After the 10% post earnings fall the stock is trading consistently below book value.

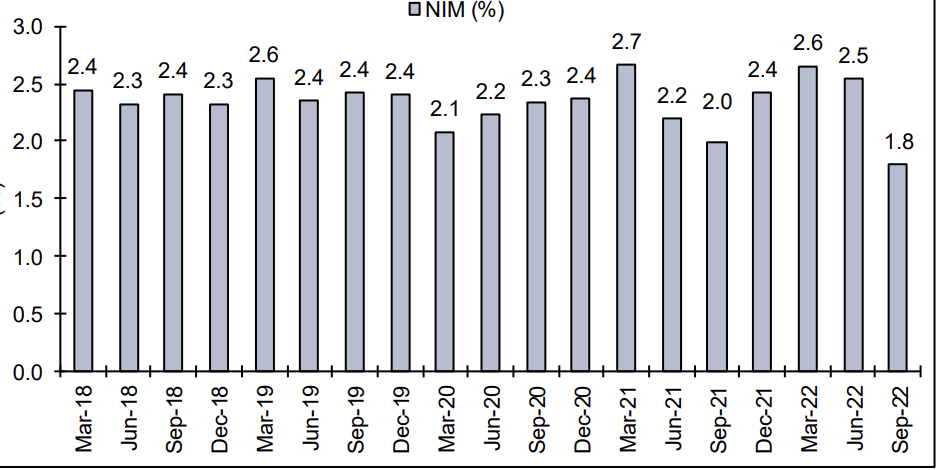

After going through a few brokerage reports (icici sec, hdfc sec, nirmalbhang ) the main concern is NIM volatility.

It is true that an nbfc will fair badly in a rising rate scenerio as the liabilities get repriced faster than the assets but that is more than factored into the prices, the company has seen high interest rate periods before has maintained its NIMs around the 2.2%

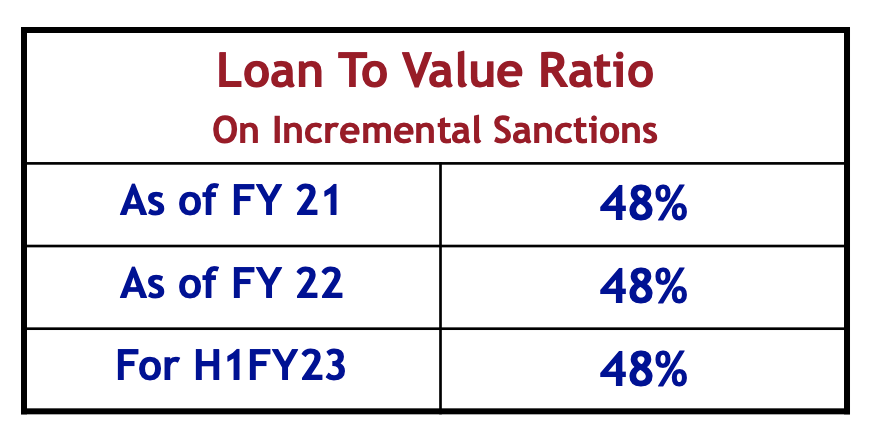

There is a risk that the 3500cr loans in OTR specific the project loans can slip in the next quater and that will keep credit costs high for the next two quarters but given that PCR is 44% and the LTV is 48% i feel they will be adequately covered from next FY with the possibility of lumpy recoveries at some point

Investment thesis is they will go back to 12% RoE in the next FY, and if you concider we are getting the equity at a 20% discount (0.8 PB) it is effectively 15%.

Assuming a 20% payout it is an attractive 3% dividend yield

the 80% that is reinvested if levered at 10x translates to a 10% profit growth

Seems reasonable

Disc: accumulating

| Subscribe To Our Free Newsletter |