Hi Mudit, below is my views on valuations:

Valuation

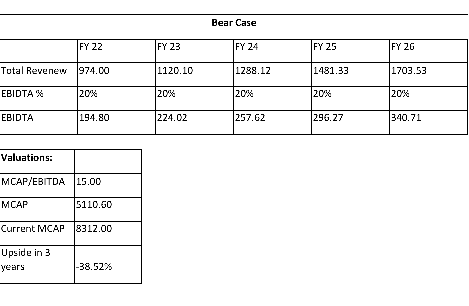

A: Bear Case

Assumptions:

- Revenue growth of 15% vs Management Guidance of 20%

- EBITDA margins Contracting to 20% vs Management Guidance of 25%

- Valuation of Mcap/EBITDA of 15 times

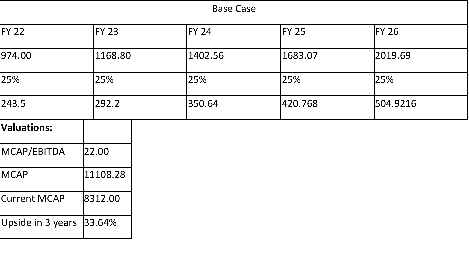

B: Base Case

Assumptions:

- Revenue growth of 20% as per Management Guidance

- EBITDA margins of 25% as per Management Guidance

- Valuation of Mcap/EBITDA of 22 times (Kims Trades @ 22)

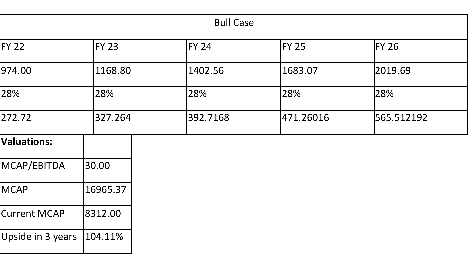

C: Bull Case

Assumptions:

- Revenue growth of 20% as per Management Guidance

- EBITDA margins of 28% because of Op Leverage

- Valuation of Mcap/EBITDA of 30 times (Max Trades @ 40)

What I think is bull case may pan out in next three years. But I want to still wait and watch (may buy small quantity 1%) 2-3 quarters as Q4 and Q1 will be seasonally low and Mr. Market may give us opportunity to add further.

| Subscribe To Our Free Newsletter |