There has undoubtedly been a lot of euphoria about SBCL recently especially on Valuepickr (And rightly so I guess, there are so many here who have been passionately following SBCL’s rise for a number of years :))

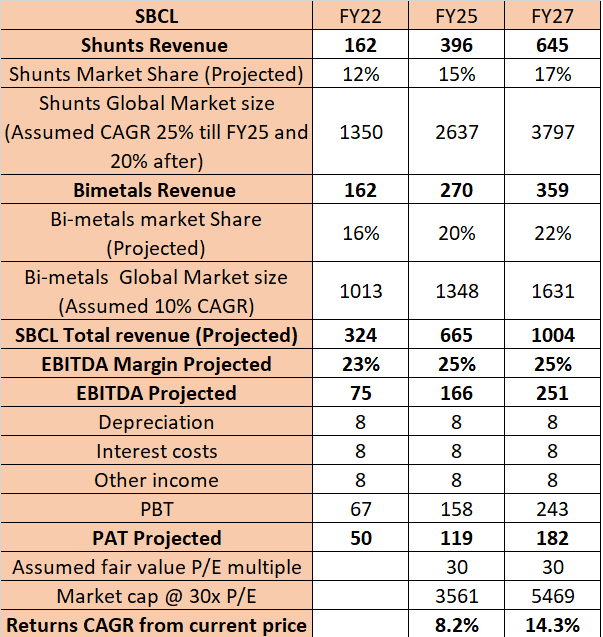

To quantify possible future returns from current prices, the best approach is to project potential revenues and earnings out 3 years or 5 years as per Management guidance and then apply suitable discounts to the guidance based on trust on Management etc. Based on what @Donald and @Worldlywiseinvestors have captured as management guidance, I have tried to put together a rough model of how SBCL revenues and earnings might look like 3 or 5 years out. Its a very back of the envelope calculation so I would invite folks to poke holes in the numbers so the projections could be fine tuned.

Assumptions:

-

Shunt market would grow @ 25% for next 3 years and @ 20% thereafter (FY25-FY27). This is roughly based on EV 4-wheeler growth estimates of 20% worldwide (cited by numerous reports that could be found online) and some extra growth to account for replacement of other current sensing tech with shunts.

-

Bi-metals being a much more mature product is assumed to grow @ 10%

-

As per management guidance, SBCL would move up from current 12% market share in shunts to 15% and 17% respectively in FY25 and FY27. And SBCL would move up from current 16% market share in bi-metals to 20% and 22% respectively

by FY25 and FY27 -

Given that shunts will significantly outstrip bimetals as % of revenue in 3-5 years, I have assumed SBCL’s EBITDA margin profile would improve by 200bps from current levels

-

Interest costs, depreciation costs and other income are assumed to be stable at 8Cr each (annualized FY23 Q1 numbers for each)

It would be a huge value add to the community if others could comment on these projections so that we could potentially arrive at numbers closer to reality.

| Subscribe To Our Free Newsletter |