Can anyone explain the above resolution in simple language?

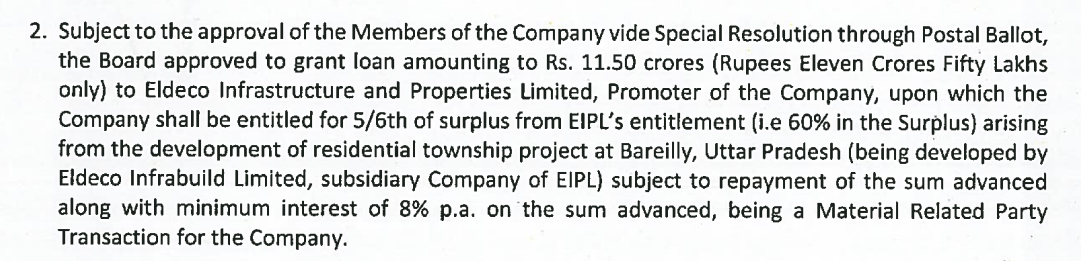

Is the company loaning to the promoter? If yes why? What kind of business is this ![]() ? Also, how is 5/6th of surplus related to 60% in the surplus?

? Also, how is 5/6th of surplus related to 60% in the surplus?

-

Revenue Rs. 109Cr in FY18 vs Rs. 127Cr in FY22.

-

PAT Rs. 24Cr in FY18 vs Rs.50.8Cr in FY22.

Is it sustainable to grow profit without growing revenue in this industry?

Last 5 Quarters PAT and PAT margin has been falling.

35 Subsidiaries and only 6 are profitable. Omni Farms Pvt. Ltd is the only big subsidiary.

Can’t really understand the competence of the company?

In my view, the company is just selling high-priced real estate. The company is just creating many subsidiaries with negative reserves and unproductive assets.

Really doubt the company’s ability in cost-cutting measures and expertise in the technicality of building real estate. I am unable to see how these subsidiaries are maintained and why they are so unproductive. -

Standalone vs Consolidated difference in inventories is 42%.

-

Standalone vs Consolidated difference in PAT TTM is 20%.

Disclosure. Invested unsatisfied with my investment. Really doubt the real estate industry. Can’t understand the business model? The company seems shady.

| Subscribe To Our Free Newsletter |