for expanding capacities and automation has been earmarked. During the current year, the company started a number of projects at Bhiwadi and Vizag to make certain high-grade import substitute products like purge plugs, coke oven blocks, tap hole clay mass, etc. These are being done via technology transfer arrangements with European and American plants of the parent company. The company also brought two patented digital refractory solutions of RHI Magnesita global to India – Automatic Process Optimization technology (APO) and Electromagnetic Level Indication Platform (EMLI), which have been deployed at a major steel plant in the country.

5. Raw Materials

For sourcing of raw materials, the industry is highly dependent on China. In China, the key producer of magnesite is the Liaoning province. Production of magnesia there came under stress due to stricter environmental control, and the recent power cuts in the Liaoning province have aggravated the problem. Prices of 97% fused magnesia and white fused alumina, which is main raw material of refractory products has increased significantly.

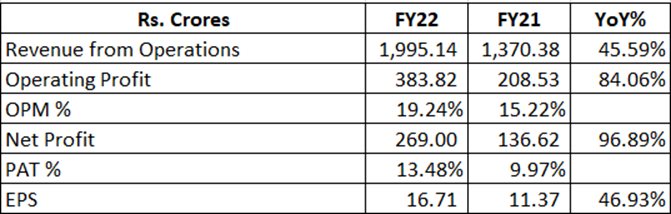

6. Accounts and Financials

Summarized financials are given below for the sake of completeness:

Not a full analysis but some exception points that I specifically noted are mentioned below.

-

During the year, merger with the unlisted subsidiaries got completed and the company has allotted 4,08,57,131 equity shares to the shareholders of its erstwhile fellow subsidiaries.

-

A large portion of revenue comes from what is called “Total Refractory Management Servies (TRMS”). Here revenue is recognized not on the basis of products sold but on the quantity of steel produced by the customer.

-

Geographical distribution of revenue – Within India is 84 % and Outside India 16 %

-

Revenue from traded goods was Rs.292 crore (28% of product sales) as against Rs.246 crores (33%) last year. (My comment: These are imports & sale of certain high-tech products from their parent which are not produced in India but demanded by their customers. I think these should go down over a period of time as more and more import substitution projects get completed as mentioned earlier.)

-

Sales to parent were Rs.262 crore and purchases from parent were Rs.381 crore. (My comment: Company is subject to Transfer Pricing norms, which is a very slippery area and prone to tax disputes and litigation – risk factor!)

-

Company used to be zero debt earlier. Now there is foreign currency debt of Rs.55 crores on the Balance Sheet, inherited from the unlisted subsidiaries. (My comment: Most of the debt is due Dec 2022, so the company can be expected to be debt free again)

-

During the year, addition to Gross Block was around Rs.67 crore on account of new capex done as mentioned earlier.

-

There are adverse remarks by the auditors around minor lapses and procedural matters which the company says have now been / or in the process of being rectified.

-

Company incurred a forex loss of Rs.5 crores during the year.

-

Royalty has gone up from Rs.1.30 crore in FY21 to Rs.8.18 crore in FY22.

Coupled with the investor presentation released earlier (see my previous post), the latest Annual Report gives a good idea of RHIM’s business in the country. Post the merger, the company seems to have become more investor friendly now.

(Disc: Invested.)

| Subscribe To Our Free Newsletter |