Ksolve India appear on screener due to consistent quarterly growth of more than 15% growth in YOY revenue and >20% growth in YOY net profit every quarter. Further, dividend yield was also high. However, I rejected the investment as it was listed on NSE SME and also management did indicate that they wanted to increase equity in order to get listed on NSE Main exchange.

Post September 2022 results, it again appears in my screen. The company was already listed on NSE, nil debt and also higher dividend payment. Hence, I got interested to explore further about the company. I did read Valuepickr post on the company. I also read last two annual reports, Prospectus and investor presentation of the company. Subsequently to this and also some primary analysis, I decided to invest a tracking position of 1% portfolio in the company.

The main factors for my investment are as under:

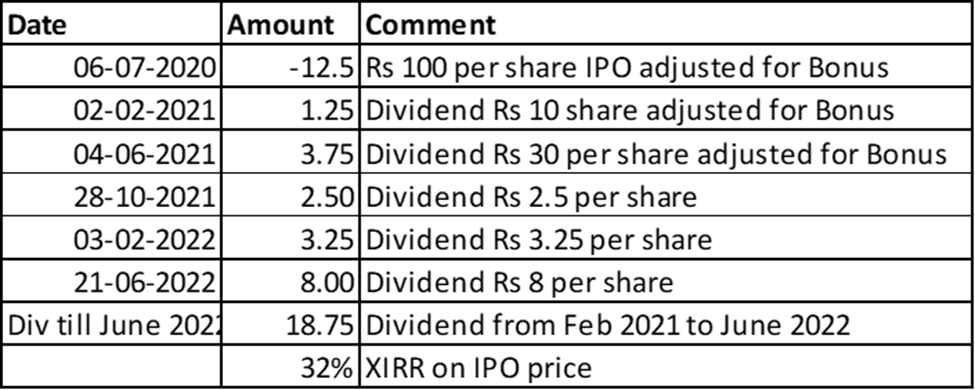

- Dividend payment since listing is higher than total issue price of share in IPO:

The company raised Rs 4.02 Cr during IPO in June-July 2020. The IPO price was Rs 100 per share (face value 10 paid up). Subsequently to IPO, the company issued bonus share twice, which resulted in increase in holding by 8 time. So 1 share in IPO at Rs 100, would now be 8 shares, resulting in cost per share of Rs 12.5 in June 2020.

As against, this cumulative dividend paid by the company till June 2022 are as under:

In case company continue to grow dividend even at 5% p.a. for next 5 years, it would serve my investment purpose. It is too simple to forecast, but too difficult to be correct on forecast

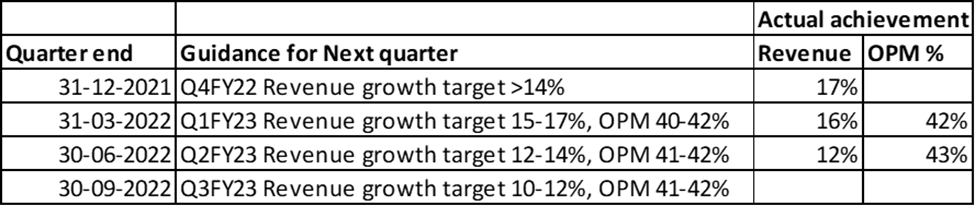

- Past performance and actual achievement:

Find enclosed actual achievement vis guidance of management over last few quarters. While the current data suggest management capabilities on execution has been good, the period of data available (only 3 quarters) is too small to make any meaningful judgment. Nevertheless, the past performance increases my optimism in the company.

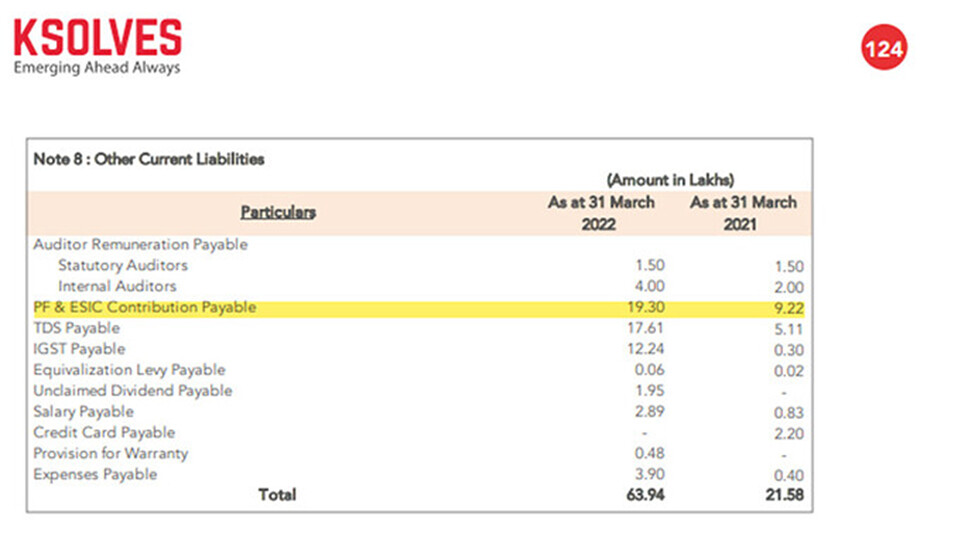

- EPF Data with Company data comparison

My limited past experience with special companies suggest generally company find it difficult to manage employee related data. Of course, Satyam has been legend in managing employee strengths as well, it is generally difficult to manage the EPF data (as cash are actually need to be paid to Govt).

Hence, in order cross check the number of employee and payment to EPF, I downloaded employee number and amount paid by EPF by Ksolve. While there would be some amount of difference can be explained by employee not being eligible to EPF (foreign employee/ contract worker etc) and other reporting factors, the deviation in employee strength from EPF data and Company reporting for March are within my acceptable range of around 5%. (Please note that this is very subjective assessment and may be completely wrong).

Further the amount paid for March month (in April month) for EPF for March 2021 and March 2022 is also matching with Standalone Financial Current liabilities in annual report. Since the company also need to pay amount for Employee state insurance and heading is PF and ESI Contribution payable, we can attribute variance to ESI.

Find enclosed information table.

Risk Factors:

-

Limited understanding of business:

While I have limited understanding of financials and accounts, I am near zero in understand IT industry in which company operate. Hence, I cannot compresence whether the verticals and segment in which the company is present can grow and whether company will be able to maintained competitive edge in its area of operations. Further, the recent growth in last two years, might be due to change in IT sector growth orbit due to Lockdown. With world market opening, whether the IT offerings of the company (mainly Salesforce and other products) would be relevant to clients, one need to observe same over period, -

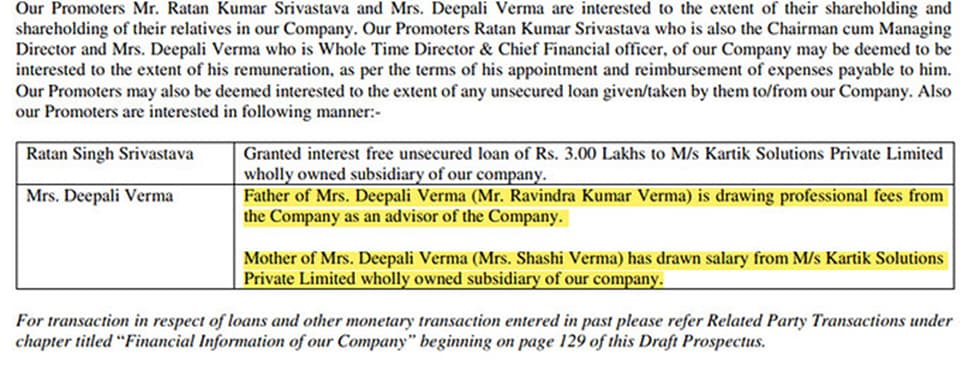

Payment of fees to related parties:

The relative of the promoter has received payments from the company for services provided. While the amount involved may not be material, but such deals shall be avoided in good companies in my opinion. The enclosed information compiled from Prospectus of the company

-

Multiple resignations of Directors and KMP:

Over past two years, CFO as well as CS has resigned from the company. Similarly, there has been multiple resignations and additions in directors. While it is not unusual in small companies, still it needs further investigation for frequent changes in KMP/Directors -

Stretched valuation:

The company is trading P/E ratio of 27 times and 13% lower at current price of Rs 450 as against all time of Rs 519. The current valuation provides limited margin of safety in my understanding.

Further, my record in investing in small companies has been mediocre at best and below average in reality. I have taken many wrong decisions and missed major red flags when my greed has exceeded my rationality. Arrow Greentech is one such hope investment for which I booked very large loss in my investment career. Hence, I may have missed many critical aspects which are very obvious and need special attention while investing.

Discl: Invested 1% of portfolio in the company in last 7 days. My view may be biased due to my investment. I am not a SEBI registered advisor. I am not recommending any investment action in the company. Reader shall do his/her own due diligence before making any investment decision. I may exit from investment without intimating this forum in case I my personal risk profile changes.

| Subscribe To Our Free Newsletter |