Brickwork and Care have come up with a Rating for EFSL. It is very interesting to read.

I am trying to connect a few dots here.

They have provided information which is very hard to get from the management, and a lot of time, even if management provides , they spin the number so that it does not come as negative. However, both rating agencies have mainly focused on the negative part, as that is the intention of the rating which is good from investor’s point of view (management always provide positive spin so it is better to understand other side).

The rating is mainly focused on Credit Business (NBFC) and has given very insightful information (to me at least). It seems the rating is based on their audited FY22 results but it looks like Care received some information which is not yet in the public domain.

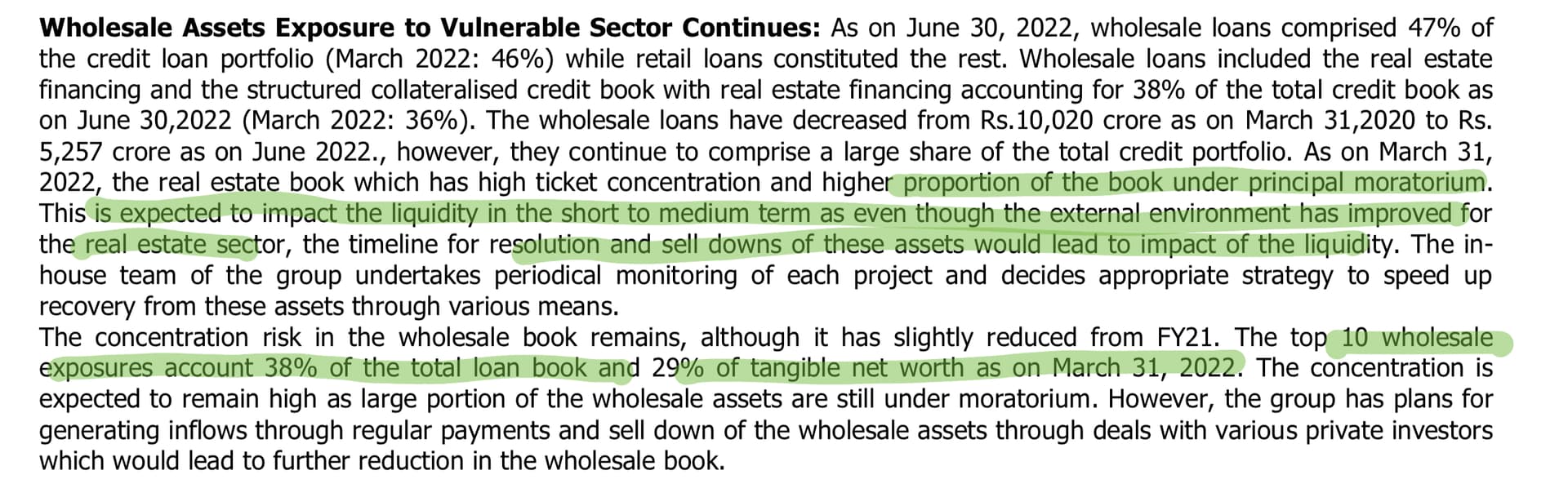

About Whole sale

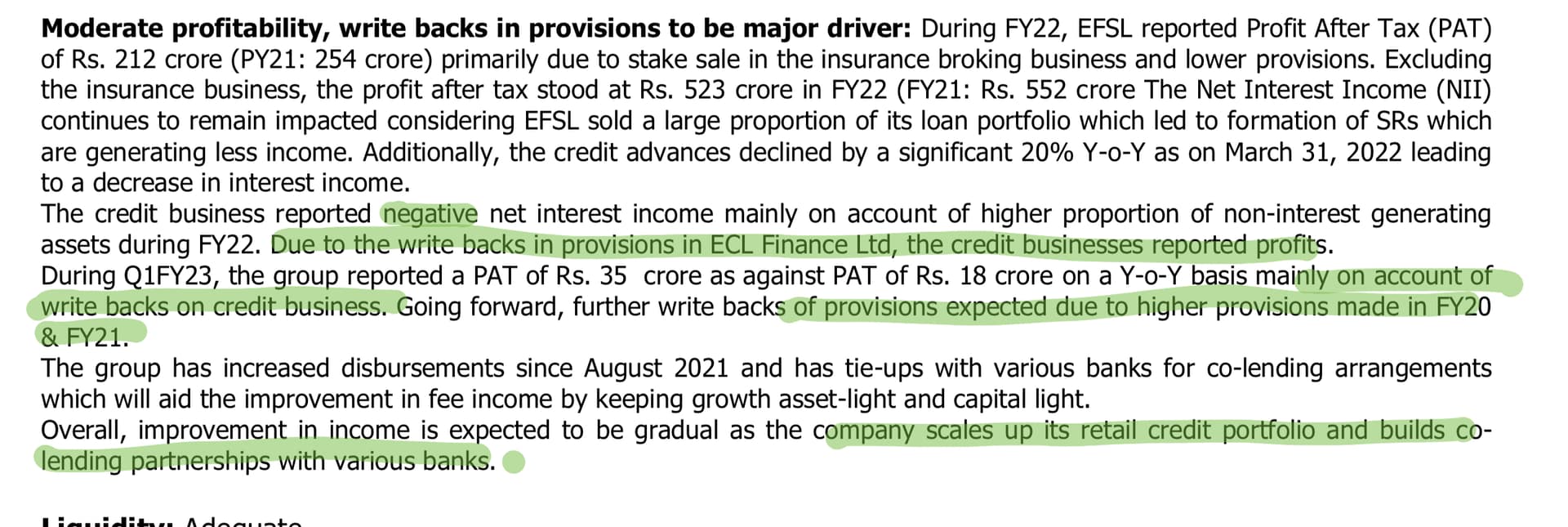

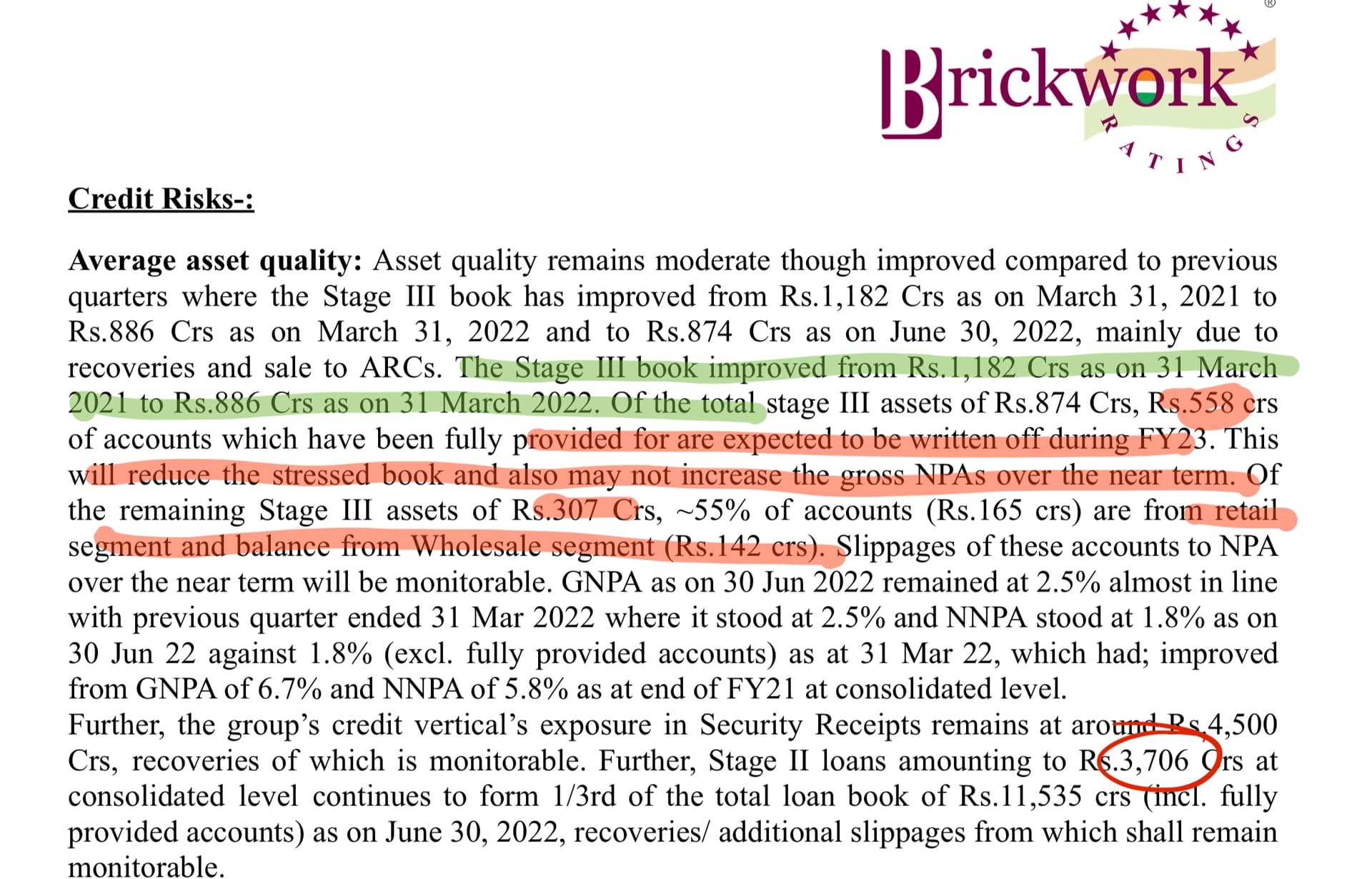

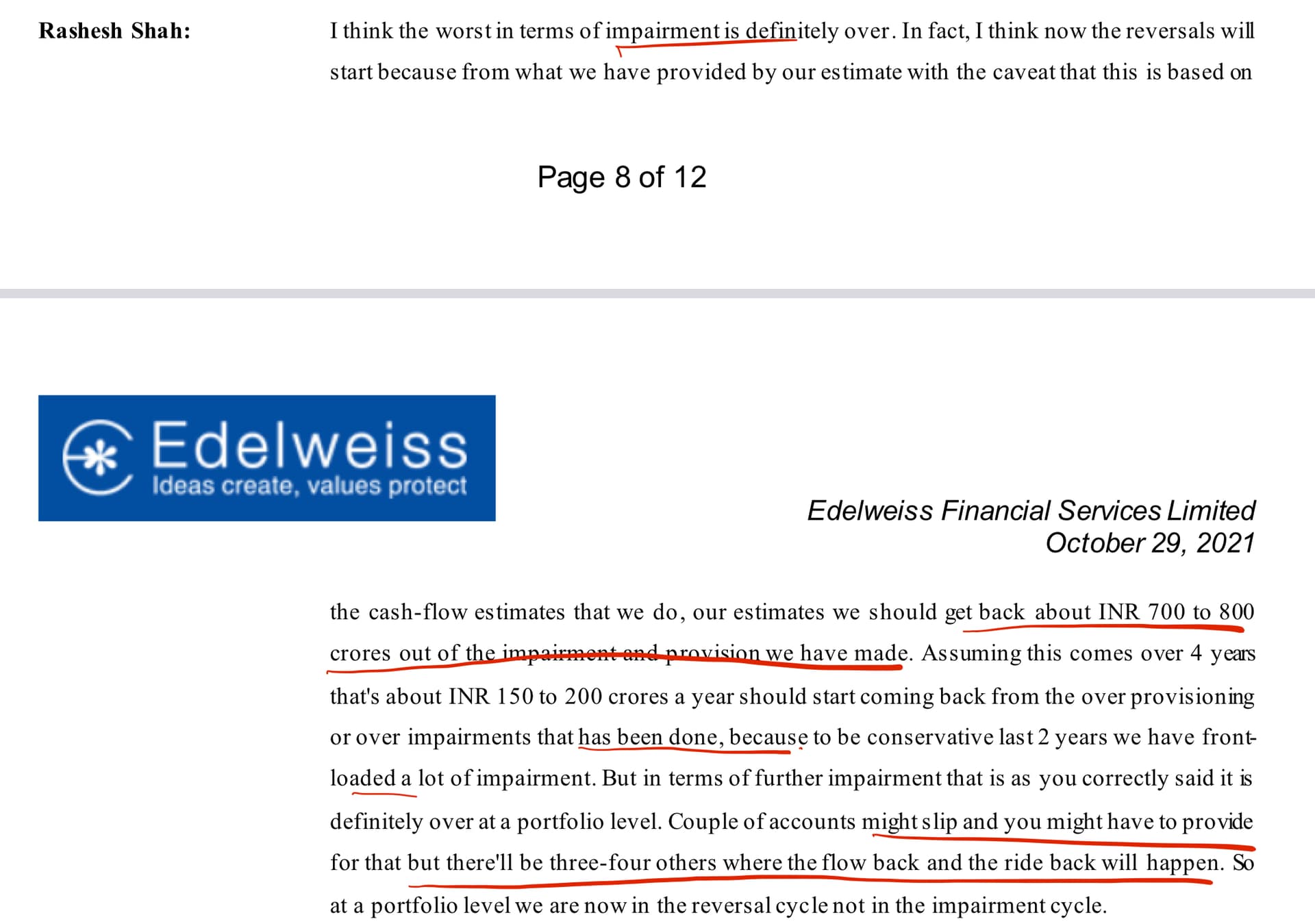

Out of the wholesale book if 8580 cr, the loan book of 4500 cr is on with ARC. ARC has provided a security receipt for this amount and EFLS received a small payment initially. As and when recoveries happen, the loan amount with flow thrown P&L. Flow back on the written amount will gather pace as per Ramesh Shah in an earlier con call, and this is the main reason for Q1 profitability for NBFC.

The downside of SR Is this amount does not earn any interest for them as it is not directly on their book anymore. As a result, their Interest income is and continues to lower. I think most of the NBFC profit will be write back for at least 3/4 quarters until retail segment pick.

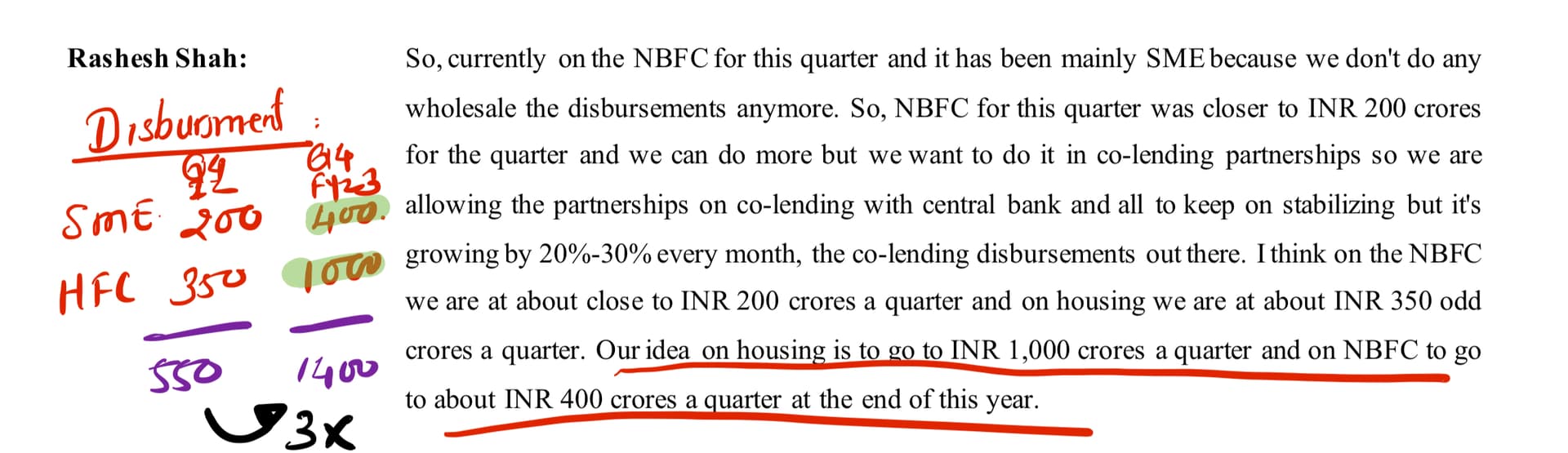

Both reports highlighted that EFSL sees a future in co-lending, which is what management has been saying for last 3/4 years. Other NBFCs such as IIFL Finance, and Capri has picked up loan disbursement in this segment, but EFSL is yet to show meaningful growth.

In Q4-FY22, ESFL has disbursed 550 cr and by Q4-Fy23, they want to triple co-lending. This will be an important monitorable from rating’s point of view as as profitability point of view.

| Subscribe To Our Free Newsletter |