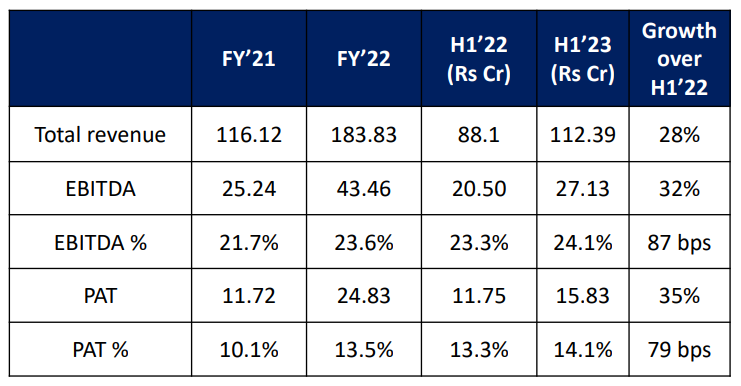

Management expects to better its 1H performance in 2H. lt expects revenues for FY23 to be at Rs 230 crores aided by strong momentum across all its four segmenrs; own Brands, Exports, OEMs & Apr. while EBITDA margins are expected to improve further.

Beta’s strong pipeline, enhanced capacity, Apl expansion and entering new export

markets will continue to support growth in the coming years.

Rs230crs implies 25% revenues growth. Assuming same PAT margin same as 1H for full year (actually it should be higher given management expects margins to expand). PAT for full year will Rs32.4crs which implies at current market cap of Rs700crs stock trades at 21.6x P/E for FY23E

| Subscribe To Our Free Newsletter |