Market History

-

Windlas Biotech came out with its IPO in August 2021 at INR 460 per share/Market Cap ~1000 Cr. The IPO saw a good subscription response at that time at 22x

-

Since then, due to headwinds for Pharma, primarily normalisation of a COVID base in sales for Windlas, has led to a strong correction in stock price.

-

At CMP of 235, it quotes at 51% of the IPO price/market cap of 512 Cr currently. This means that the company is currently available for ~1.1x sales and sub 15 PE

-

Despite being a micro cap, the management has regularly held conference calls/share investor presentations since the IPO and offer good clarity on the business

Company Overview

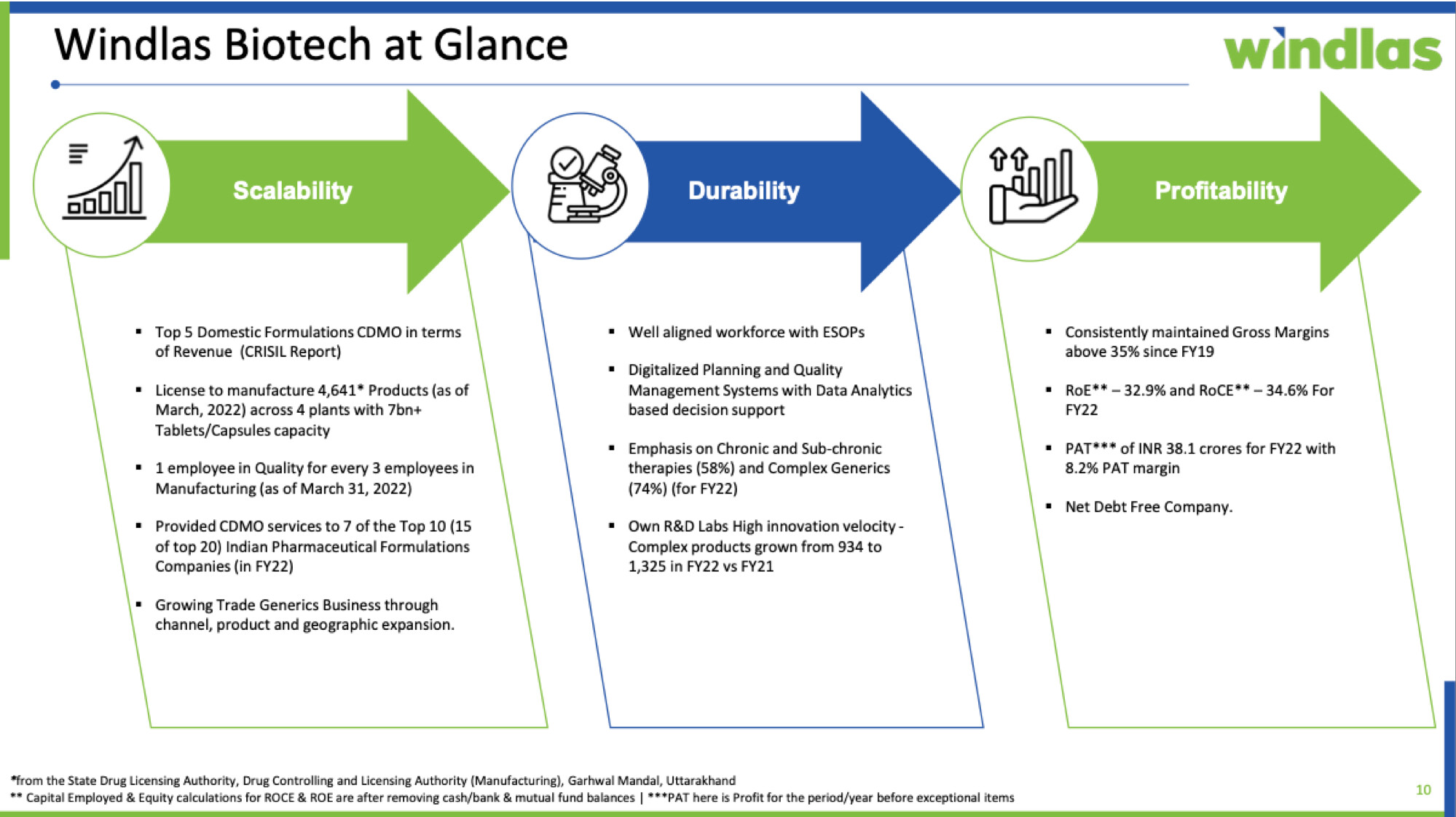

Here is a slide from the investor presentation which gives a decent company overview

-

Revenue Mix : As of Q1 FY23, Windlas has ~79% of revenues coming from its CDMO vertical. ~18% revenues come in from trade generics and they have just started exports (non USA markets only) which contribute ~2% of sales

-

They claim to be amongst the top 5 players in the domestic CDMO space, supplying to customers like Pfizer, Sanofi, Cadila, Emcure, Eris and Intas amongst others (from DRHP – Page 134). In the latest Q1 FY’23 investor presentation, they also claim to be in all aspects of the value chain including CRO and CDMO depending on the customer, except in API manufacturing (Slide 11)

-

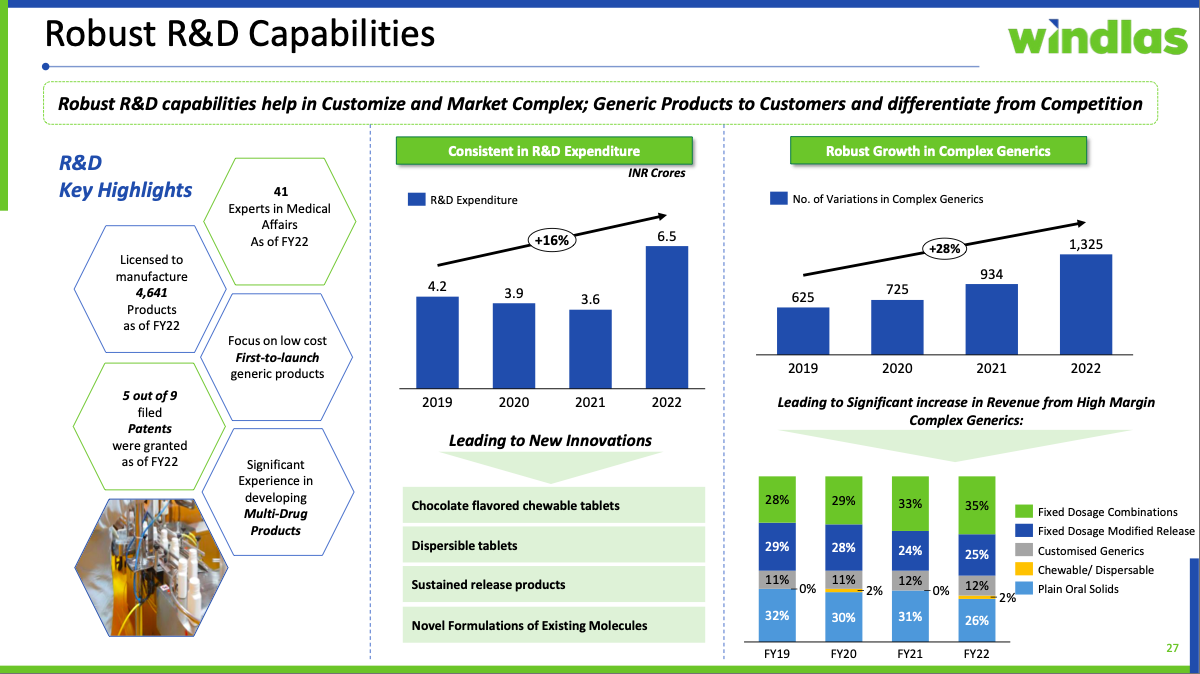

They claim to have a high product concentration in complex generics and from the chronic segment. The below slide mentions historical growth of CDMO business along with good growth in product offerings in the CDMO space coming from good R&D capability

- Margin Mix : The company in different concalls claims to work on a cost plus model and hence not be largely positively/negatively affected by input prices/industry pricing interventions. Margin profile (GM ~36%, OPM ~11%) suggests a more manufacturing oriented CDMO model rather than a higher margin one based on IP/research. Interestingly, forays into the faster growing verticals of trade generics and international business are margin accreditive over the CDMO business, as can be seen from concall snippet below. These could be potential sources of margin expansion over the long term from current base apart from an upcoming foray into injectables.

Manufacturing Footprint and Potential for Operating Leverage

-

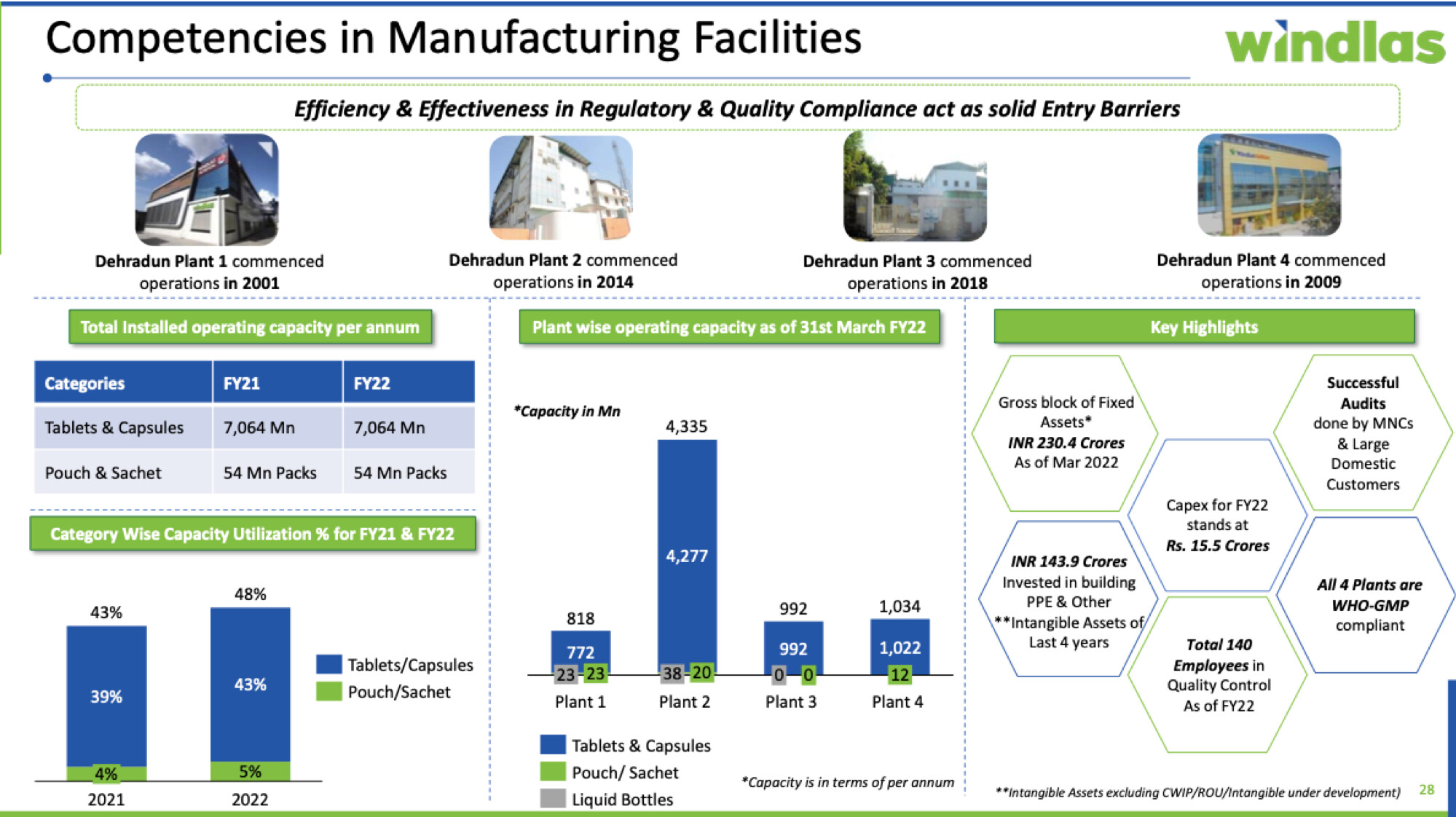

Below slides from investor presentation give a good insight into manufacturing footprint (through 4 plants, all in Dehradun) and R&D focus

-

What stood out to be that they are currently only at 40% capacity utilisation, which would mean that unit economics currently would not be too favourable. If they can deliver on their growth expectations in the next 4-5 years (Q1 FY 23 concall snippet below), this could provide substantial scope for operating leverage to play out and improve return ratios

A look into shareholding pattern and management credentials

-

Promoters have good skin in the game (~60% promoter holding)

-

Key person seems to be Hitesh Windlass (MD) who has been leading the company since 2020 (earlier led by his father). Hitesh’s background from annual report is as below

- There were also some good interviews with him around the IPO and he is the key person on the concalls. Link for a BQ interview below

https://www.youtube.com/embed/YoRGkM3YMME

- Overall, they seem to be building a foundation for a solid senior leadership team. A cursory search on LinkedIn showed me 350+ profiles, including strong key leadership profiles including a CBO who is ex director sales at GVK Bio and a CFO who is ex DSM Sinochem

I would also like to mention anti thesis pointers I could think of:-

- Management execution bandwidth still has to be proven and it remains to be seen if they do actually deliver on growth they project which will be required to deliver operating leverage and strong OCFs

- Lower GM and OPM profile suggest they operate in a highly competitive space

- I do not view this to be as evolved as say a Syngene with considerable IP, so possibly IPO valuations were quite demanding initially itself

- The inherent nature of it being a microcap makes it a high risk investment in the current exuberant environment

- My expertise in Pharma as a space is relatively limited versus other industries and hence there could be aspects I am missing

Though for my own investment purpose, the positives outweighed the negatives significantly. Key Thesis positives for me were:-

- Scope for longevity of growth in CDMO space

- Potential for growth triggers in trade generics and exports

- Potential long margin expansion from operating leverage

- Potential margin tailwinds from higher growth trade generics and exports

- Management credentials with skin in the game

- Reserves of 384 Cr in balance sheet currently and debt free status

- Current pessimism around the space and end of IPO lock in meant current valuations at ~1.1 PS, sub 15 PE did not feel demanding at all

Would be happy to have inputs of fellow members on the business.

Disclosure : I have recently invested in the company and am biased. I have made buy transactions in the last 30 days. I am not a SEBI registered advisor and investors should do their own research

| Subscribe To Our Free Newsletter |