Many risks are actually playing out currently.

- While saregama does have minimum guarantees in place the overflow revenue is because of growth in advertising. In a recessionary setting those wil suffer specially for Europe & western world geographies. When Europe is finding it difficult to pay bills i find it hard to imagine how anyone renews their Spotify 7 or 10 € / month subscription. This is a discretionary spending

- The carvaan phone is at least a management focus misallocation; depending on the wc requirement could be a capital misallocation too (bears would be quite to judge and bulls will probably give management enough time to execute).

- Gaana going off of free is at least a buyer side consolidation and can potentially affect the competitive dynamics of the industry going forward

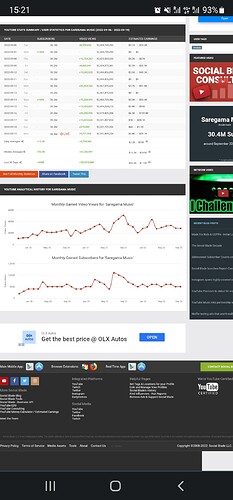

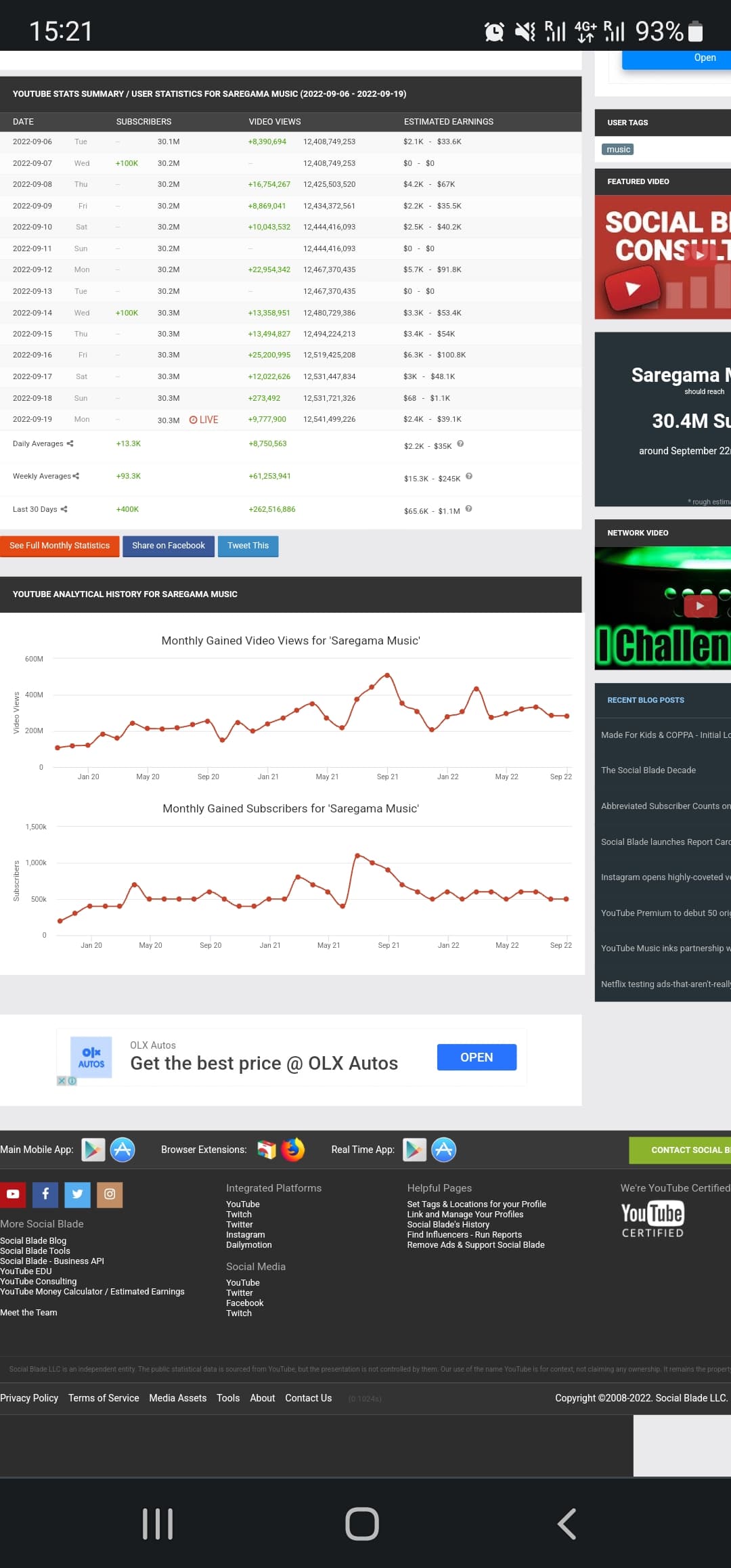

- From my calculations their streaming revenues have not been growing that fast last few quarters. Just see social blade stats for views

Alone each of those are probably things investors can ignore taken together imo they imply a real xirr risk at least in medium term of 1-2 years. I have halved my position. The supply side industry structure is still too too tooo good and thus i won’t be removing the position altogether. Let’s see how the one goes.

Disclaimer: invested, reduced position to half recent weeks.

| Subscribe To Our Free Newsletter |