Disc – I have a small allocation in Meghmani Organics, purely based on undervaluation and capex coming on stream.

One of the issues is capital allocation decision with TiO2 capex. Company will have 33K MT capacity at the capex of ~600cr.

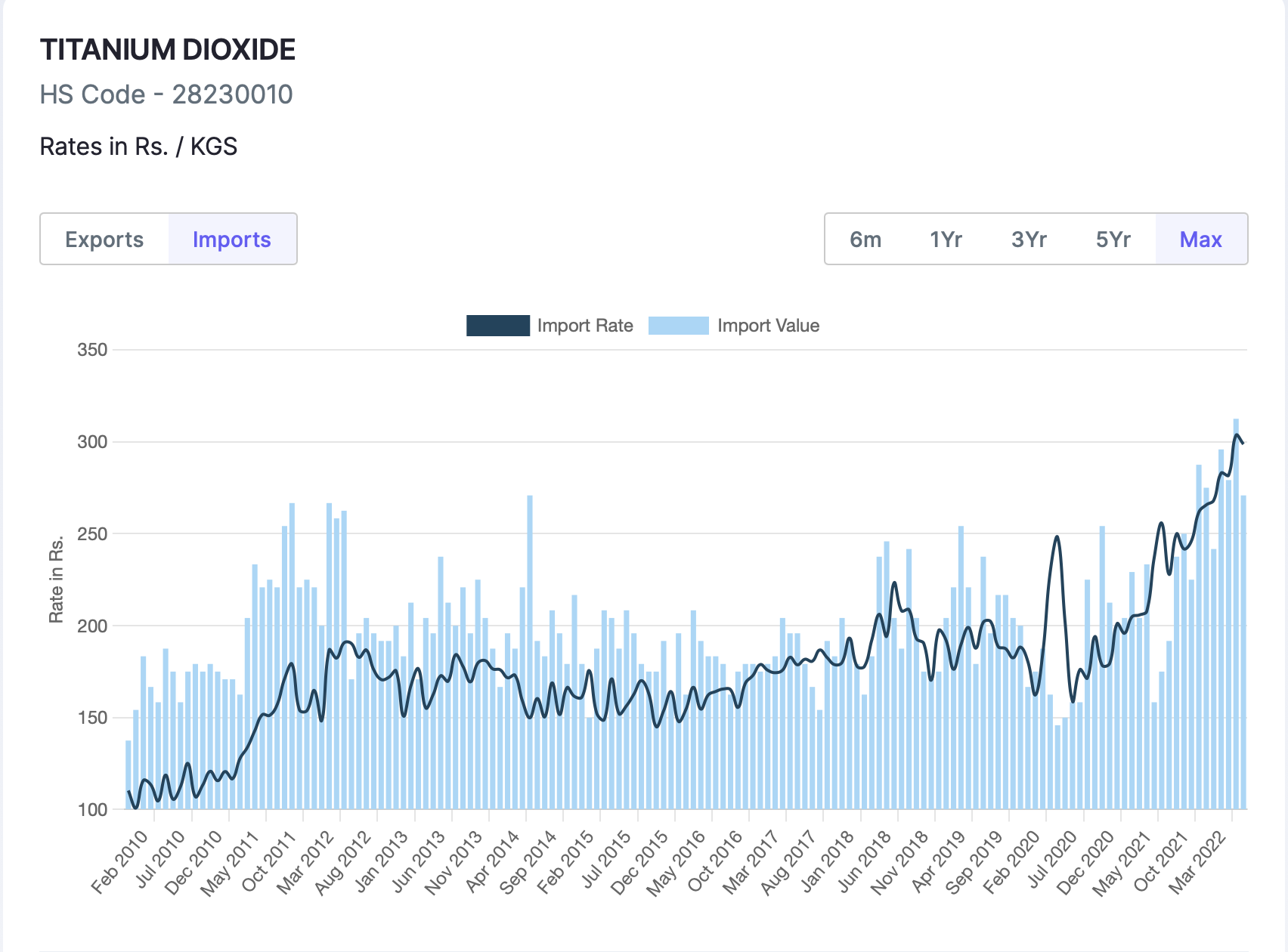

There are two grades ot TiO2 – anatese (lower grade) & rutile (higher grade). Following is realisation chart of TiO2 (rutile) grade. Long term average price of TiO2 is 200rs which went to 300rs in commodity upcycle. The prices are now correcting and they have settled at 240-250rs.

Anatese grade prices are 30-50rs lower than rutile grade prices.

At full CU, revenue of the company would be 33K * 250 * 1000 = 825cr. Assuming highly efficient net working capital cycle of 2 months, WC requirement would be 825cr/6 = 135cr.

Total capital employed – 600cr + 135cr = 735cr.

To get 15% ROCE, company has to make PBIT of – 110cr i.e. PBIT margins of 13-14%.

Assuming very less depreciation of 40cr, EBITDA of 150cr i.e. EBITDA margins of 18%.

If one wants to make 20% ROCE, required EBITDA margins are even higher.

If WC goes to 3 months, margins have to be higher.

Optimum CU will be 85-90% and not 100%.

Company will make anatese grade of TiO2 first which has lower realization and hence lower margins/ROCE.

Overall, it is quite clear that TiO2 will be a drag on capital efficiency and ramp up will be gradual. Eventually whether it will generate 18-20% ROCE is not yet fully settled.

Further, capacity in China is 46L MT and buyers for TiO2 will be 5-6 really large players who will try to extract as much purchasing discount as possible.

Some support in the form of PLI, ADD will help to make this business capital efficient. Otherwise, it remains a poor/average capital allocation decision.

| Subscribe To Our Free Newsletter |