HBL POWER SYSTEMS STOCK STORY

ELEVATOR PITCH

• Focus on niche technology based solutions with large opportunity size and limited competition eg. TCAS is a pretty large opportunity with only 3 approved players and a almost a 3 year lead time for any new player to develop the same – and that too at a significant lesser cost compared to other MNC cos c. 50-60 lakhs/km for Indian companies vs Rs 2-3 for MNCs. Similarly in PLT Batteries – HBL is the only Indian company to manufacture PLT batteries – for use in data centres etc. Electronic interlocking is another space with limited competition.

• Better Product mix to lead to higher margins – Electronics likely to command much higher share than batteries in 3 years from now, and even within batteries – share of commoditized telecom lead acid batteries to decline and share of specialized PLT and defence batteries to increase – resulting in overall higher margins

• R&D Intensive business – R&D on products like TCAS, PLT has been done by HBL for over 15+ years – and is likely to bear fruit over next 2-3 years and hence not easily replicable by anyone else – high entry barriers.

CURRENT MARKET/INDUSTRY TRENDS

• Atmanirbhar in Defence – Indigenisation of Indian defence sector eg. Indian Navy plan detailed at https://www.ddpmod.gov.in/sites/default/files/INIP%20(2015-2030).pdf which mentions only 2 Indian companies as suppliers for submarine batteries – HBL & Exide

• Railways capex – Large capex being done by Indian railways – suggests TCAS rollout likely to be fast with c. 2000kms this year and c. 4000-5000kms+ every year thereafter, across 60,000 kms+

• Z

BARRIERS TO ENTRY

• X

• Y

• Z

• A

• B

• C

BUSINESS MODEL

• X

• Y

• Z

• A

• B

• C

INTERESTING VIEWPOINTS

- In the National Budget of 2020-21, the Government allocated 7,500 Crore for installing

TCAS over 25,000 route kms (out of a total railway network of 67,956 kms) in 16 zonal railways. [1]. For many years, TCAS was competing with European solutions like ETCS L1 and L2. FY21 saw this competition being put to an end, with the discovery of total cost of ownership and overall value proposition of TCAS as superior. It was named as

the National ATP system for India. - The FY21 National Budget provided an allocation of I 3,450 Crore towards installation

of TMS and CTC in 1,646 stations (out of total 7,349 stations) of the Indian

Railways network. [1] Significantly, unlike TCAS (3 RDSO approved Indian Vendors) HBL reportedly is the only approved TMS Indian Vendor for Indian Railways. Alstom’s ICONIS platform is the other known Integrated Train Management System (TMS) installation in Eastern Dedicated Freight Corridor (EDFC) Operational Control Centre. HBL has also own orders from Siemens for TMS installation in Eastern DFCC project (probably in Kanpur-DDU section) - Commenced manufacture and supply of Type I batteries for Kilo class submarine and Varunasthra DRDO designed submarine heavyweight torpedo batteries to Indian Navy. 250-300 KW Silver Oxide Zinc (AgOZn), both primary and secondary batteries for Varunasthra torpedo propulsion Further batches will be delivered during the current year in periodic intervals until the order is complete. [1]. The team also developed and successfully received product approval for Type IV batteries for Scorpene class submarines.

- it intensified its development efforts of new products such as the EV drive train system, batteries for light & heavy weight torpedoes, Type II batteries for HDW class submarines, among others. [1]

- Absorbed technology from NSTL (Naval Science and Technology Laboratory) for manufacture and supply of Lithium-ion batteries for defence applications [1]. We have set up a pilot plant conforming to the requirements of the NSTL. This paves the way for HBL to develop Li-ion batteries for various defence applications. Is this for High Capacity Lithium Ion Battery Technology HCLBT MK-II 200 Ah Cell?

- Kilo and Kalvari class submarines to get next-gen lithium-ion-batteries. Who’s the Vendor? HBL?

- Secured product approval from the Indian Army for PLT batteries for use in defence

vehicles. Delivered the first batch of battery for use in vehicles that run in sub-zero

temperature in Leh-Ladakh. Enhanced export volume of PLT batteries for battle tank

cranking application [1]. HBL Total installation base of PLT batteries in Data Center application in excess of 100 MW (should have gone up to atleast 200 MW in FY22?) - Silver Oxide Zinc Storage Battery

https://www.drdo.gov.in/sites/default/files/2021-10/TA-605.PDF - Ni-Cd Aircraft Battery

https://www.drdo.gov.in/sites/default/files/2021-10/TA-2011.PDF - VLRA Battery

https://www.drdo.gov.in/sites/default/files/2021-10/TA-2005.PDF

*Use of lithium ion batteries in submarine

India to tap ‘Lithium Triangle’ for Lithium-ION batteries onboard Indian Navy subs | The Financial Express

BULLISH VIEWPOINTS

There are a couple of opportunities in HBL Power that look very attractive, summarized below:

1. TCAS/Kavach

• HBL Power has been approved as a vendor by Indian Railways for Kavach (TCAS- Train Collision Avoidance System). Kavach is an indigenous automatic train protection system developed by RDSO under the railway ministry and has been under development for 10+ years. Components of system are depicted below – key ones being Loco TCAS, Stationary TCAS, RFID readers etc.

-

Why is it attractive? This project is likely to be a reasonably high margin product given that:

- It is a very large opportunity – Kavach is expected to be deployed across 68,000 kms by 2028 and thus potentially a 30,000 crs+ opportunity, with c. 2000kms expected for FY 23 and 4000kms/year thereafter.

- There are only 3 companies approved as vendors for Kavach – HBL Power, Kernex (listed) and Medha Servo Drives (unlisted). Any new vendor will take atleast 2-3+ years to get approved, thereby limiting competition.

- Of the total cost, significant part is on the technology related part – railways electronics/systems c. 70%, and cost component related to cost, license cost etc. is pretty low.

Source: https://ncr.indianrailways.gov.in/uploads/files/1646997292370-Kavach%20A%20new.pdf

o Medha Servo is an unlisted compay with topline in last few years of c. Rs 1500-2000 crs and base business has EBITDA margins of c. 20%. It is very unlikely that they would incur development costs in a project like TCAS for over 10+ years if expected margins in the same weren’t significantly better than their base business.

o To summarize, the set-up is perfect – A large opportunity in a specialized product an oligopolistic set up with visibility of no more competition at-least for 2-3 years.

-

Recent updates:

- HBL received their 1st order in FY 20 for 350 kms which is currently under implementation. Next set of tenders totalling 11 in number across c. 3000 kms have been rolled out (Delhi-Mumbai and Delhi-Howrah) and expected to be awarded over next few months.

Refer attached document which clearly shows that TCAS for c. 8000kms is already signed off. With orders for this year already announced, this document provides clear visibility for next year as well.

2. Electronic Interlocking

Opportunity size:

- HBL is ready for field trials of electronic interlocking after successful testing by RDSO (as per AR FY 22). This seems to be a large opportunity with electronic interlocking at c. 1550 stations over next 3 years (Source: https://pib.gov.in/PressReleasePage.aspx?PRID=1727213). Indicative cost for interlocking is c. 10 crs per station on average) translating to an opportunity of c. 5000 crs / year and execution time frame of 9-15 months across contracts.

Source: Various tenders

• IRCON invites tender for electronic interlocking based signalling system at various stations in connection with doubling work in Katni-Singrauli section – Rail Analysis India

o 10 stations 131 crs design supply installation testing commissioning

• IRCON invites tender for electronic interlocking system and S&T works at various stations of Danapur division of East Central railway – Rail Analysis India

o 4 stations 50 crs – design supply installation testing commissioning

• MRVC invites tender for the work of electronic interlocking system and indoor and outdoor signalling works at Juinagar station of Mumbai division of Central Railway – Rail Analysis India

o 1 station – 8.5 crs design supply installation testing commissioning

• Indian Railways’ PSU, RailTel to implement modern signalling projects worth Rs 224 crore on Northern Railways | The Financial Express

o 26 stations costing Rs 224 crs

Number of players

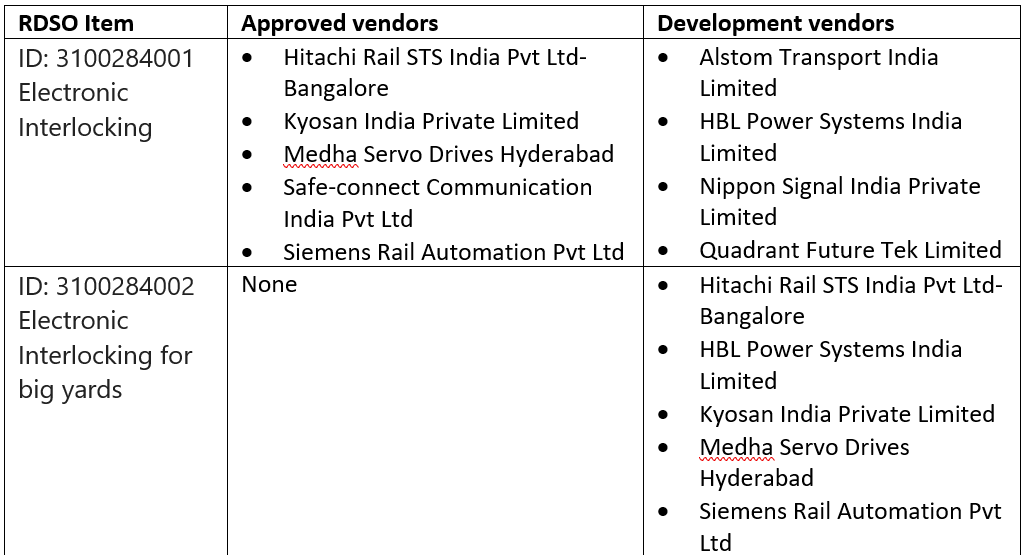

• This technology also has been in the works for c. 10 years and is limited to few players. A look at the vendor approvals for electronic interlocking shows the following:

We have not been to establish yet the split of opportunity between regular electronic interlocking and electronic interlocking for big yards.

HBL’s approval status

HBL has received provisional approval for field trials for 24 months with supply limited to 10 systems. Supplies beyond the field trials quantity shall commence only after successful completion of the field trials for 10 Numbers, over 3 months period, and for 30 equipment months (after fitment).

What does this translate to for HBL?

On a conservative basis, 5000 crs / year divided amongst 10 players can potentially be c. 500 crs/ year kind of opportunity on average. EI for big yards can potentially be even larger with only 5 players involved. The important thing to note that this too is a niche technology space with limited competition where HBL is going to compete with primarily MNCs + Medha – but 10+ players can potentially kill the margin.

Unanswered questions on EI

- Reaffirm the opportunity size 1550 EI across 3 years with cost of c. 10 crs = 15000 crs?

- Split between EI and EI for big yards?

- Reaffirm the field trial period – is it 3 months – can it start in few months from now?

- What kind of margin opportunity? With 10 players will margin get killed? Or is it a low capex business where with higher demand margins can still be ok?

-

HBL prefers to do business where only 2-3 players are present so why EI then?

Why doesn’t Medha sell this internationally? Taiwan?

**3. PLT Batteries Opportunity Size

Potentially this can be huge. Reportedly at 150 Cr Sales FY22 can scale up rapidly?

- Jio plan is to deploy 400 MW capacity DC over next 3 years. There will be at least 4 100 MW bid DC. Nagpur, Jamnagar and Mumbai and Kolkata are prime locations. Class 5

They will have many MEC (Mobile Edge computing…DC will move from code towards customer … …at edge) sites almost 42 where the DC capacity will be around 25MW. …Class 4. 42 MEC sites will start with 5 or 10 MW and eventually grow to 25MW over 3 to 5 years.

As per Cisco Delivery Head – one can assume investments will trigger in 2023 …they have to deploy close to 800MW in 5 years …either alone or alone with Azure Data Centres.

@Anant to explore with MSFT seniors

Data Centre Tiers explained

Tier 5

Tier 5 is a relatively new standard in data center requirements. Tier 5 data centers must meet the same standards as Tier 4, plus several additional ones. For example, they must be able to run forever without water, have outside air pollutant detection (and be capable of initiating a protective response), have permanently installed stored energy system monitors, securable server racks, and much more. Furthermore, Tier 5 data centers are required to run on local, renewable power projects.

Tier 4 vs Tier 5 DC – Nice comparison table for Tier 4 and 5

-

Risks

- Slow rollout: As of FY 22 end, Kavach had been implemented on c. 1450 kms and orders for c. 2000kms expected in FY 23, and 4000kms annually thereafter. Any slowdown in rollout from the government can impact the business case here.

- Commodity price increase: Understand that there is no commodity pass through under the contract and thus any material changes in commodity prices can adversely impact the margins.

- Failed execution: HBL has a track record of excellent R&D but failed execution and monetization of the same.

• X

• Y

• Z

• A

• B

• C

BEARISH VIEWPOINTS

KAVACH

-

Slow rollout: As of FY 22 end, Kavach had been implemented on c. 1450 kms and orders for c. 2000kms expected in FY 23, and 4000kms annually thereafter. Any slowdown in rollout from the government can impact the business case here.

-

Commodity price increase: Understand that there is no commodity pass through under the contract and thus any material changes in commodity prices can adversely impact the margins.

-

Failed execution: HBL has a track record of excellent R&D – One look at Annual reports of last 10 years gives a colour of their expertise in R&D – but they have failed at execution and monetization of the same. This has changed now in the last 3 years wherein one can see significant increase in Gross and operating margins, better cash flows and lower debt.

Nickel cadmium battery market is a saturated market – facing overall decline of c. 5% p.a.

• PLT foray – 150 Cr in FY22? (to investigate contours, try and demystify the “hype”)

Data centre applications is the main big scale-up argument here. However EnerSys docs point to the compelling argument versus competing Li-on being TCO and OPEX and NOT per se the technology talking points. Need to investigate Like-to-Like Lion vs PLT configuration costing/trends – to understand if TPPL advantage is long-lasting or not

TCO of Lithium ion batteries is 2.5-3.0x of PLT batteries and convertibility / usability is easier in PLT compared to Lithium ion (which needs a BMS). TPPL batteries are useful in data centres. More deatails here:

Why choose TPPL

- One quick way might be through Data Centre Operatirs liek ST Telemedia and others. They might have both Lion and PLT packages to offer to Data Centres for backy=up solutions? https://analyticsindiamag.com/the-top-data-centre-operators-in-india/

https://www.linkedin.com/in/vipin-jain-36b7635

Vipin Jain is the Guy. Many of my contacts know him from Tatas/Telstra days. Will check who knows him well and set up a call

• Li-On Cells foray – 100 Cr Investment – (to investigate contours, try and demystify the “hype”)

Given HBL’s operational/process-efficiency track record, this is another concern area given how competitive this space is likely to be in the near future.

-

Maruti is starting localisation of Lion cells and purchasing these batteries from fellow subsidiary TDSG, Suzuki’s JV with Denso and Toshiba in Gujarat, for both in-house use and export. Maruti will export battery packs to Suzuki’s European subsidiary Magyar Suzuki and the amount will not exceed ₹1,500 crore in a financial year for the period beginning from FY23 to FY25. Maruti Suzuki: Maruti sourcing local Li battery packs for export, home use in hybrid buildup – The Economic Times

-

Lithium-ion Battery Manufacturing in India – Current Scenario • EVreporter

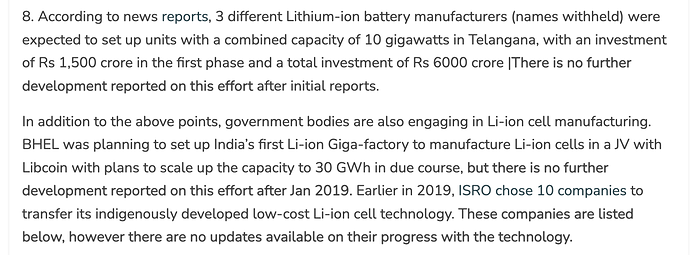

BHEL has been supplying batteries for India’s space program for over 15 years and has recently set-up a Li-ion cell manufacturing facility for meeting the requirements for the space program.(19-05-2021)

Lithium-ion (Li-ion) battery technology has the potential to bring value when integrated into UPS systems. Traditionally, data centre operators have used valve-regulated lead acid (VRLA) batteries. Li-ion batteries have high power density (up to 6 times more than VRLA), offer a long lifespan (around 20 years), highly reduce maintenance, can withstand high temperatures and offer faster recharge times to recover quicker.

Source: High performance of Li-ion batteries unlocks major savings for data centres | Saft | Batteries to energize the world

• Vodafone Data Centre – we are using VRLA+ , SMF and Lithium ion batteries in our PowerPlants and UPS’s at Data centers , So far…

We have not used TPPL so far and this technology still under evaluation phase…Above message is from SVP Vodafone

- Interesting to understand why Vodafone is evaluating TPPL technology? What led them to now?

• JIO ONE PERSON HAS CONFIRMED THAT only in DC they are using combination of PLT batteries and Li Ion batteries…but he does not have details and was not having enough info. We are still exploring about. Performance details and likely hood of future deployment…searching for people.

• Data Centre Level 1/2 requirement very different from Level 4/5 requirements

Need to quiz deeper on TCO/MW for diff levels. It might well be that Li-on is cost effective for Level4/5 and not for lower levels

- NICd is a big segment for HBL. Probably 400-500 Cr annually (even though Silver Zinc Oxide was reportedly 40% of current order book, maybe a one off year). Europe banning NiCd Battery except for very specific applications – medical, alarms, emergency lights, power tools.

Nickel–cadmium battery – Wikipedia.

Because of alternative batteries that are more efficient and the negative environmental effect of cadmium by-products from old cells and batteries, nickel-cadmium batteries are losing favour. In some areas, the use of nickel-cadmium batteries is prohibited, except for a few specialised applications. Cadmium is a hazardous metal. It cannot be thrown away in a landfill. As a result, there is a lot of pollution in the environment.

Source: https://www.alliedmarketresearch.com/nickel-cadmium-battery-market-A11699#:~:text=Because%20of%20alternative%20batteries%20that,for%20a%20few%20specialised%20applications.

- good to understand the worldwide impact/trends accelerating risk?

• TCAS, TMS B2G business; slated to become majority segment in 3-4 years time

• A

• B

• C

VALUATION MODEL

CORPORATE GOVERNANCE SCAN

RED FLAGS/FORENSIC SCAN

DISCLOSURE(s)

Yachna Bhatia: Invested

Donald Francis: Not Invested, yet ![]()

BACKGROUND

HBL Power Systems Ltd is engaged in manufacturing of different types of batteries and other products. It is also engaged in service activities related to the above products.[1]

It has established itself as a leading manufacturer of batteries, electronics and engineering products based on in-house developed technologies.[2]

PRODUCT/MARKET FIT

MAIN SEGMENTS

Battery Vertical (~76% of revenues) [1]

The company is one of the large manufacturers of industrial batteries in India. It produces batteries for Telecom, UPS, Railways, Solar, Oil & Gas and power sectors. It produces various kind of batteries such as lead-acid, tubular gel, pure lead thin plate (PLT) and nickel cadmium batteries.[2]

Railway Electronics Vertical (~11% of revenues)

Under this vertical, the company primarily has 2 flagship solutions for meeting the demand requirements of railway signaling in India i.e. TCAS and TMS. They address the railway safety and track utilization efficiency aspects for the Indian Railways.[3]

Defense Vertical (~11% of revenues)

The company provides an array of products to the Indian defense. It supplies specialized batteries deployed in demanding applications like fighter aircrafts, unmanned aerial vehicles, submarine propulsion systems, torpedoes, battle tanks, missiles and artillery fuses.[4]

Revenue Breakup

In FY21, sale of products accounted for ~91% of revenues, followed by sale of services (~7%) and others (2%).[5]

Export Presence

The company has a global presence spanning across 80+ countries. It has presence in America, Europe and Middle Easy through its subsidiaries.[6] In FY21, exports accounted for ~18% of total revenues of the company.[7]

Manufacturing Facilities

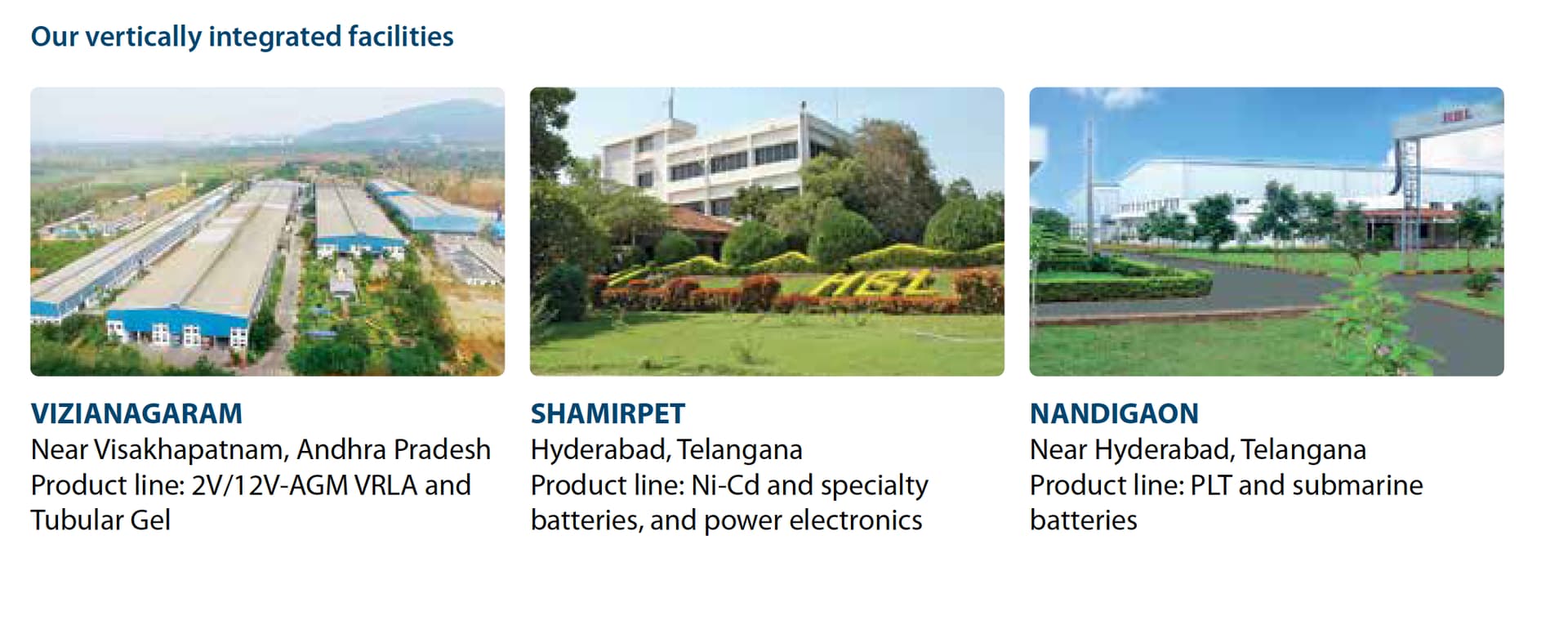

Presently, the company owns and operates 6 manufacturing plants across Telangana and Andhra Pradesh.[8]

Quality Certifications/Facilities

HBL is the first company in India to get Silver level certification (upgraded from previous Bronze level) from International Railway Industry Standard (IRIS) during the recent review

assessment by M/s DNV GL as per IRIS Rev 03 (ISO 22163 – 2017).

HBL is approved by FAA (Federal Aviation Administration, USA) for the supply of on-board

nickel cadmium batteries for Boeing aircrafts. HBL is also an OEM supplier of on-board nickel cadmium batteries for aircrafts manufactured by Airbus, IAI (Israel Aerospace Industries), and Bombardier.

The Company’s central test facility at its Shamirpet campus is the only NABL accredited laboratory in India (as per ISO 17025) with the facility and capability of testing all the applicable tests of IEC 60623: 2017, IEC 62259: 2003, IEC 60896 : 2004 and IEC 61427:2013

Scheme of Amalgamation

In FY17, the company issued ~2.4 crore equity shares of Face Value Rs. 1 each as per the scheme of amalgamation of Beaver Engineering and Holdings Pvt Ltd within the company. It was the holding company of HBL with equity holding of ~59%. The rationale behind the merge was to enable shareholders of Beaver to hold listed shares of HBL, simplify the group structure, de-leverage the financial statements and enhance floating stock of shares of the company.[9]

Sale of Subsidiary

In FY14, the company sold its entire ~62% stake[10] in its subsidiary Agile Electric Sub Assemble Pvt Ltd for ~175 crores[11] It also booked a profit of ~62 crores on the sale.[12]

Agile Electric was involved in the production of DC and AC motor sub assemblies. It was sold to Blackstone Group.[13]

Sources:

- TCAS Handbook – April 2021 (here)

- Kavach Dashboard (here)

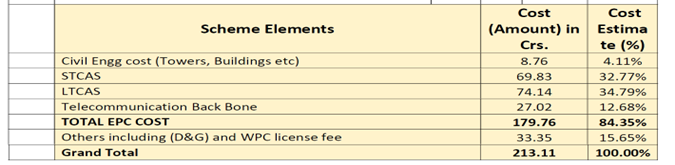

- Cost Breakup of Kavach Work (here)

- HBL Wire – Jul 2020 Issue 03

- HBL Wire – Sep 2020 Issue 04

- HBL Wire – Dec 2020 Issue 05

Reference:

- Kernex 2020-21 AGM Recording (here)

| Subscribe To Our Free Newsletter |