thank you everyone for input . i am also interested in buying this company .

thesis :-

1)its a TATA company

2)showing good growth in term of sales

3 )part of packaging industry specially in food segment which includes oil and canned food and non food like paint , sprays etc.

4 ) with growing consumerism chances of consumption of these items will increase so use of tinplate

5) there is almost none domestic competition , but there is risk of cheap Chinese competition if FSSAI give license to them

antithesis :-

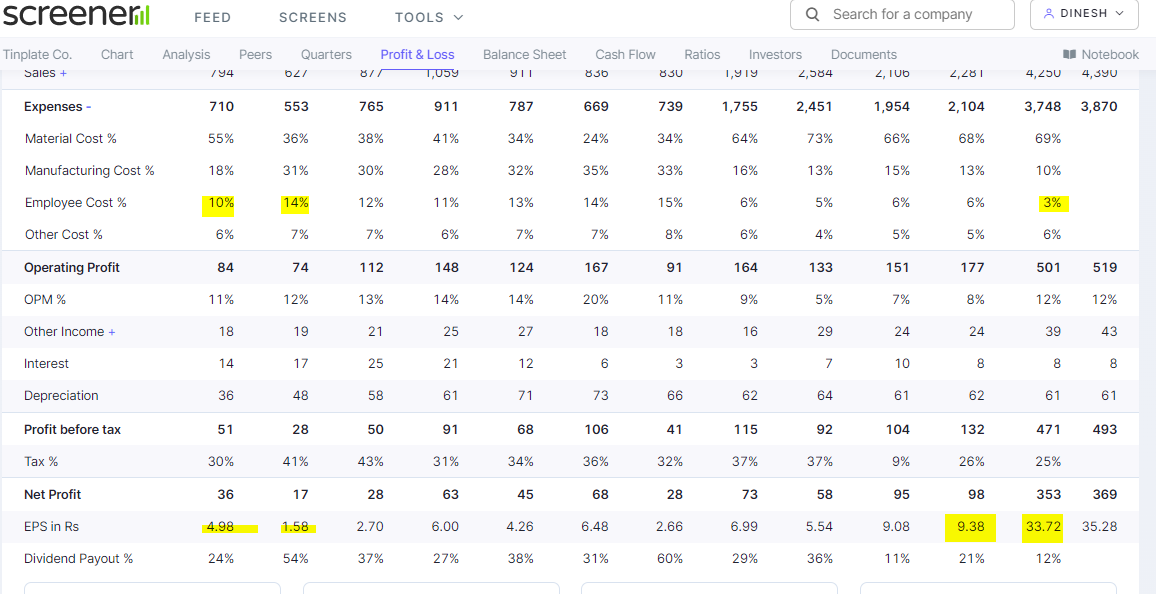

although this company makes product focused on consumer but there is wide fluctuation in EPS , for which it behaves like a cyclical company. it may be because of rise in input cost , but it again arise a suspicion why its not able to pass the input cost to its customer.

if anyone of you have this answer i will be obliged and will make a decision to buy some part of company

| Subscribe To Our Free Newsletter |