Pricol, Monthly – 4 year bottom formation and a lot of dilly-dallying around for 6+ months this year and then getting a move on. A breakout like this generally doesn’t happen unless there’s strong fundamental shifts and a price struggle for 6 months post breakout also implies the confusion for sustenance and the belief is perhaps in the price its trading it last 3 months. This pullback that’s currently on could be a good entry for the long-term.

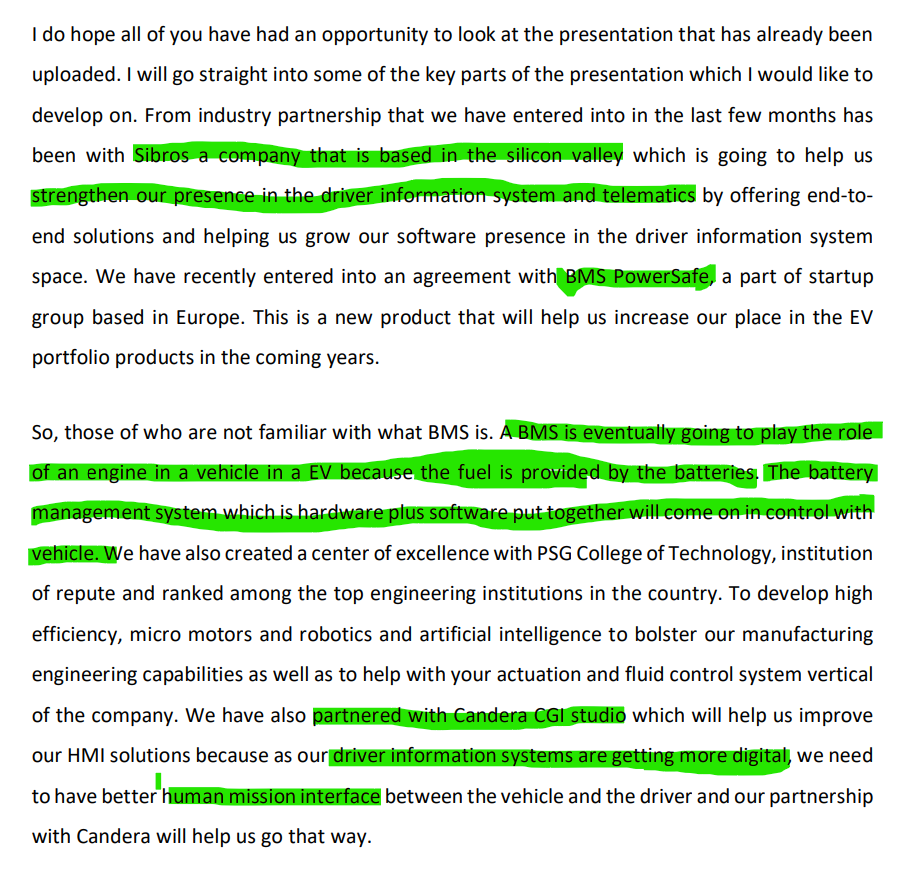

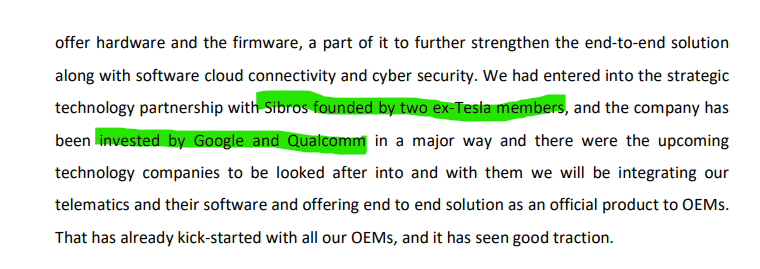

Why Pricol? The recent (this year) partnerships show the company is ambitious and hungry. Three very good partnerships – with Sibros in the driver info systems and telematics space (DIS will show everything from speedo, odo, temp, battery etc., along with ability monitor where the vehicle is remotely and also do OTA updates just like most smart devices.)

Another partnership with BMS Powersafe that gets them into the BMS space. I like how Vikram Moham the MD explains about BMS – as the equivalent of an engine for a EV (although I see it more as a ECM – Engine Control Module, which is the brain of an ICE vehicle, controlling the fuel injection, spark plugs and the firing). This gets them future ready into crucial EV components

The partnership with Candera will help them design good UX in their DIS. As the layout, the nature of colors, the design of menus etc. will matter a lot in their digital TFT screen based touch-screen interfaces, as compared to the traditional analog instrument clusters.

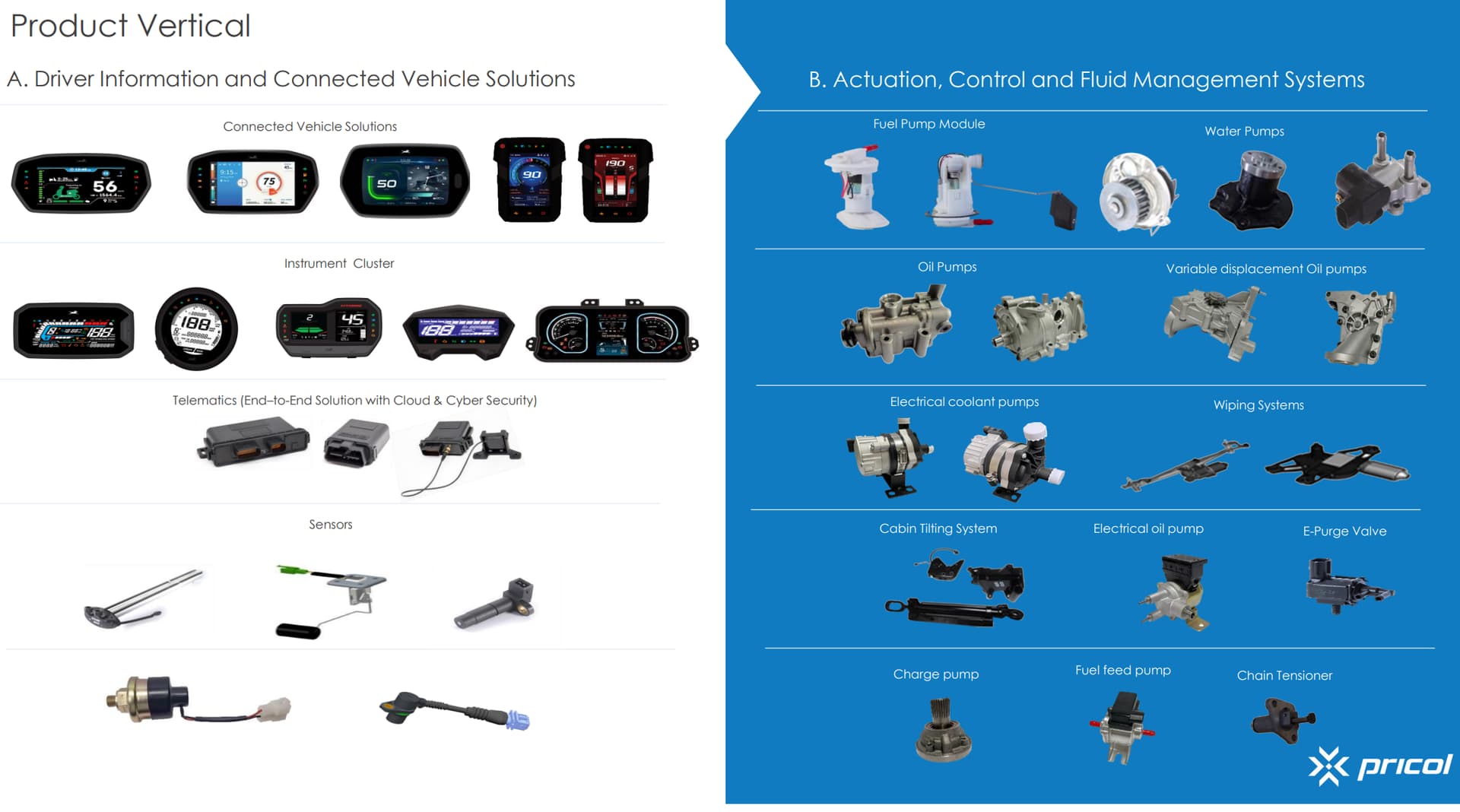

The products they make currently

Good clientele

Recent product launches

It looks like the sort of interfaces we are used to in cars, are making their way to 2W space now.

They also make instrument clusters for CVs, tractors

They also make some crucial components like Fuel pump, water pump for ICE vehicles and count CAT, Ducati, BMW, Volvo etc. among their clients in the export market

There seems to be some sort of transformation happening the business and having seen this business making auto meters and boring analog instrument clusters, its nice to see them reinvent and get ready for the future.

There is a lot of info in the concalls Q4, Q1 and Q2 and investor presentations Q4, Q1 and Q2 and the AR

The earnings have started to show up in the recent quarters but I believe the future may have a lot more to offer.

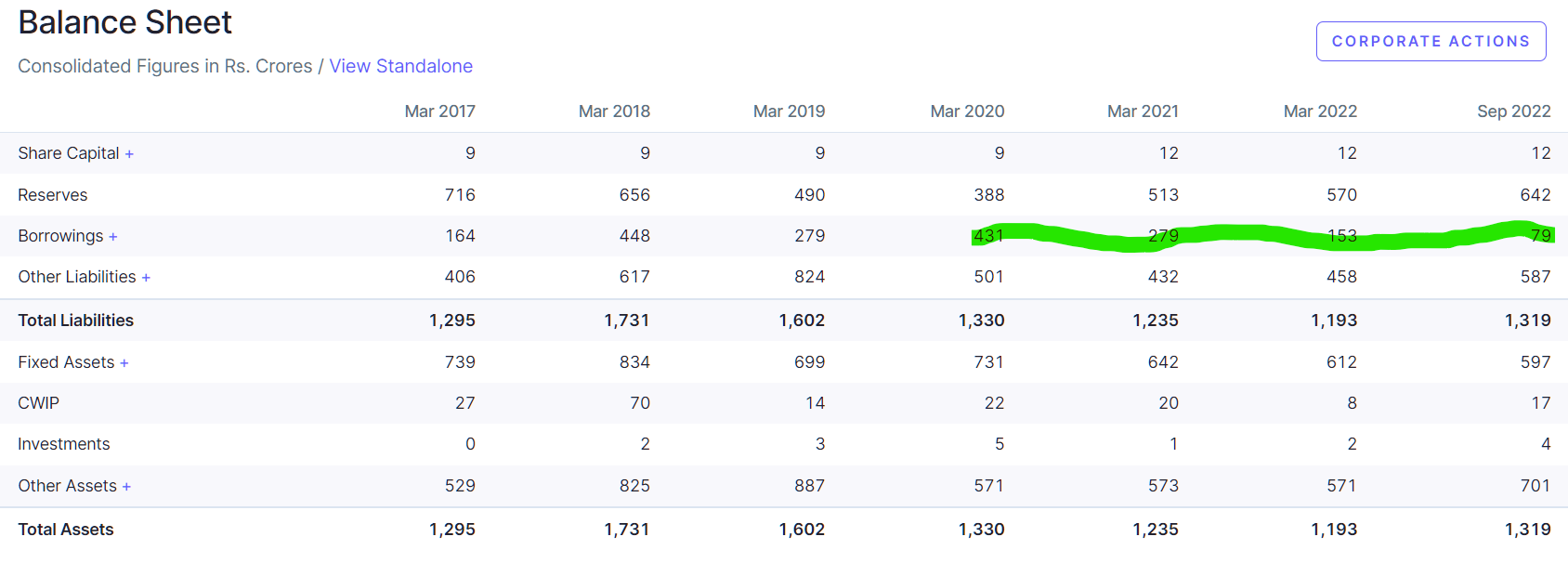

The balance sheet is lot stronger of late after they have taken some hard decisions to sell of some of their subsidiaries to re-align themselves.

The valuation at 10x EV/EBITDA isn’t very expensive for a company displaying the hunger to grow in a country with a lot of opportunities to do so. There are margin risks though in the business since a lot of the electronic components like the TFT screens are imported from China which exposes them to forex risks. There’s also risk of obsoletion of some of their products in the ICE catalog and the analog instrument clusters. However the business is perhaps in a better place today to overcome those than anytime in its history.

Disc: Have positions around 175.

| Subscribe To Our Free Newsletter |