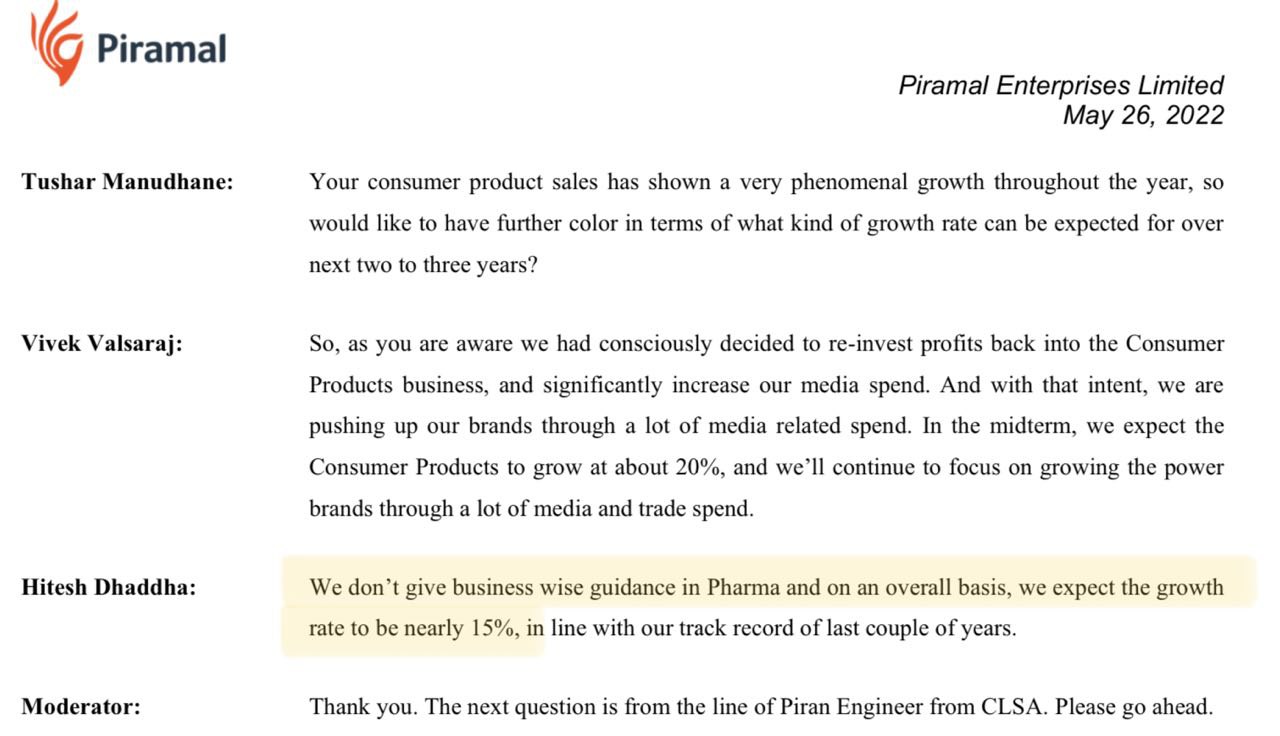

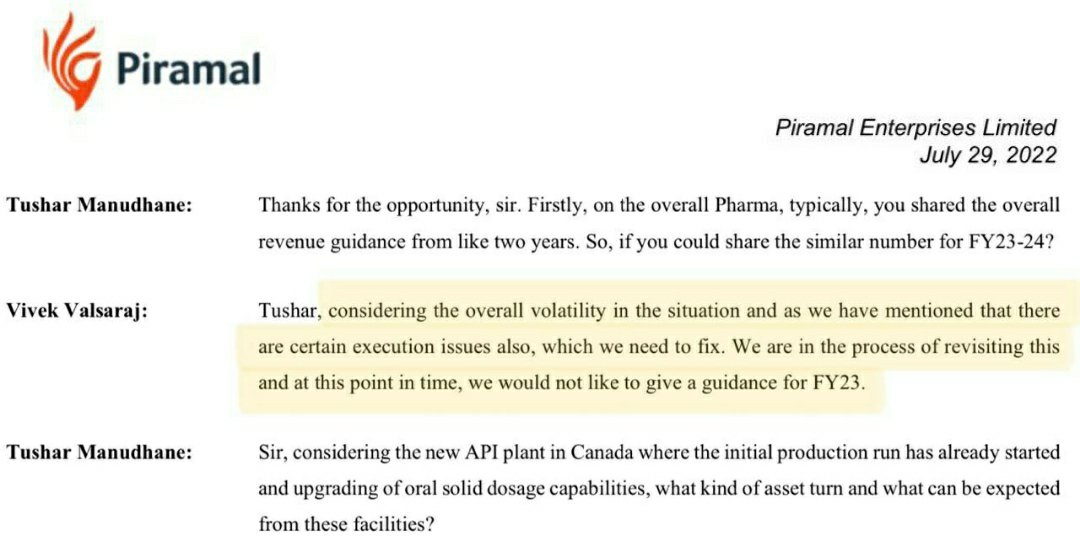

On May 2022, management gave a guidance of 15% growth rate for overall pharma business.

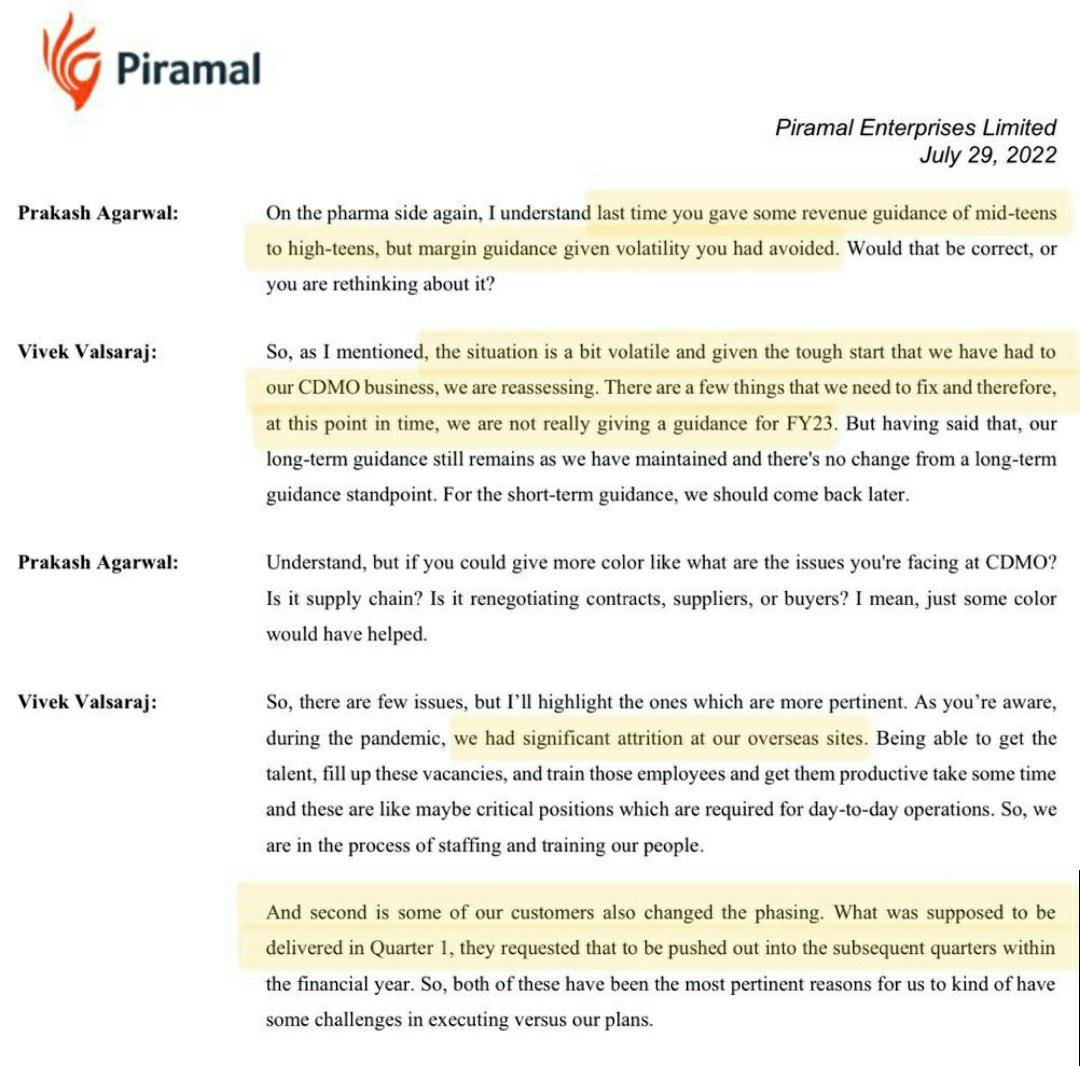

But during July 2022, they said they don’t want to give guidance for 2023 because of overall volatility in the business & certain execution issues they need to fix first.

What made them to rethink the guidance?

-

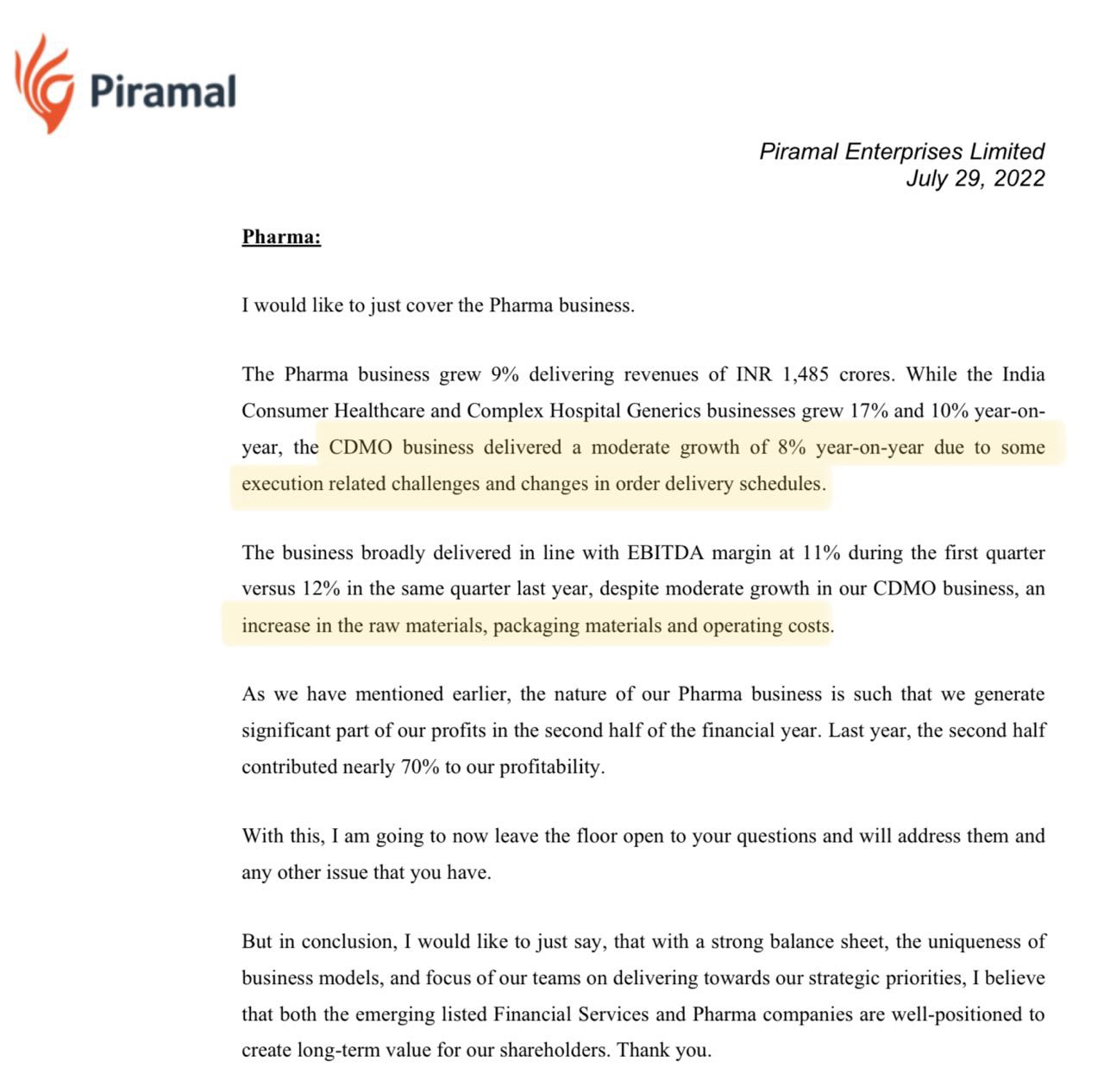

Facing tough time in CDMO business. Some of the customers changed the phasing of orders. Orders are pushed into future.

-

Significant attrition at overseas sites. Finding right talent, filling up these vacancies &training them may take some time. These are critical positions.

- Higher operating costs, increase in raw material & packaging materials prices. (Inflationary situation in UK & USA)

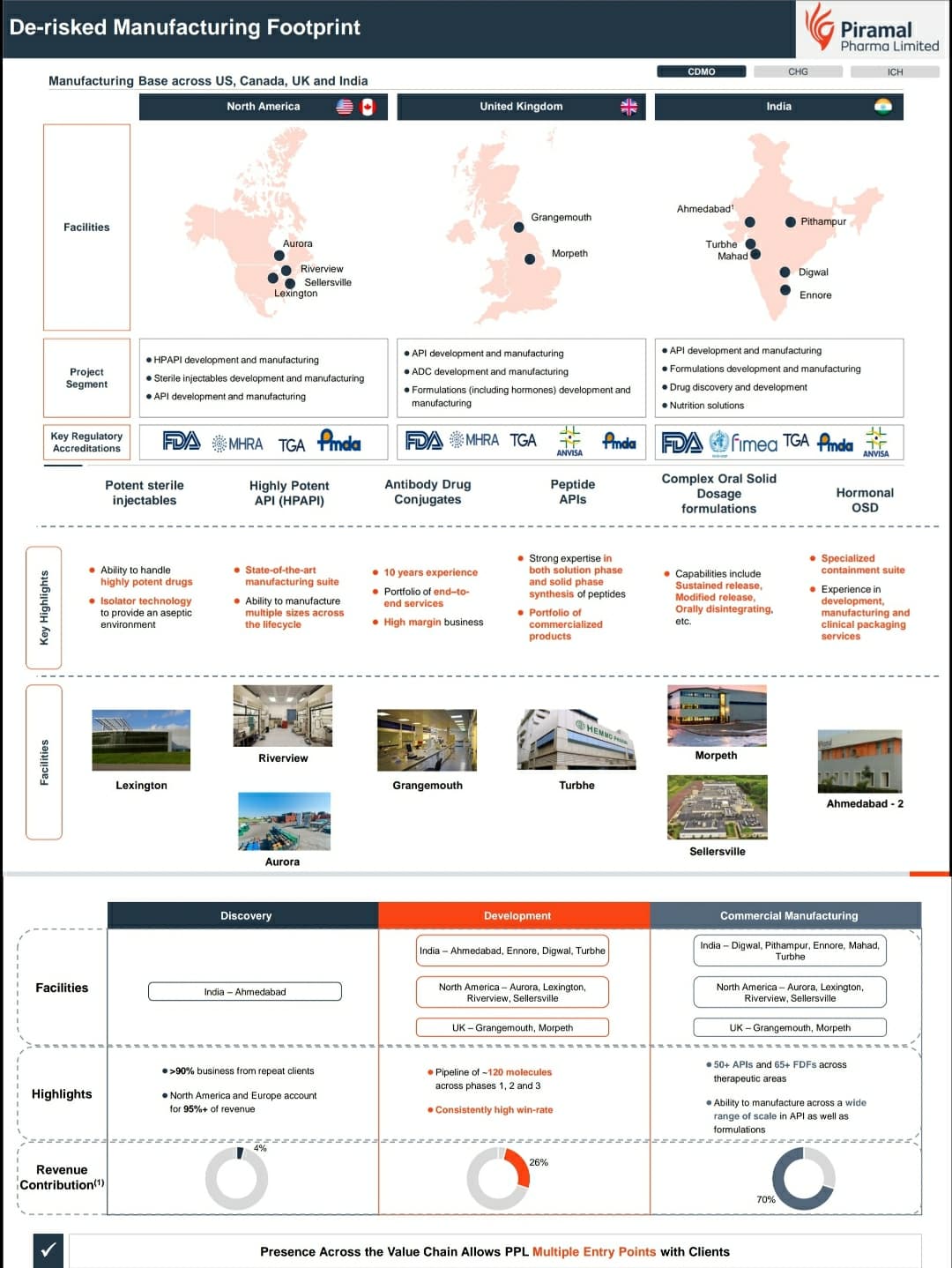

They have many overseas facilities which make niche products & are essential facilities in their integrated services.

Sterile injectables – Lexington (USA)

HPAPI – Aurora & Riverview (USA)

ADC – Grangemouth (UK)

Complex oral solid dosage- UK & USA.

I reckon these facilities are facing

1.Attrition of critical talents & finding the replacements & training them may take some time & effort.

2.Higher operational costs due to highly inflationary situation in UK & USA.

3.Power crisis in Europe. Pharma manufacturing is highly power intensive & this may affect the margins.

Not a buy/sell recommendation.

Disclaimer: I dont own PPL.

| Subscribe To Our Free Newsletter |