I took time to buy into HBL Power systems because hitherto I was used to buying companies where the numbers are there but HBL is a company where the numbers will come in future. So, the past looks hazy but the future looks bright as amply written by the folks following the company closely.

Some observations:

- Debt NIL

- RoE = 10% (Low but cyclical low)

- Last 10 years NIL revenue growth & so is share price (doubled in 15 years). So, market has been efficient. Not much future is baked in the current price.

Now, the numbers:

FY 22:

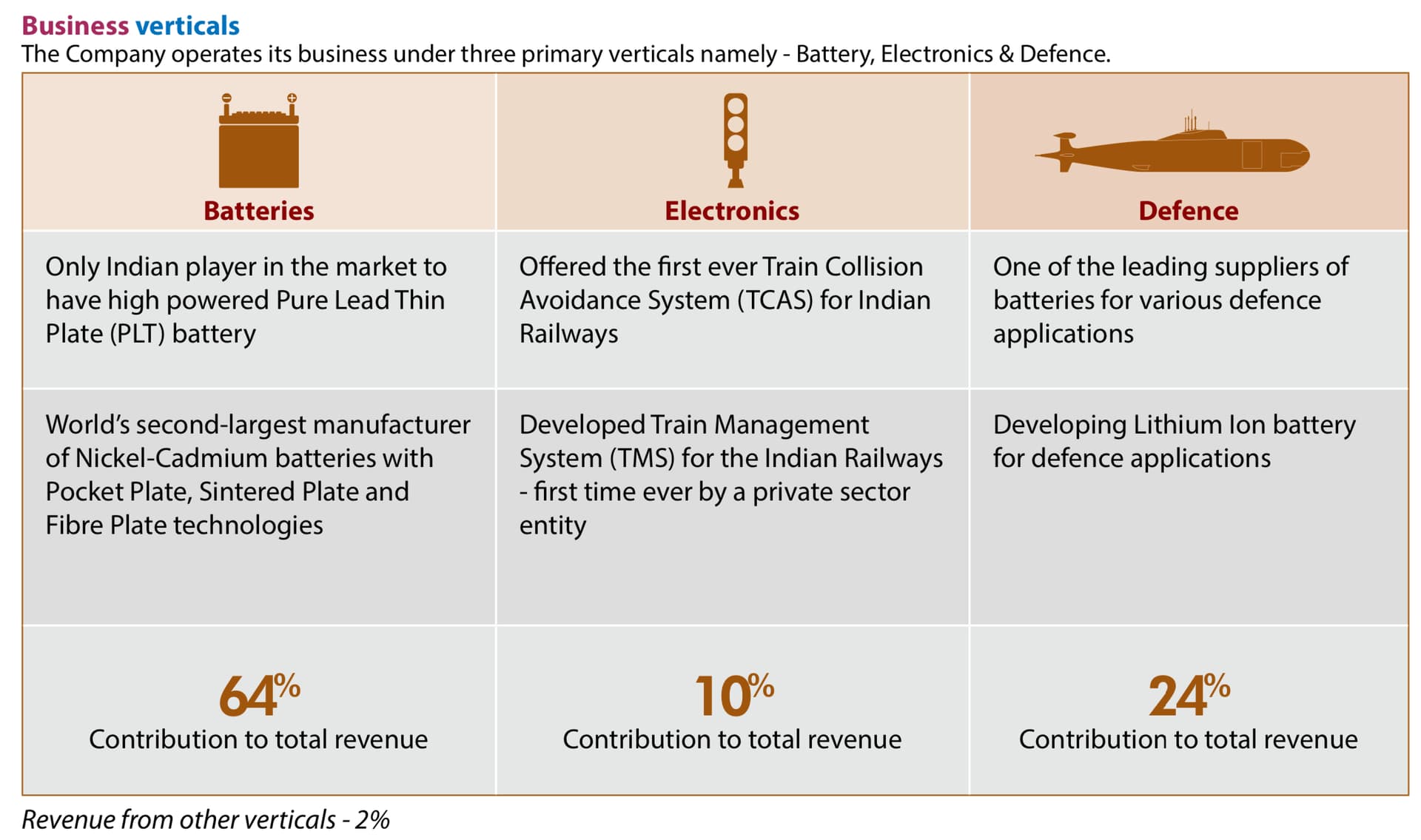

Batteries ~ 780 Cr

Electronics ~ 120 Cr

Defence ~ 300 Cr

What FY 25 looks like?

Batteries: 1000 Cr

Electronics: 1000 Cr

Defence: 300

Rationale: Batteries, I assumed average growth even with 5G.

Electronics: Assuming 3000 Cr per Annum of Railways business & HBL takes 1/3rd of it, assumed not much from electric drive train.

Defence: High base of FY 22, so assumed NIL growth.

In all the three segments, I have filled in conservative numbers. Even though Railways ministry has been super efficient, at the end of it it’s a Government business so I assumed Kavach project to overshoot by 4 years & finish by FY30 only (30000 crore budget spanned across 10 years). The fly in the ointment is 2 new competitors. By then I assume HBL would have showcased enough project management skills. I assumed stable government till then & fair budget allocations. Given the fiscal status & GDP growth, this is fair for India in the coming decade barring anything cataclysmic.

FY 25E, on 2300 crore revenue & margins of 15% (12% is last year margins & Railways business is highly margin accretive & less working capital intensive as well given that MoR has been paying in a week), EBIDTA comes out to be ~ 350 crore. There would be servicing revenue which is annuity type where HBL TCAS is serviced by HBL only for eternity. Servicing revenue is very high margins. Triveni Turbine too is increasing service revenue, which grew by 80% last quarter, of course on a low base. But I think Triveni can service any other turbine as well not only proprietary turbines.

It all comes down to –

So, Conservatively, For a business making 350 crore EBIDTA in FY25E, NIL debt, RoE >15%, 12-15% growth, 15% margins, it seems fair that 15 times EBIDTA which makes the market cap to 5250 crore, while the current market cap is 3000 crore.

Risk: Most of the thesis is predicated on Railways!!! Key man risk as pointed out by others. I would have preferred the MD appoint a professional CEO.

Someone interested can point out chinks in the armour?

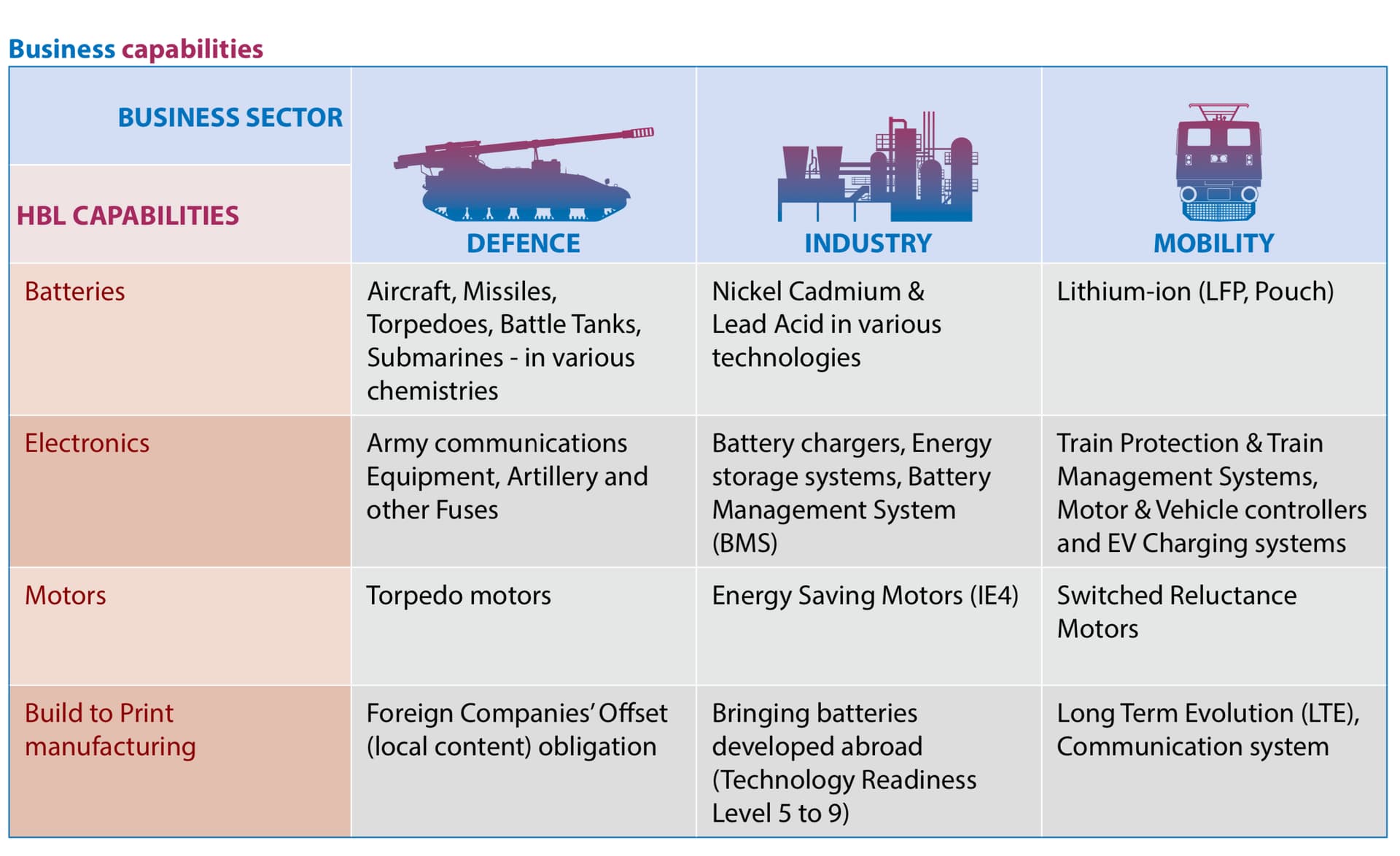

The Annual report is amply positive:

Important snippets below:

| Subscribe To Our Free Newsletter |