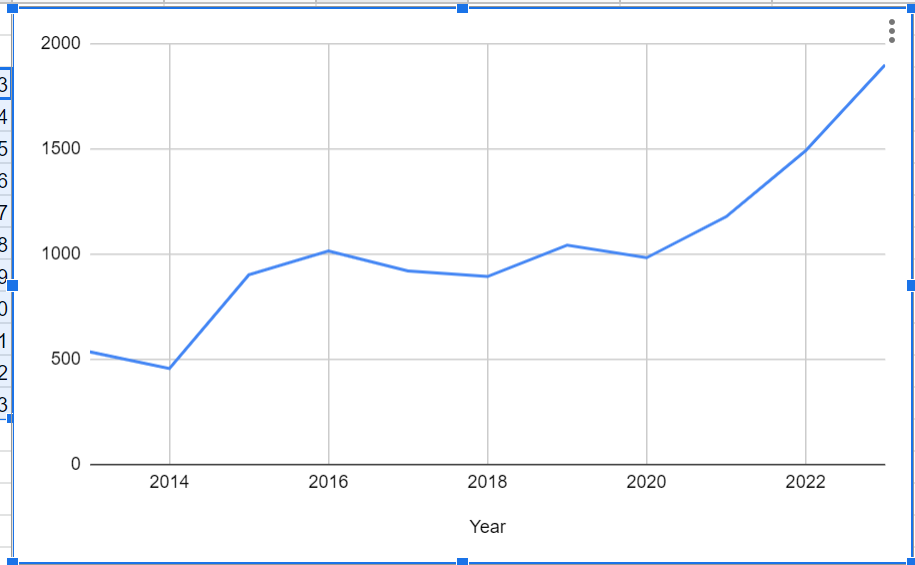

A stab at Shivalik shunt division – Volume/Value/Realization/Copper price co-relation and analysis for longer time frames to find answers/patterns

To understand – whether Shunt realization is structurally moving up or seeing some spikes inline with copper prices

- shunt realizations

- Copper prices trend in last 10 years

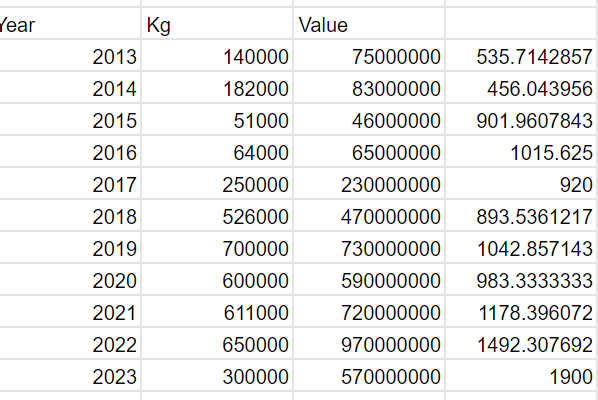

- Above analysis is based on below data – rounded off Shunt volume, value , realization trends for same set of years (only for exports and as per export data at https://tradestat.commerce.gov.in/meidb/com.asp?ie=e )

Key takeaways

-

Kg volume may not be best way to look at Shivalik as directly co-related with end product pricing – answer lies in evolving product performance characteristics and thus value. (low ohmic, tolerance range, temp range/ metal mixes etc) –

-

Shivalik realization have been on uptick over the periods irrespective of Volumes & copper prices. One way to further validate this trend would be as to how end mkt shunt prices have moved historically over years.

-

April 22 onwards Copper prices(4.5$ to 3.2$) have fallen over cliff and stayed low till Oct before bouncing back again in Nov – if there was high priced inventory – should have reflected in last 2 qtrs numbers with some pain – doesn’t seem to be the case yet – either mgmt commentary/numbers. Still better to observe in coming Qtrs.

-

50% of revenue share of lesser glamourous division, Bimetals are doing very well for shivalik (better than shunts in H1 growth) and may continue to surprise with continued client additions etc. Though this division may be more susceptible to RM price movement and impact.

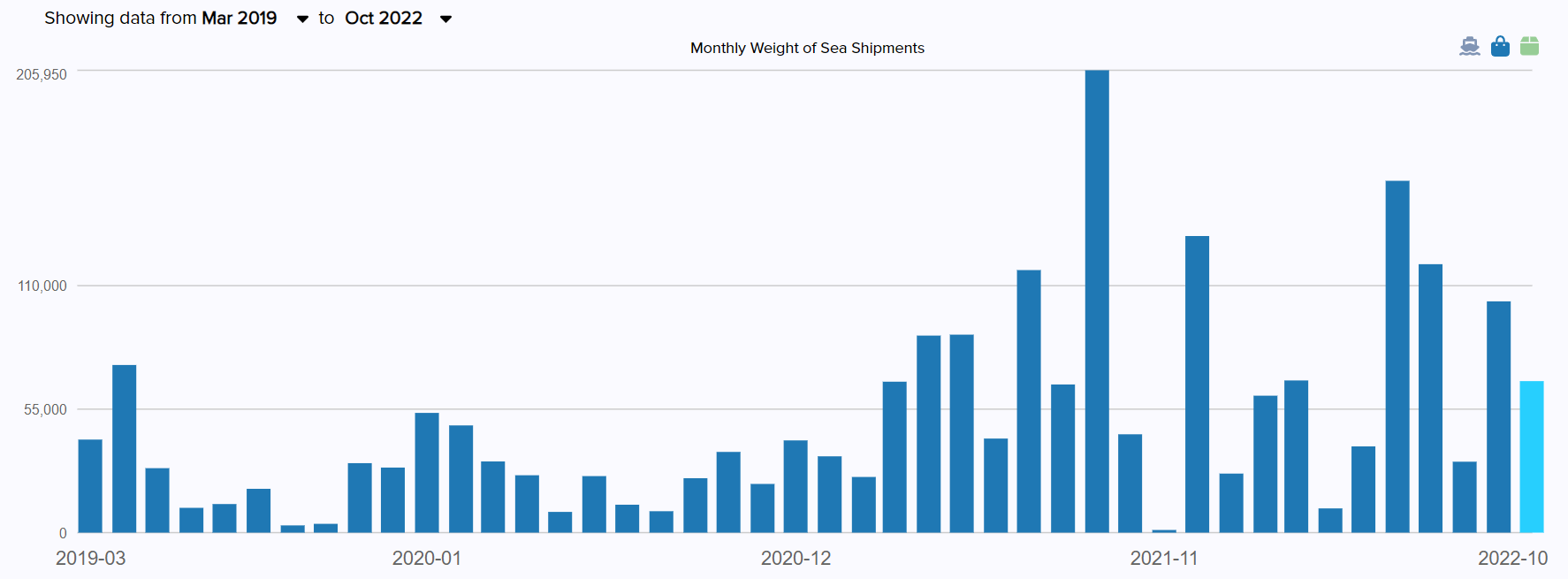

Another stab at quick reality check on Shivalik vs one of key Competition – Isabellenhutte.

Here is the last 3 years export pattern (Volumes in Kg)

Here is shivalik for same duration

note – this may not be comprehensive data and product profile may differ to some extent, idea was to see export trend and volumes over broader periods

some inferences at broad level

Volume trends

- Pre corona Isbl was in range of 25-35000 /mo – now 35000-65000/mo range

- Pre corona shivalik was 25-45000/mo , now 55000 – 110000/mo range.

Both have done well, Shivalik gains are much higher – somewhat aligns to Mgmt claims of being efficient and scalable supplier, mkt share gains.

source – https://www.importyeti.com/supplier/shivalik-bimetal-controls

Above is based on limited data & analysis and could be off/have gaps, feel free to do your own analysis and expand with additional views/points.

Though stock Price action indicates pain/doubts in line with broader mkt small cap under-performance and will test individual conviction.

| Subscribe To Our Free Newsletter |