As of today, have initiated a position in MCX, thus deploying some of the cash raised. These two charts explain the full thesis:

There is a massive increase in options volume on the exchange this year, primarily led by energy contracts. This is a completely new revenue stream that didnt exist last year. It is happening as a result of this:

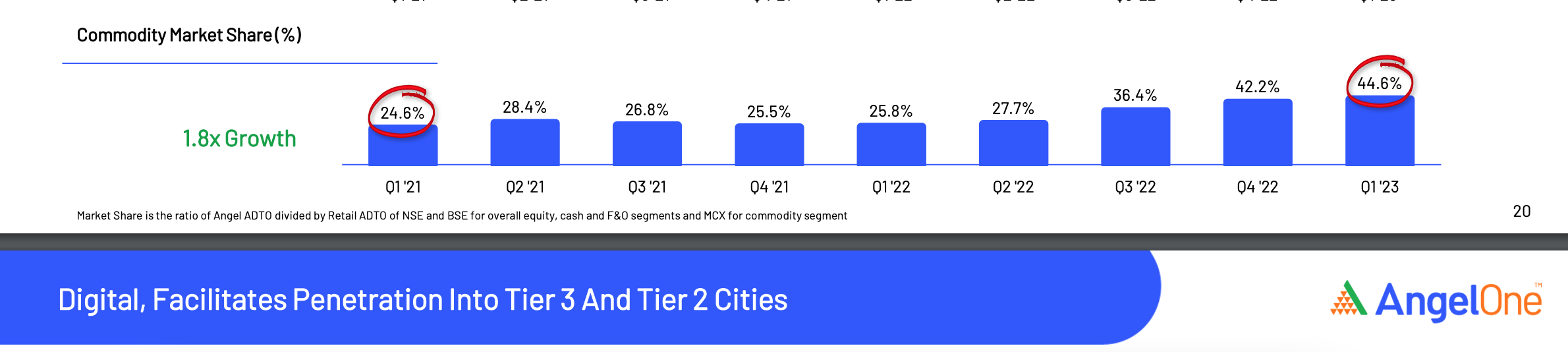

Above is the latest investor presentation of Angel Broking. Clearly, a large part of the increase in turnover is due to retail participation. Having transacted in futures contracts on MCX myself, I can understand why it was difficult for retail investors to participate in futures: the ticket sizes were very high: multiple lakhs for a single lot. Options brings the ticket sizes down substantially. At the moment there are 2-month options, MCX is planning to launch 1-month contracts soon. That should increase liquidity even more.

This interview with the Angel One Chief Growth officer explains why this shift has happened. The large volume jump has happened due to just one single brokerage house providing advisory services for commodities. Seems like a large opportunity here. Furthermore, the exchange will shift over to a new software system from Q4 hopefully. This will increase EBITDA and cash flow by a further 30-40 cr/year and make the software line item fixed rather than variable (more operating leverage).

My assumptions for FY25 are as follows:

Operating Revenue : 645 cr (predicated on 20k cr futures ADTV and 62k cr options ADTV)

Interest income: 98 cr (this is interest income of only the equity part, interest income from float goes into operating income)

Operating EBITDA: 425 cr

PAT: 338 cr

Exit EV/EBITDA Multiple: 25x

FY25 EV: 10.6k cr

Net Cash: 1250 cr (assume 100% payout ratio)

FY25 M.Cap: 11.9k cr (or equal to 35x FY25 PE, long term average multiple)

Today M.Cap: 6.35k cr

IRR : 28.5% + 2% div yield

Trajectory in options volume is the thing to track here.

| Subscribe To Our Free Newsletter |