I do not think the PAT will bounce back quickly. The reason is due to the shift from product to platform business.

When a product company move licence revenue from one-time licences to subscription-based revenue, it is always a painful journey. I think IDA started it a couple of years back, but now this product-to-platform shift is accelerating, and it will continue to cause a problem for some time.

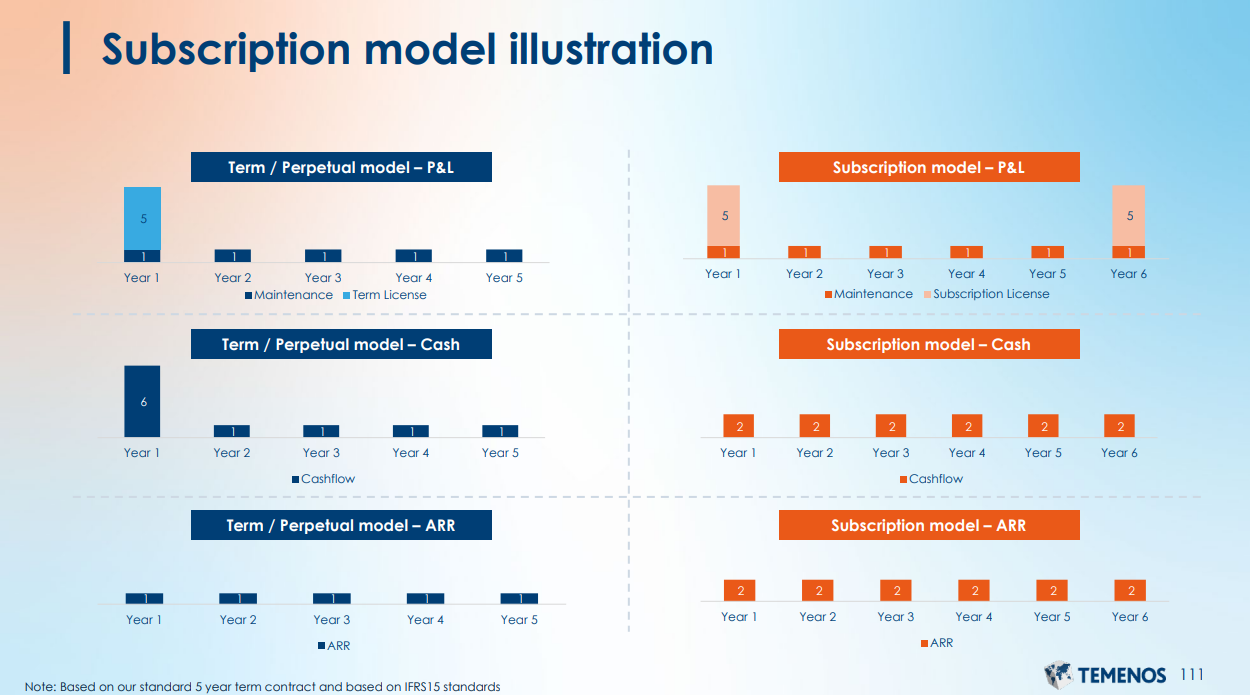

As per the Temenos calls, this is how they book subscription revenue.

Arun Jain is more or less saying the same time. IDA won products with a linces cost of $2.9 million. Had the sales been a one-time license, their PAT would have been higher by at least $2 million(as licences have very less cost). However, IDA could report only 1 or 2 cr of revenue in the current quarter due to subscription-based revenue. As a result. The PAT slump is severe.

AS more and more clients prefer to use the platform, this impact will be visible for a few quarters at least. The customer they are signing today is likely to be very profitable (75% gross margin business) in 2 to 3 years, but it will be a hard grind until then.

They said earlier that Tier 1/2 clients prefer one-time linceses. If they manage to sign a few Tier 1/2 clients in the next 2/3 quarters, the picture could be different.

In summary, it seems to me that PAT will take some time to recover to an earlier level (80cr + quarters run rate), so this year’s PAT will be considerably lower than FY22.

Here is today’s interview on TV18

https://www.youtube.com/embed/UOBXlY2QPhs

| Subscribe To Our Free Newsletter |