Of recently markets have been discounting good results posted by many commodity companies. Paper industry was no exception. And as @anjeshv4 has said commodity stocks prices peak before peak earnings. If you look at OPM for JK Paper they were @ 33% which is close to peak margins posted in 2019. In addition to the high margins, most of the capacity is optimally utilized as well. So we may be close to peak revenue as well as margins. So can the current margins and revenue be sustained?

Major Indian integrated paper companies benefitted from the very high pulp prices. JK Paper buying almost all the wood that it require from its own adjoining plantations through contract farming. At a time when most commodity companies are hit severely due to raw material costs, Indian integrated players are at a sweet spot due to their farming operations. Utilization levels of JK paper was always very high close to 100 % even in bad cycles. It was the usually the landed cost of imported paper that played the spoilsport for Indian Paper companies. With high freight rates and high pulp prices the landed price of imported paper is stay high atleast in the short period. China banning import of waste paper had a severe impact on paper pulp prices, which doesn’t seem to be going down any sooner.

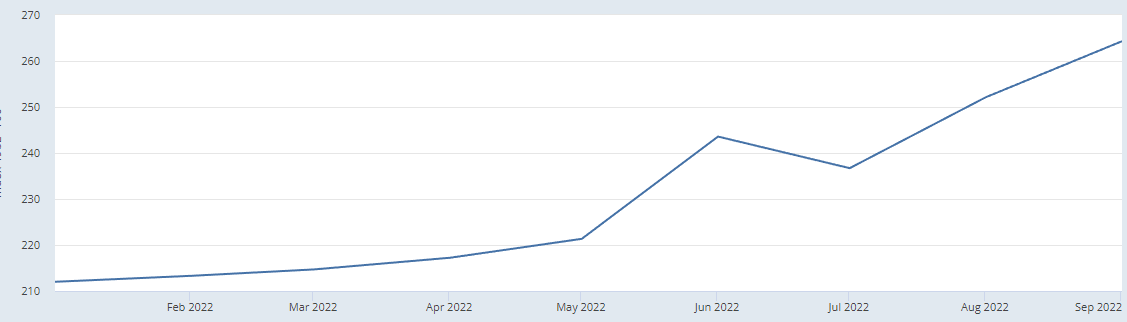

Infact pulp prices are continuously going up.

Eventhough all its capacities are optimally utilized now, the corrugated paper capacity may come up in a couple of quarters. There is a CWIP of 115 crores in balance sheet as of Sept 22.

So even if prices for different paper are getting soft as per news, I dont see prices going down sharply due to the high pulp prices. So margins may stay high.

Also company had an EBITDA of 500 crores, and Market cap/ EBITDA of 3.6 on an annualised basis. The company’s high debt of 2900 crores may have been an overhang on the stock price. With much improved cash flow and repayment in debt could lead to better market cap eventhough enterprise value remains the same.

Discl: No investments. exited way too early

| Subscribe To Our Free Newsletter |