July import-export values are out.

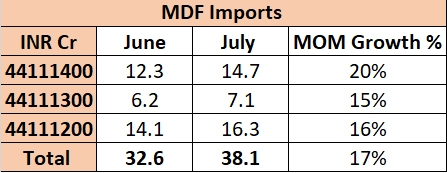

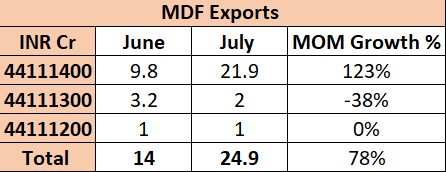

MDF imports have grown by 17% MoM but exports have increased by a whopping 78% MoM. June export numbers were low, so this MoM export growth is a little misleading. However, average monthly exports in Q1 FY23 were 25.5Cr, so the July numbers of 25Cr remain on trend and strong.

My interpretation : Freights are cooling off slowly but are still much higher than they were 2 years ago when imports were really strong. Export market remains healthy going by export revenues in July (Export realization data is needed to confirm this but that will only be available in Oct when Greenpanel releases its data).

Of course this data is with a lag of 1.5 months, so intervening changes in freights and import/export will affect real time data. Global freights seem to have come down by ~7% MoM from July to Aug, so this will have some incremental impact in Aug and Sep numbers.

Tracking freight remains a key for this stock. Going by the trend so far I am not expecting any significant dent in realizations in Q2. If freights keep coming down secularly in Q3 and Q4 then we might start seeing some moderation in realizations in late Q3-Q4. Shall wait for Q2 results to evaluate further.

| Subscribe To Our Free Newsletter |