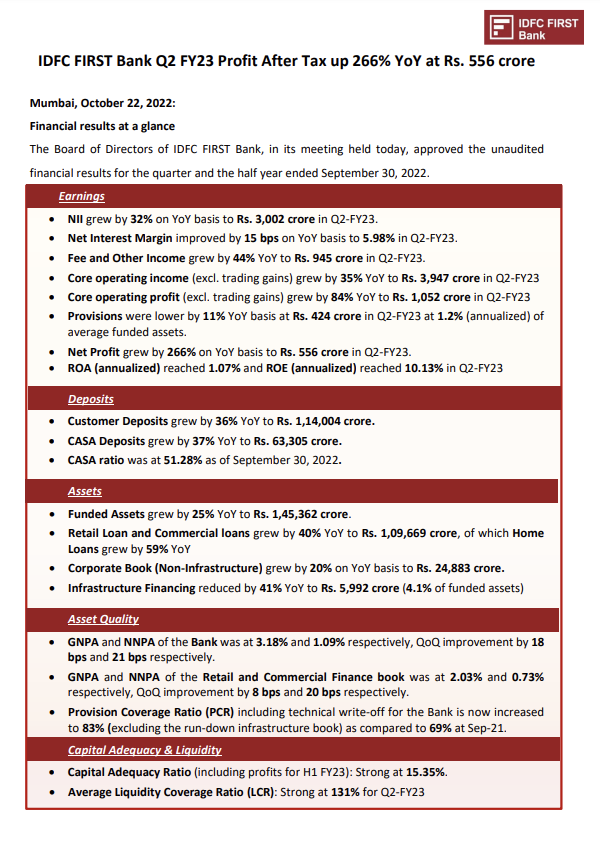

- Retail loan book growth led by home loans

- RoA at 1.1%. RoE > 10%. Karan Arjun aa gaye?

- Credit Costs at ~1.2% quarterly annualized) much lower than < 1.5% guidance so far

- Infra book is now only 4% of assets

- PCR is strong at 83%

- One thing to remember: the 3% GNPA includes a large toll road which though technically NPA is paying (NPA was due to covid time 0 traffic). This will further improve significantly to be ~2% after dues payments sometime in FY24 IMO.

Disc: Invested, biased

| Subscribe To Our Free Newsletter |