Hi Harsh,

When you exited from ICICI Lombard, you mentioned that IL’s inability to scale Health Insurance segment prompted the call to exit.

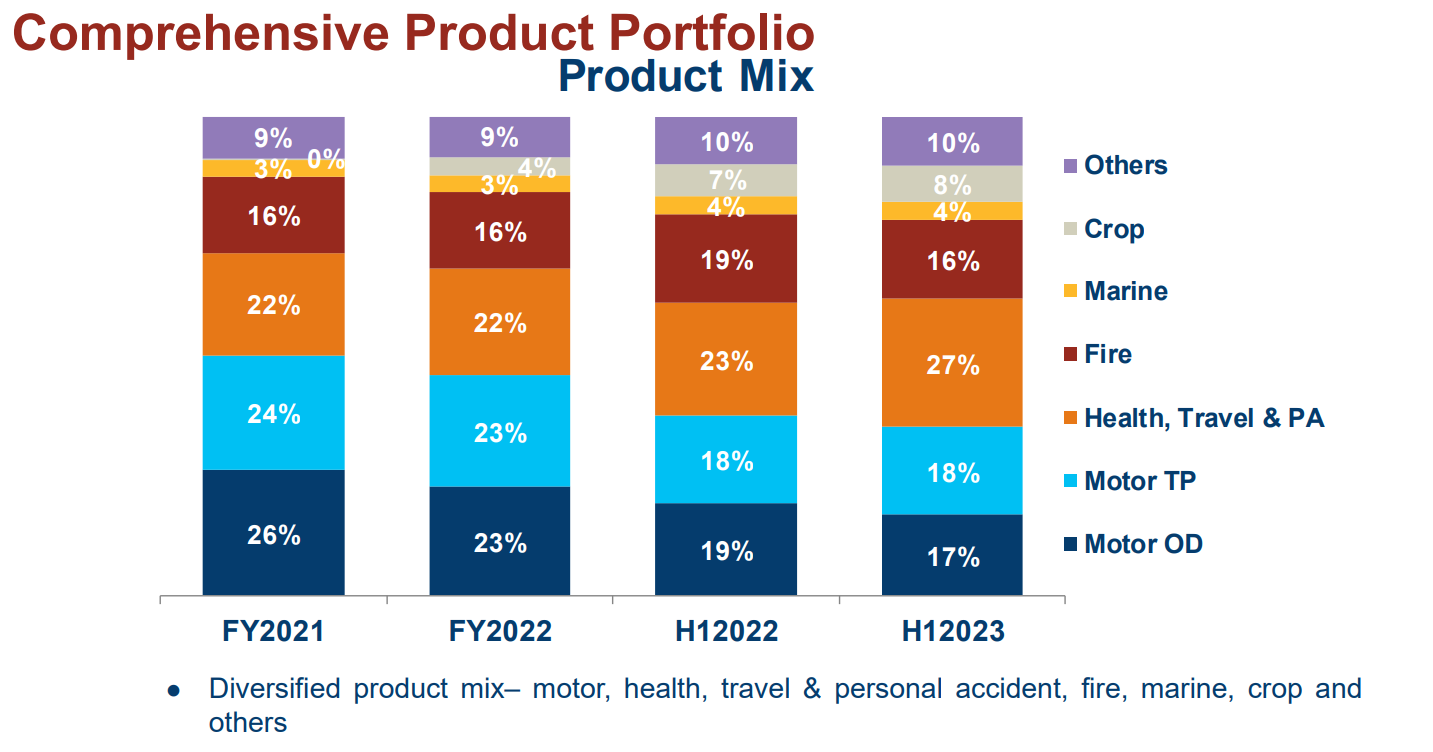

As per company’s H1-2023 presentation, Health, travel & PA segment improved to 27% of the product mix vis-à-vis 23% for H1-2022.

GDPI for this segment grew from ₹2015 crore for H1 2022 to ₹2834 crore for H1 2023 (~40% growth). Although, the growth is mainly driven by Health-Corporate segment whereas Health-retail growth is muted and Health-Govt de-grew.

The company is making all the right noises regarding capturing market share in health segment. From the concall-

Within the quarter, we have outgrown the industry and standalone players for the month of September with a growth of 21.1%. This was driven by growth in business sourced through retail health agency vertical of 30.7% in Q2 FY2023.

At the time of writing this post, P/B ratio has further moderated to 5.7.

Given that the interest rates have increased world over and in India, the investment portfolio float is more valuable now than this time last year (ignoring the short term MTM losses).

Does this stock catches your fancy now that the major concern of growth in health segment is resolved, or will be sitting out waiting for P/B to moderate further to 4 as you have mentioned previously?

| Subscribe To Our Free Newsletter |