Company Introduction:

Dynacons Systems & Solutions Ltd. (DSSL) is an IT company with global perspectives with its headquarters at Mumbai and branches all over India. Established in 1995, Dynacons undertakes all activities related to IT infrastructure including infrastructure design and consulting services, turnkey systems integration of large Network and Data Centre infrastructures including supply of associated equipment and software, onsite and remote facilities management of multi location infrastructure of domestic clients. The Company has built a strong customer base, variety of talent and a competent service delivery infrastructure.

Dynacons Enterprise Services offerings include a wide spectrum of Enterprise IT and Office Automation Services including Infrastructure Managed Services, Breakfix Services, Managed print Services, cloud Computing, Systems Integration Services, and Applications Development and Maintenance. The Company provides end-to-end technology and technology related services to corporations across industry verticals.

DSSL is headquartered in Mumbai and has 11 branch offices and warehouses with presence in more than 250 locations across India. The company also has a wholly owned subsidiary company in Singapore, handling Asia Pacific operations.

DSSL has strategic alliances with multiple Global Technology Companies.

DSSL has Over 2000 Clients ranging across verticals including :

- Global Companies

- Government & PSU

- BFSI

- Corporate

- Health Care

- Educational

Company Offerings:

Some of the Clients:

Numbers:

Company Strengths and Investment Thesis:

*DSSL has built a strong customer base, variety of talent and a competent service delivery infrastructure.

*Company was successfully appraised at Capability Maturity Model Integration (CMMI)- Level 5 v 2.0

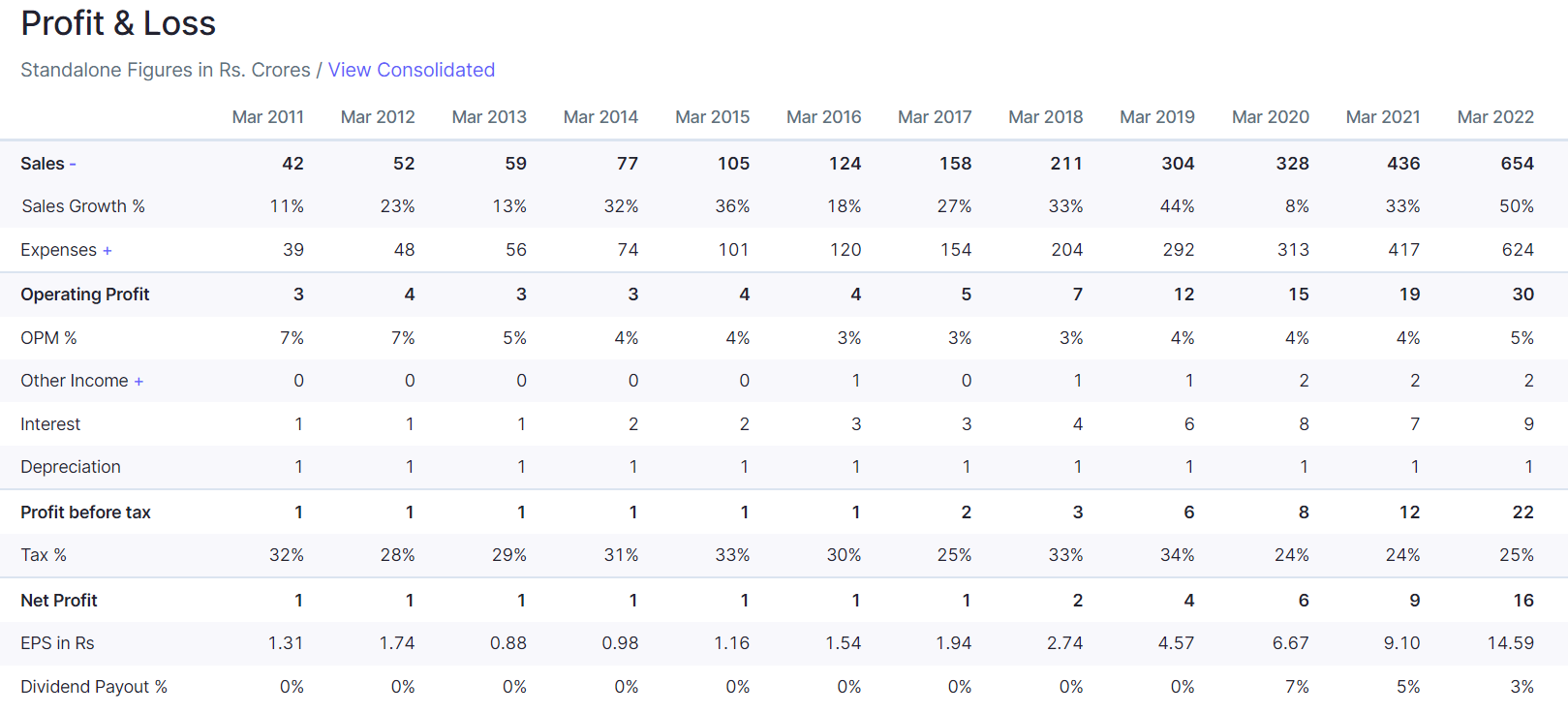

*Company is growing both topline and bottomline at steady pace. The operating income of DSSL has grown at a CAGR of 33 percent for the period FY2018-FY2022. The revenues increased to Rs. 653.98 Cr. in FY2022 from Rs. 435.94 Cr. in FY2021 and Rs.327.95 Cr. in FY2020.

*DSSL has an orderbook position of around Rs.940 crore (Against revenue of Rs.654 cr in FY20202) showing healthy revenue visibility over the medium term.

*The directors of the company have an experience of over two decades in the aforementioned line of business which has also helped the company to garner reputed clientele (See clients above).

*DSSL is trading at low Price to Sales multiple of 0.51 and reasonable P/E multiple of 19.1 considering the healthy order book and revenue visibility.

*DSSL has maintained healthy ROCE of above 20% in last 4 years (28% in FY2022).

*Promotors shareholding is in increasing trend and current promotor shareholding is 59.66%.

*Management provides regular update to shareholders on Order wins and have good annual report details for a company of this size.

Risks:

*This is a microcap company with mcap of 339 Cr. As with any microcap company, the risk is high and chance of capital erosion is high.

*DSSL operates in a fragmented and competitive IT industry, where it faces high competition

from small as well as well established players with high resources.

*DSSL undertakes significant business with government authorities like MCGM, RBI, LIC, SBI etc which demands an extended credit terms which has resulted in stretch in the debtors’ cycle during FY2022 which stood at 98 days against 85 days in FY2021.

*Trade receivables is high.

*OPM is very low around 5%.

Disclosure: Invested (This is not a investment advice. Please do your own diligence.)

| Subscribe To Our Free Newsletter |