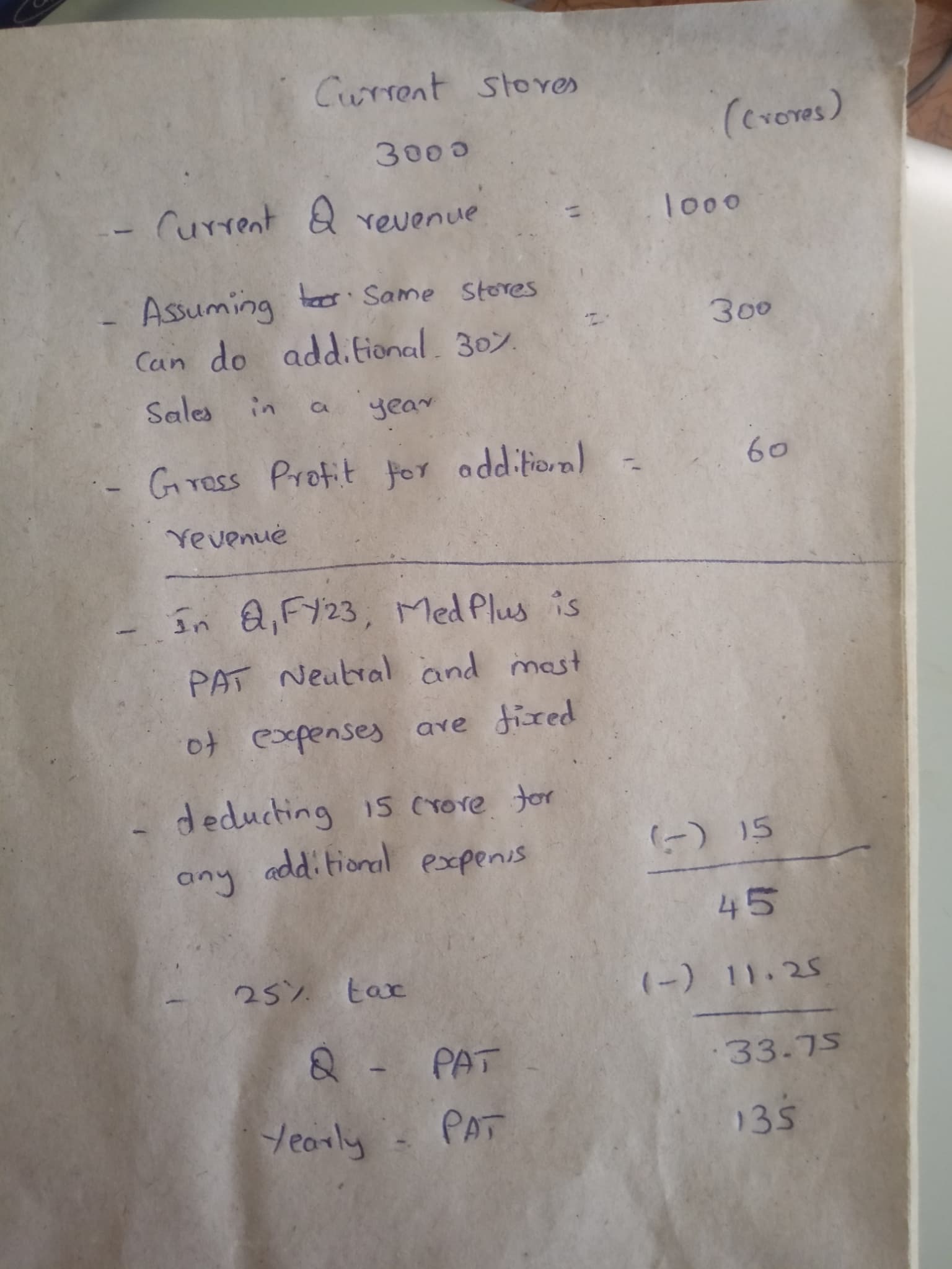

My assumptions lead to similiar PAT, I value 2500 cr for current stores and 600 cr for any new stores they put in and not valuing optics and diagnostics business. I feel anything near to 3500 crore valuation is good. Now its exactly 2x.

In your assumptions, you need to change topline, in last quarter itself, they did 1000 crore topline, you are calculating 1600 crores entire year. You are not deducting enough from ebidta to pat. They will incur rent payments as interest and depreciation after ebidta, so you have to tweek there also

| Subscribe To Our Free Newsletter |