Luckily (or unluckily only time will tell) my manager was on leave and I could not pre clear the trade- so I still have Mangalam in my portfolio. I went through this thread (excellent digging done by the likes of @Pranshinv and @phreakv6) and FY22-AR again to list down the positives and the negatives. I was hoping this exercise would outweigh one over another and help me pull the trigger.

Noting down my observation:

• 80% of the revenue comes from terpene operations of which 80% is contributed by camphor. So 64% of the total revenues for the company is from B2B Camphor ( B2C camphor is separately categorized under retail)

• From FY 21 to FY 22, the revenue grew by 45% but the PAT decreased by 35%. Q1 FY23 result is even worse(If you look at some of the posts on this thread around 2018-2019 there seems to be a belief that company can easily pass on increase in RM cost. That myth has convincingly been busted this year)

• The Forex outgo for the year was Rs 340 Cr while the COGS addition was worth Rs 401.9 Cr- almost all of the RM is imported. The company has never commented on what the raw material is but it most probably is Gum turpentine.

I tried to find correlation between Gum turpentine and camphor prices. Below is the long term chart of gum turpentine price i found online and the WPI chart of Camphor

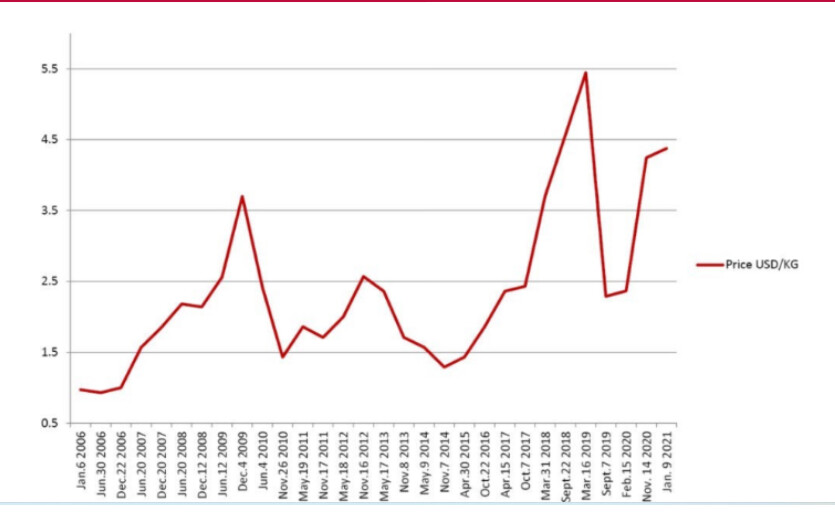

Gum Turpentine price chart

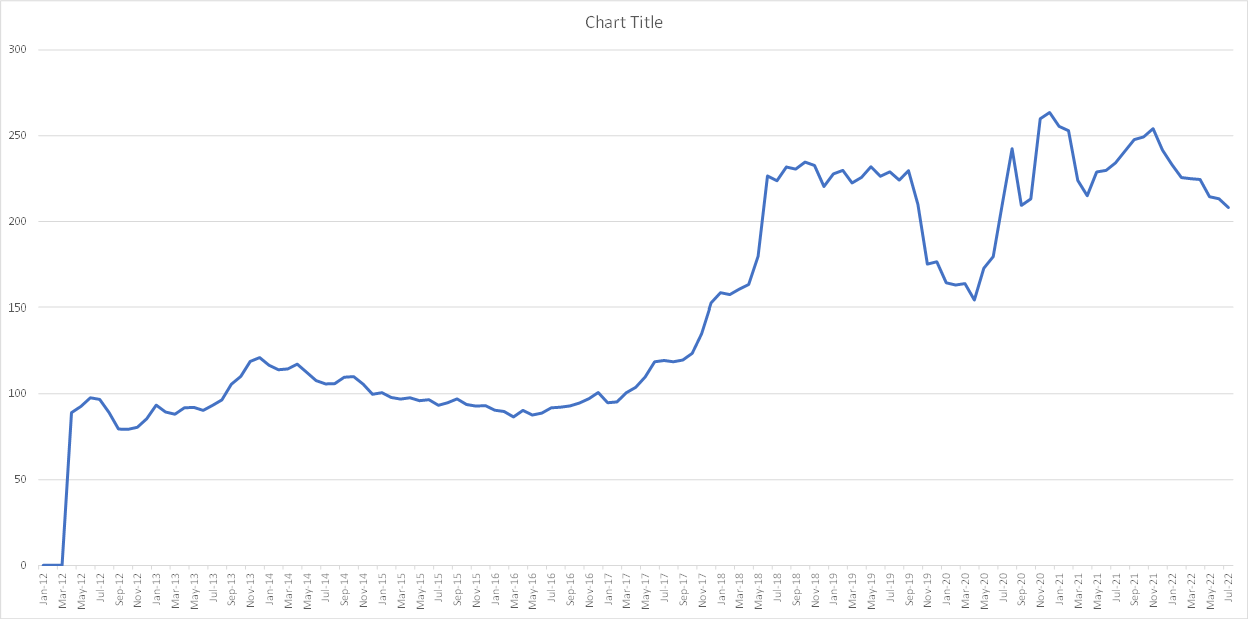

Camphor WPI chart

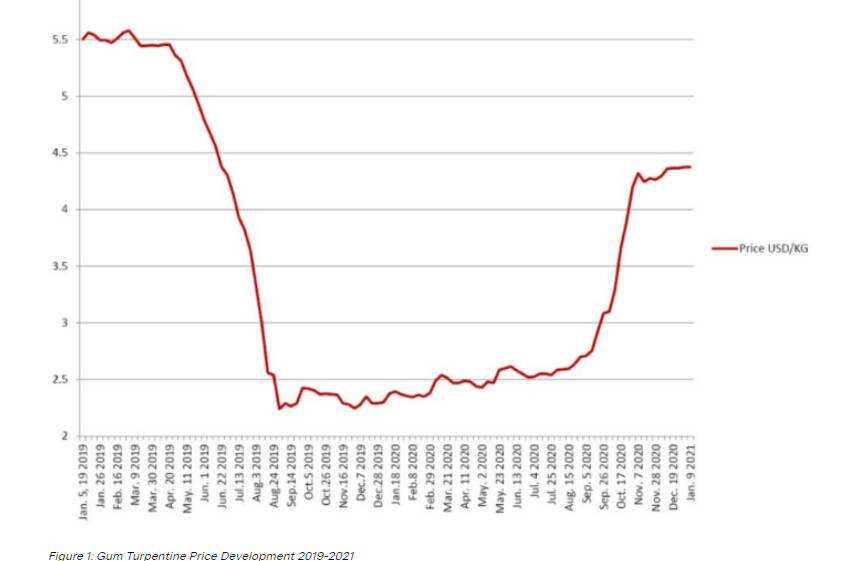

Recent trend of Gum turpentine prices

Source of gum turpentine charts:https://www.prinovaglobal.com/us/en/resources/trends/gum-turpentine

○ As expected Gum Turpentine prices and Camphor prices have historically always moved in tandem. However, last few quarter results suggests there might currently be a dissociation. Gum turpentine prices hasn't fallen at the pace at which camphor prices are falling. Company can also have a lot of high cost inventory which has taken the COGS up (Question for the Management at the AGM)

○ Whatever report I could find on the internet, all seem to suggest Gum Turpentine prices will continue going up for the foreseeable future because of its varied uses

○ The global camphor market is actually a fraction of the global gum turpentine market- Camphor prices won't pull up gum turpentine prices as is the case with most commodities and its RM. It most probably will be the other way round- Camphor prices will have to be adjusted according to gum turpentine prices.

• **Management Remuneration-** This has been discussed in the past, but I think promoter family is not being ethical here. Not only do the two directors draw Rs 3 crore each, 33 year old Akshay Dudojwala ( no meaningful experience in any other firm) draws Rs 3.6 crore as the Chief Strategy Officer. In all, these three account for Rs 9.6 Cr salary expenses which is 1/3rd of the total employee expenses, way too much for a Rs 500 Cr Mcap firm. To get a sense of how significant it is, I reduced their total salary by 50% which resulted in an increase in the pretax profits by around 10% for FY 22. For the sake of comparison, find below Kanchi Kapooram's top renumerations.

• **Market Opportunity**- The Company claims to be the largest manufacturer of Camphor in the world. That got me thinking how big can the camphor market be if a Rs 500 Cr Mcap company is the largest manufacturer. With some more help from Mr. Google, I found this- The global Synthetic camphor market size was $367.0million (Rs 2929 Cr) in 2019 and is projected to reach $448.1 million by 2027. Synthetic Camphor Market: Global Industry Analysis, Size and Forecast, 2018 to 2028 (futuremarketinsights.com)

This makes Mangalam have around 18% market share in the global synthetic camphor market,this was before Mangalam Organics doubled its capacity.Now with both Kanchi and Mangalam having more than doubled its capacity, there can downward pressure on the Camphor process due to excess supply.

• **Some accounting worries**: Other current asset has gone up significantly. Balance with Revenue authorities up from Rs 3.3 Cr to Rs. 14.35 Cr. I am no expert here, so not sure if this is normal. My worry is if there is some disputed claim that they have shown as Balance with revenue authorities.

What is this Rs 10 Cr Security Deposit. If possible someone should get this clarified by the Management

Now to the good bits…

• **Expansion plans :** @Pranshinv had shared MPCB order in one of his posts. I have assumed this to be the new production break-up.

In the table below, the highlighted portion is the data from MPCB order, based on which I came up with some estimates of revenue

To estimate the price/kg of camphor I looked up for the wholesale price (Rs 600-800/ kg). I assumed Mangalam's selling price will be lower to the wholesale selling price. To ensure that I am not way off mark, I used the Sep-18 Quarter revenue to deduce the final realisation as that quarter's WPI range is closest to the current WPI value of 210

Sodium Acetate prices in the wholesale market is around 20/kg

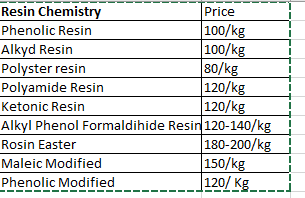

For resin Chemistry products I again checked the wholesale prices of products mentioned in the MPCB order. All the products are around the same range of 80-120/ Kg. I have assumed a selling price of 85 for Mangalam.

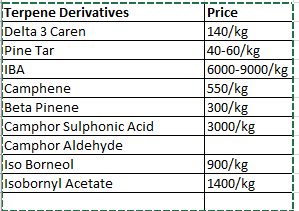

Terpene derivatives is what should get Mangalam Organics investors excited. Management has mentioned about Isobonyl Acetate as being the next growth area in the FY22 AR. (Some orders are in the final stages of approval). I have assumed an avg selling price of Rs 700/ Kg for terpene derivatives. There is no valid reason why it can’t be Rs 1000/Kg or even more. It all depends on what product Mangalam can produce off these derivatives and also at what rate. I have assumed 75% utilization level for all calculations.

MPCB order 11.11.2020.pdf (3.7 MB)

From these calculations, the estimated annual revenue on the expanded capacity is Rs 1548 Cr (whenever it comes fully onstream).

These estimates will make sense only if the MPCB order accurately reflects the expanded capacity and product mix. Management’s confirmation is required on this.

Few words on B2C: B2C currently accounts for 16% of the total revenue. Akshay Dudojwala on his Linkedin Bio says that he is spearheading the B2C operations and is targeting to take the B2C revenue share to 50%. There is no timeline mentioned for the same. I did not find any evidence to suggest that B2C is making money at EBIT level. Management should guide for targeted operating margin from B2C

I am not very sure if all of the camphor sale for Pious use is accounted in the B2C sales? Till now I was under the impression that pious use is the main contributor to camphor sales but that can’t be true if all of pious use sales are accounted for in the B2C revenues. Who are the B2B camphor customers and what are they buying for?– Requires Management’s confirmation

Hopefully the management clears few of these ambiguities at this year’s AGM

Disclosure: Currently 2.5% of my portfolio

| Subscribe To Our Free Newsletter |