@remonc –

1. Agree with the fact that RoE has low for the last 2 years. RoE, RoCE #s should be looked at when the company is in stable environment. If you look at any company which was operating in a turbulent environment these #s will usually look sub-par. But if on a very conservative basis,if the company were to have a 60-62% capacity utilization and stable cement prices their RoCE #s would improve to ~28%.

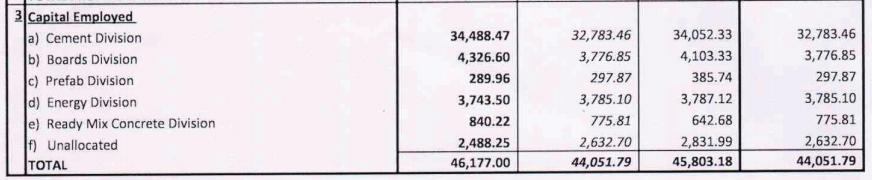

Here is how I arrived @ 28%:

Total Capital Employed: – 461 Crores, Q1 PBIT @ 62% capacity utilization was ~33 crores. If you annualize this you get a rough PBIT of 133 crores. 133/461 = ~28%

What are the major variables/risk factors that would affect the above #s? – Cement Price Stability & Demand

Price Stability – As of today, cement prices have been stable in south and with much of Q2 behind us, we can safely assume Q2 south cement prices have remained stable.

Demand – NCL’s customers are predominantly retail customers and demand is tepid and some of my friends point out that construction activity has not picked up yet in full swing. However, recently AP + Telangana government has started floating tenders for about 3MT cement.

These are the 2 big risk variables and if any one of these play out adversely, the above RoCE calculations would go for a toss. So if one is interested in NCL, he has to have a close eye on these two variables. Having said that, at current prices I feel there is reasonable MoS.

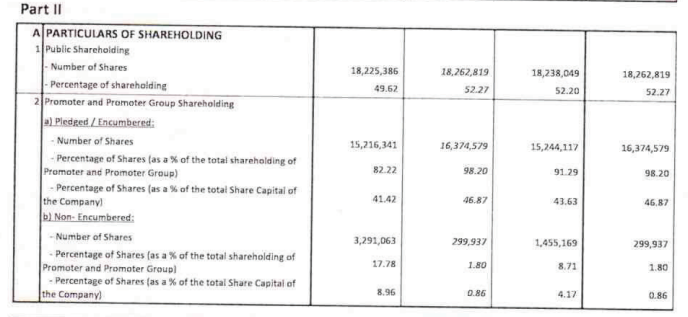

- Here is the break-up of pledged shares by the company after Q1 2016. As the company went into CDR, the promoter’s shares were provided as collateral and hence these were pledged.

As Nikhil has pointed out in the earlier posts, promoters have started releasing these pledged shares.

@manish26: I will check Anjani and get back to you. But before I entered into NCL, i checked out the valuations of other AP based cement companies like Sagar Cements, Deccan Cements & KCP. I found that NCL was relatively attractive.

@getsach – NCL is a small player and hence this will not be available in Analyst’s radar. So you will have to go through their annual report.

Thanks,

Ravi S

Disc – Invested. My views may be biased. Please do your due diligence.

| Subscribe To Our Free Newsletter |