Portfolio Update:

Not too much change since the last month. Trimmed some Raghav Productivity in response to the large gain in stock price. Some signs of euphoria there in valuations. Exited Saregama as discussed earlier and further trimmed Faze Three. Added some Ganesha Ecosphere and Axis Bank. Wish I had been bolder with my decision on PSU Banking and weighted that better; thesis there is playing out to a T. Risk reward at the time was extremely favourable.

When I look back on the last 12 months performance of the portfolio, even though it has beaten the index, I feel I missed out on a significant opportunity to compound at a higher rate. The list of stocks that I looked at, passed on and which did well during the year was extremely long. Some of them are Orbit Exports, Tyre Stocks, Raymond, Mirza Intl, Shivalik BiMetals, Maharashtr Seamless, Voltamp Transformers, Rossell (sold too early), Zomato. All were significant wealth creators during the year. The list doesnt even include stocks that were suggested to me by others and which I didnt have time to look at: Aegis Logistics, Ramkrishna Forging, Amara Raja, Varroc, Dixon, etc. I have decided to start keeping a decision journal to jot down the reasons why I decide to not buy a stock after research and see what patterns emerge over time.

The sheer volume of good opportunities identified in a fairly difficult 12 months for the market leads me to 2 conclusions:

- Great opportunities are available even in overvalued markets. You just have to work hard to uncover them

- When those opportunities are identified, you need to be courageous to act on them even if it means portfolio churn is higher. In fact, for portfolios of small size, high portfolio churn is actually preferable if it leads you to reallocate funds to ideas which have better return potential.

Hoping I dont make the same mistakes in the next 12 months and am more pro-active pulling the trigger where I am able to find good opportunities.

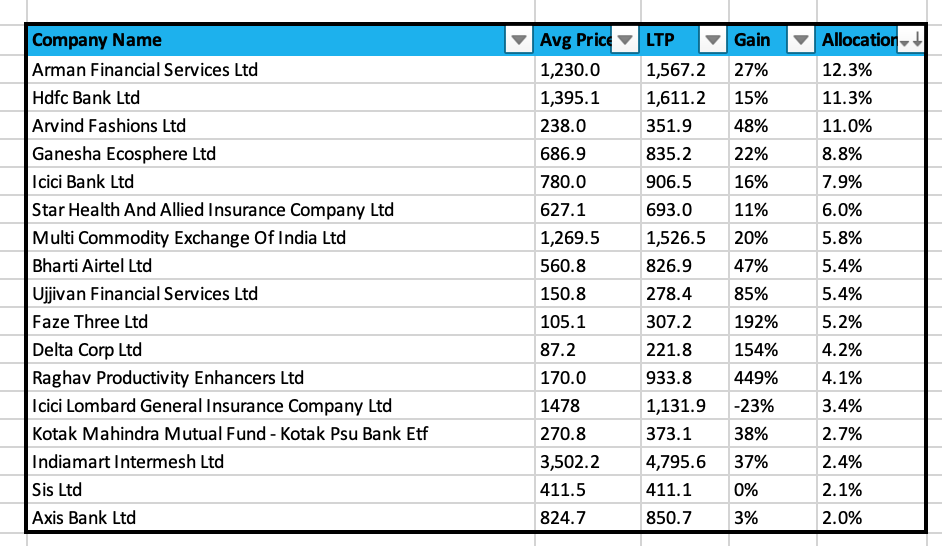

Portfolio looks as follows:

Watchlist:

Continuing to look at technology stocks. Am ready with target price for Zomato, will pull the trigger at Rs 55 though I dont think I will get that opportunity. Have passed on Nykaa: I actually think contrary to general market perception that Nykaa is the worst of the lot and will constantly require cash to grow unlike the others (being an inventory model). They also have the worst balance sheet; having taken the call of not raising money in the IPO and are consequently now funding a large chunk of working capital with debt. Doing work on PolicyBazaar now.

Also continue watching the agro-chem export basket closely. Pharma (both domestic and export) also are on my list to look at.

At the moment, I think a historically great capital deployment opportunity is available in Chinese stocks. There are a few mutual fund options available to investors. There is a general perception that Chinese stocks are ‘uninvestable’ due to geopolitics, excessive govt control, poor policies, etc and thus the entire basket as a whole has been beaten down to levels that I believe to be very attractive. One must remember that the value of a company is the discounted value of future cash flows and decide if the narratives above affect that in the long run and to what extent. In fact, even in his latest speech, Xi Jinping mentioned his support to encourage private enterprise, enterpreneurship and view to let the market play the decisive role in capital allocation. These points have been completely ignored by the global media

| Subscribe To Our Free Newsletter |