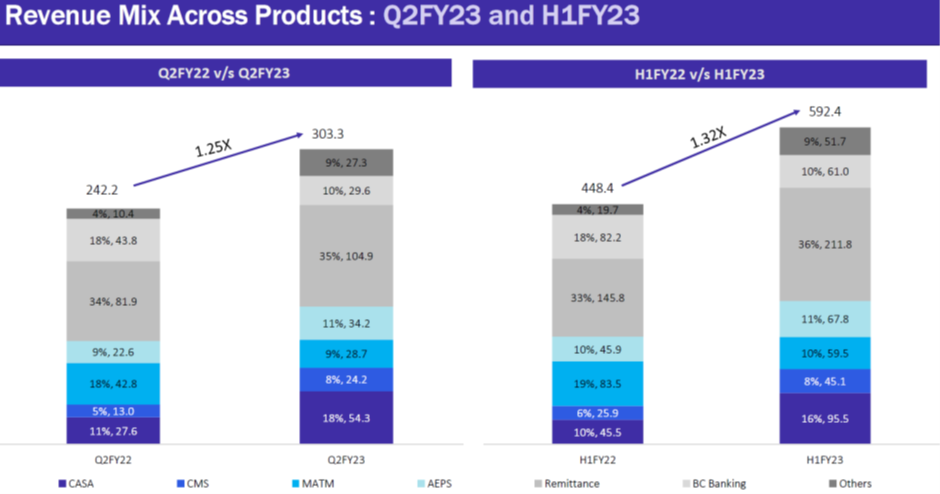

When I started initially investing in the company it was the matured services like MATM and AEPS and the population of our country that kept me interested in the company. But today, ,looking at the company the matured services like MATM and AEPS is facing severe competition from many fintech players. Share of MATM in revenue has severely gone down, from 42.8 crores to 28.7 crores. AEPS however seems to be growing at the expense of MATM from 9 % to 11 %. It was CASA and CMS that surprised the most and is now 26 % of revenues.

CASA services

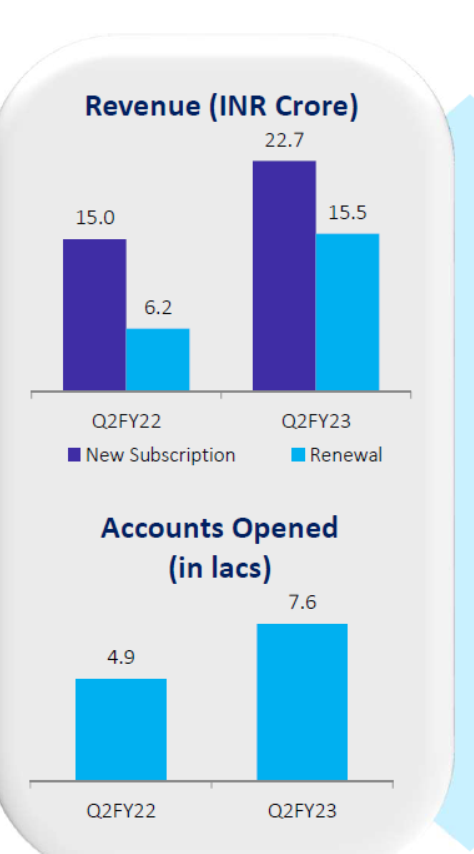

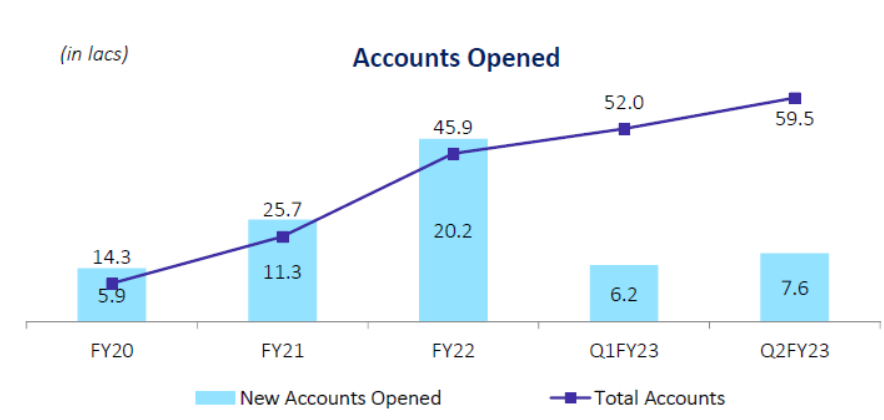

Fino is able to open 7540 accounts on a daily basis which is consistently improving.

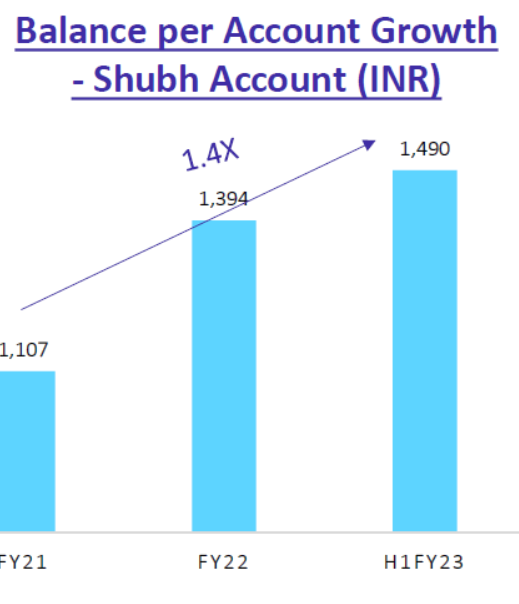

With CASA growth the amount of deposits with the bank will grow which will add to treasury income in addition to subscription income. Also with market interest rates the spread on these deposits also will grow

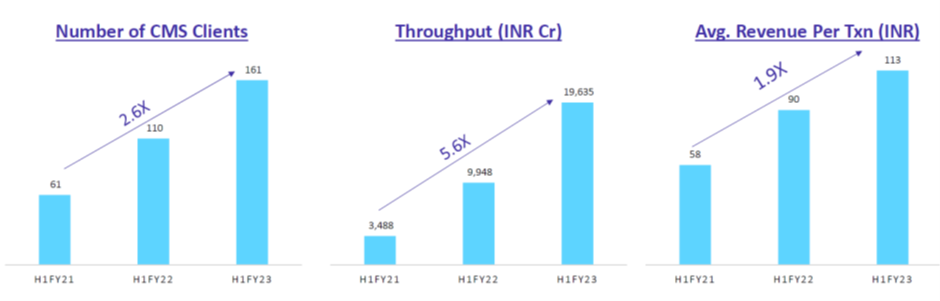

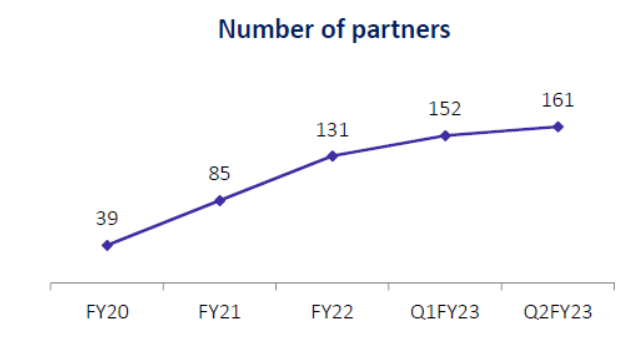

CMS

FINO 2.0

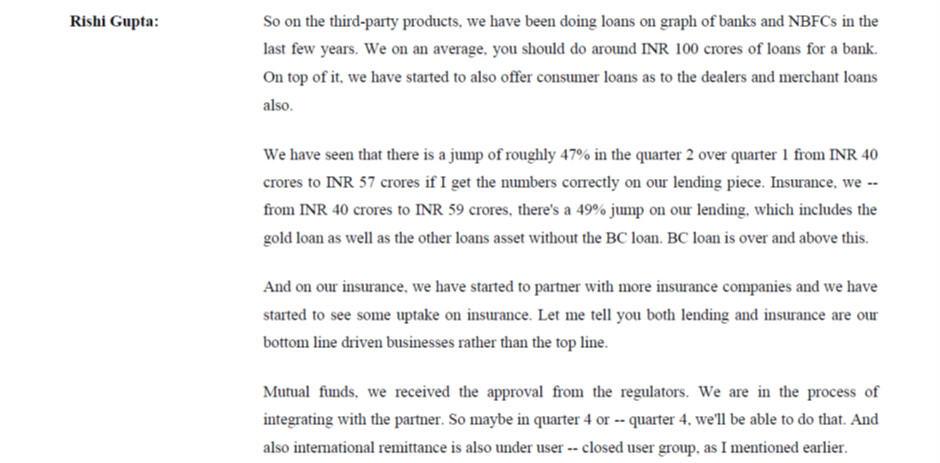

Company is speaking about transition from Fino 1.0 to Fino 2.0 wherein more and more cross sell of third party services will be focussed on esp Mutual Find / insurance, Referral loans and International remittance.

Referral loans services and insurance are expected to take off in Q4 of this FY or Q1 of next year. Peers like paytm and Airtel payments bank is talking a lot about the referral loan services whereas Fino is speaking very little about these. With such a huge clientele and phygital presence the loan referral can be a major revenue contributor. Hope to see that in FIno 2.0 atleast in next FY.

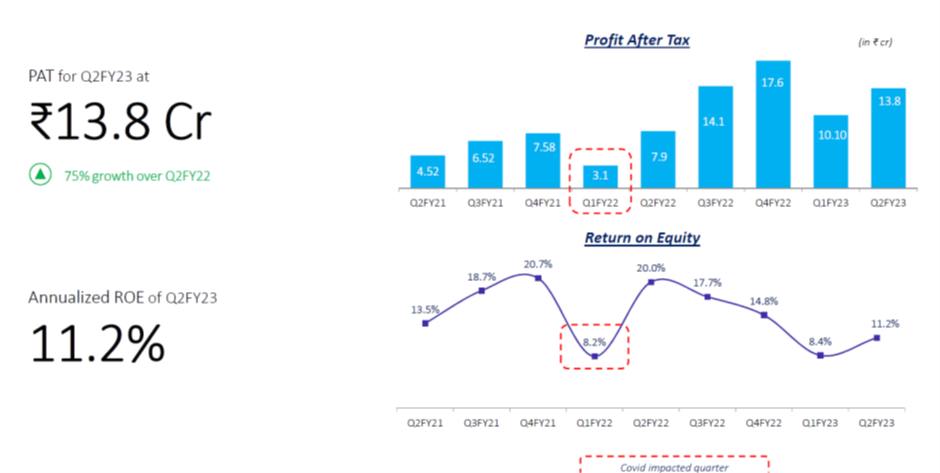

PAT has been improving continuously except for the covid affected quarter.In Q123 There was an unusual digital stack expense which pulled the PAT lower as per management . Not sure whether these continue in the current quarter as well. will have to obtain clarity on this from management.

Management is talking about transition from payments bank to SFB, will be interesting to see how that pans out in the future.

Discl: Invested and biased. Have buys in the last 30 days.

| Subscribe To Our Free Newsletter |