-

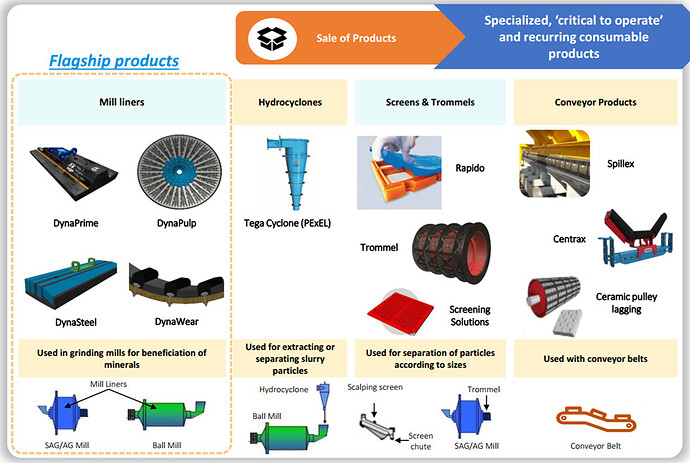

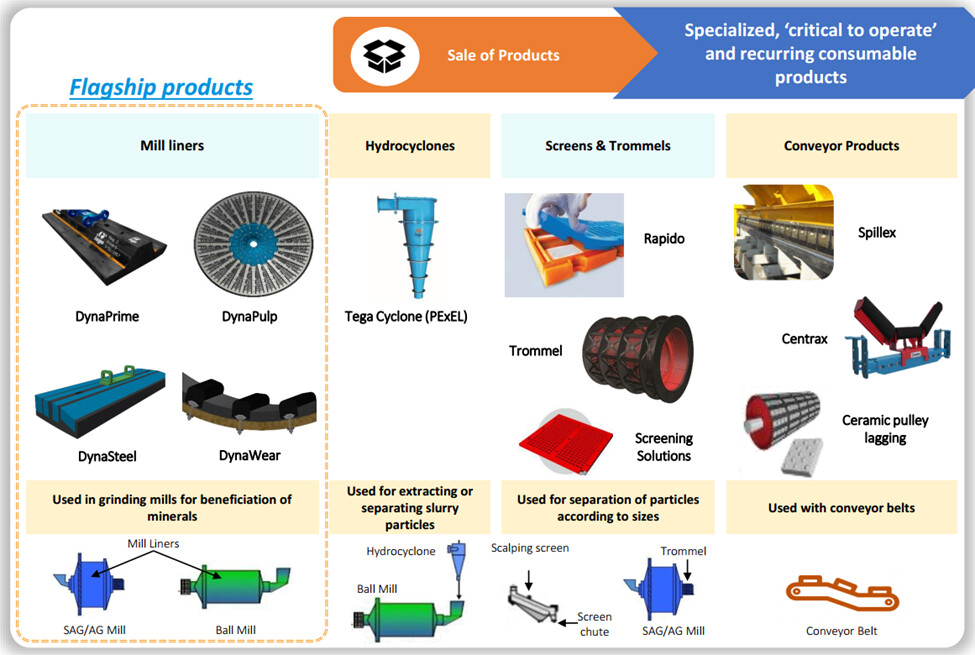

Tega is 1 of the leading manufacturers of specialized critical to operate & recurring consumable products for the global mining, mineral processing, and material handling industries.

-

The product basket comprises products (specialized abrasion and wear-resistant rubber, polyurethane, steel and ceramicbased lining components) like Mill liners, Conveyor components, Wear Resistant Liners, Screening Solution, Trommel, Hydrocyclones and Slurry Transportation

-

Industry Trend

-

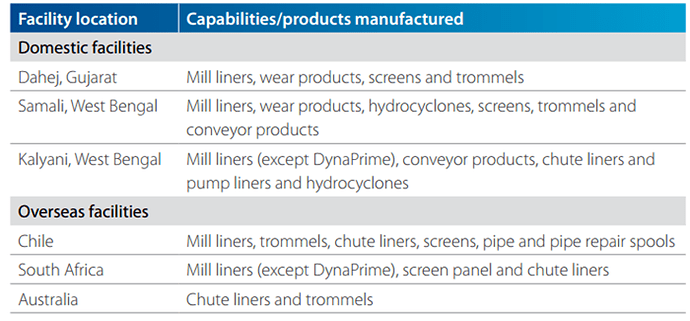

Tega is second largest producer of polymer-based mill linings as well as one of the largest players providing hybrid liners across semi-autogenous and ball mills. Operating 6 manufacturing plants across the world with three in India and three in overseas locations.

-

Almost 85% of revenues are generated outside of the country. Revenues build up throughout the financial year starting from a moderate Q1 and finishing higher in Q4. Hence the performance analysis of Y-o-Y is more relevant vs Q-o-Q

-

Strengths:

a. Immunity from mining Capex Cycles: Majority of the products are linked to the opex budget of the mining site. Thus, the company is insulated from capex cyclicality of mining players.

b. High Entry barriers: Generally, in mineral processing sites, switching costs for the customers are high on account of high cost of inital planning involved, the lead time required for approval, degree of certainty of the products of an established supplier, the high cost of downtme or shut down of a site, and relatvely lower percentage cost of components in the total opex of a mineral processing site. New customer conversion typically takes 12 months which includes six months of product trials and validaton which is a reflecton of high entry barriers in the industry. These approvals do not have any expiry period.

c. Industry Dynamics: Also, decreasing ore grades has led to a greater demand for larger-sized equipment, leading to an overall growth of 17% of the mill lining industry in Fiscal 2021.

d. DynaPrime Composite Mill Liners:

>Launched the DynaPrime range of our products in 2018. It’s a composite liner which is first of its kind in the entire world, and this has helped to unlock new addressable markets for our company, which includes larger-size mills which offers greater productivity gains and cost savings for our customers as well as almost a 50% increase in life compared to traditional steel linings.

>It is about 19% of the total revenue. Expecting it to sustain off-take at 25% compounded growth across the next five years with the objective that it account for a little less than half of our revenues by 2027

>DynaPrime has set new avenues of growth for the company by replacing existng metallic liners with an addressable market size of ~US$ 900-1,000 mn where the company’s market share stands at 2-2.5%. This is an addition to the already available opportunity of $40- 50 cr in composite mill liners market where the company’s market share is 16%.

>In FY22, DynaPrime product alone has contributed 24.1% of sales as compared to 6.7/20.4/21.4% in FY19/FY20/FY21.DynaPrime’s revenue grew at a CAGR of 75.7% over FY19-22 on a low base.

>The company expects DynaPrime’s revenue momentum to continue and grow at a CAGR of 25-30% in the near to medium-term on account of benefits it provides as compared to metallic liners. -

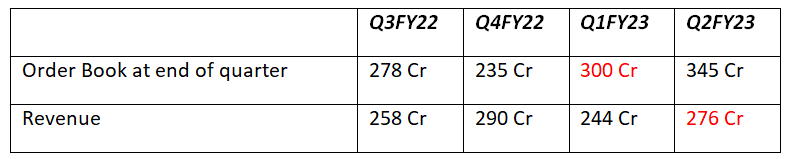

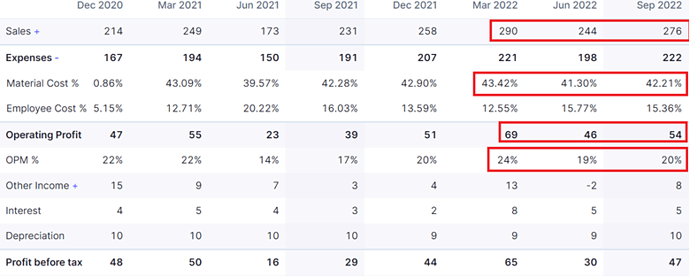

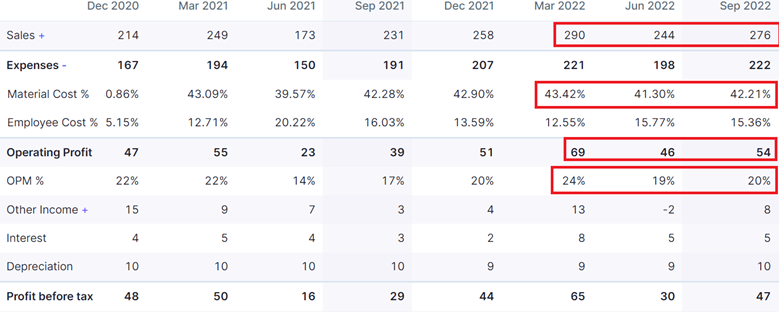

Order book and Revenue Trend. Orderbook at end of quarter is executable in 3-4 months. This gives revenue visibility

-

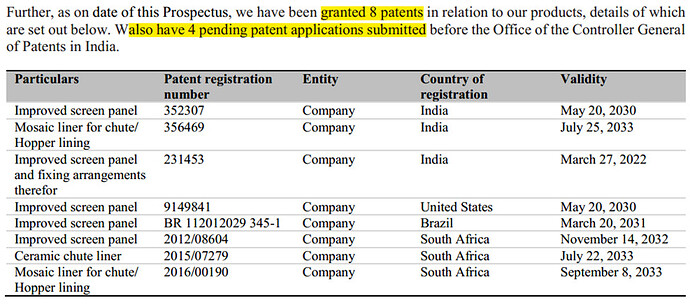

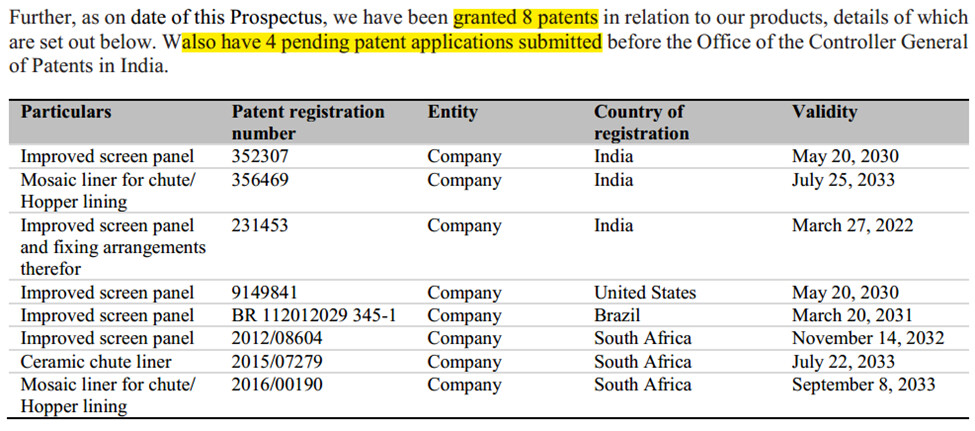

The company has patented products:

-

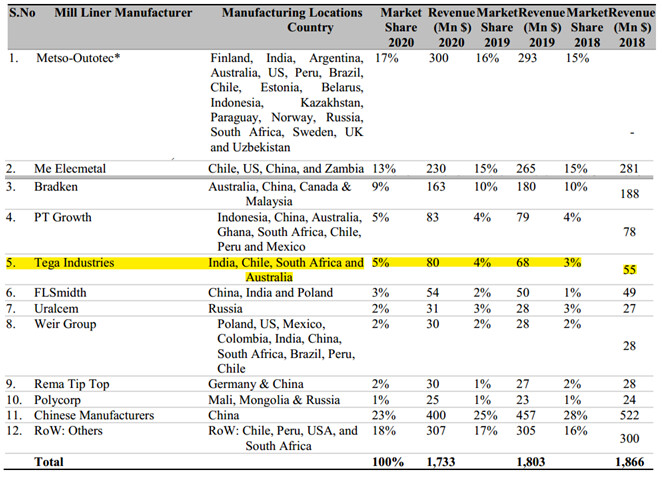

The co is targeting to gain market share from 5% at present to 7-8% in coming years. They are already gaining market share as per information in RHP

-

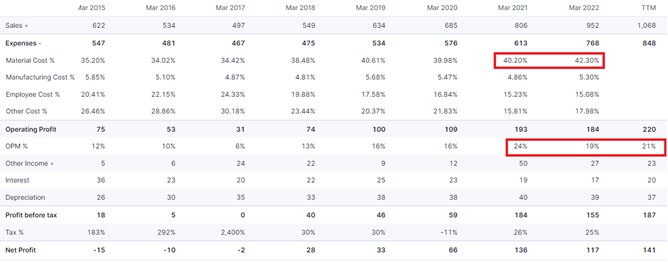

Also take a look at the past performance of the company in last few years.

-

Positive Triggers:

a. Reducing freight cost can give the profitability a boost.

b. With increasing revenue operating leverage will play out as company has significant unutilised capacity this is evident from explosive growth in EBITDA and PBT.

-

Valuation: With ROCE around 20% & TTM PE at 26 PE co seems to be fairly valued as ROCE can improve going ahead due to operating leverage. So EBITDA & PAT can rise very fast in H2FY23. The capacity utilisation was at 60% at Q1FY23 giving 400 cr qrtrly run rate capacity.

-

Antithesis:

** Peers copying Dynaprime as it doesn’t look like patented. So it can slow down the explosive growth of Dynaprime once the peers complete the development of similar products which is 2-3 years away so in the meantime Dynaprime can continue its explosive growth.

**RM Deflation reducing the top line growth offsetting the volume growth bcz company intends to keep the gross margin at 60%. Although company has not fully passed on the price hike so RM deflation will aid the gross margin to some extent. This should be asked in next concall. This might not be the case also because at Q2FY23 there was hardly any price lead growth. Someone asked in Q2FY23 concall if going ahead there can be inventory loss which the mgmt told it’s the other way around because they built up the inventory at high-cost environment

**Forex fluctuations.

**Increase in logistic costs. Though as freight cost is going down this is now turning to be a tailwind. -

Technical Aspects:

a. The Stock is still inside the IPO base, albeit the downtrend has reversed. After the breakout of the Ascending triangle it is basing again inside a rectangle while displaying some VCP (volatility contraction pattern) characteristics

b. Entry: An initial entry can be made at the breakout of the Rectangle around 590-595 levels with a SL at 508 or below the weekly breakout candle (tight risk).A breakout above 670 which is also the rectangle pattern target can be a pivot above which we can average up.

c. Finally, a breakout above the O’ Neil Pivot around 768 can be another point to average up the stock -

If you have read this far that means you are interested and have patience to dig deeper Read a more detailed research report here: https://twitter.com/TheRisingCurve/status/1594393626599047168?s=20&t=VRtBP_VmUWhRRgdiGW9r5w

-

Disclaimer: I’m planning to buy the stock based on technicals. Please do your own due diligence before buy & sell. We are not SEBI registered analysts.

| Subscribe To Our Free Newsletter |