Yep. The demand of cotton should come down and supply should ramp up. Seems the prices have already corrected significantly to pre-COVID levels.

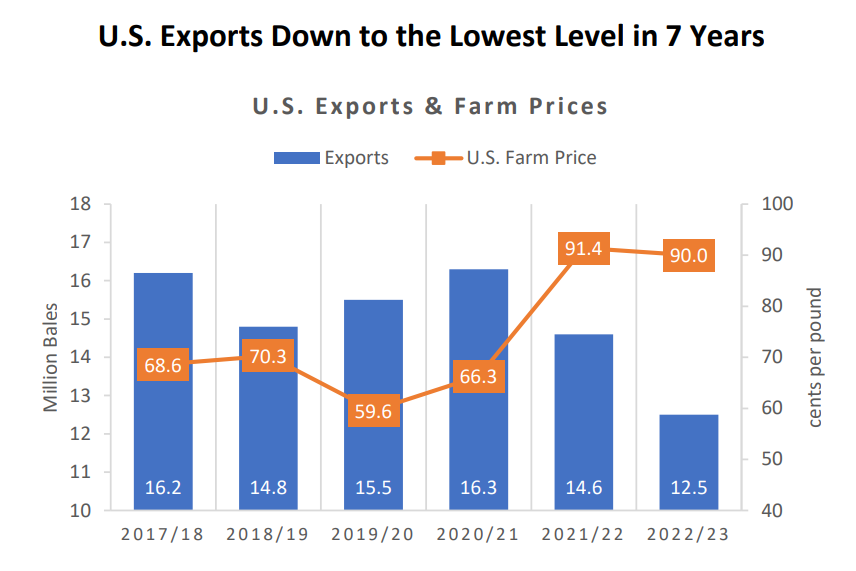

Meanwhile, I am also expecting the production volume to trend upwards. Below is a view specific to US, but it is relatable to Himatsingka as it consumes american cotton as well.

Most of the indicators say that the cotton prices should stabilize and therefore margins should expand in another quarter.

In terms of vertical integration, it is better to assume that they are not producing significant amount of cotton themselves.

IMHO, the integrated biz model is on following aspects:

- Direct Sourcing: They may be having contracts / agreements with farmers and thereby do direct sourcing. Cotton is about 60% of the cost. So, the co is almost directly affected by cotton price as others.

- Yarn manufacturing: About half of yarn requirements are met in-house. This avoids inefficiencies in passing on cost adjustment from cotton to yarn to end products.

- Branding and private labels: This is their strong relationship with clients and also the way they differentiate themselves in the industry.

Info on sourcing cotton from partner farms (annual report)

More details on their integrated business model in the report below (section – Integrated Business Model)

2021-10-01_5300_Ashika – Stock Picks – Himatsingka Seide Ltd. – October 2021.pdf (600.9 KB)

| Subscribe To Our Free Newsletter |