I understand where you’re coming from, the US generics space is horrible, and the companies I’ve mentioned above are even worse. Pharmova is a soup, Aurobindo has a horrible USFDA track record and Strides has made some questionable decisions in the last year.

The way I’m looking at it is that if the US market is a commodity business, it isn’t an automatic avoid, but one should treat it as so and have strict entry/exit conditions. The worse the sector, the more strict one would want to be with entry valuations. The entire pack is trading at cyclical lows, and has already felt pain for an entire year.

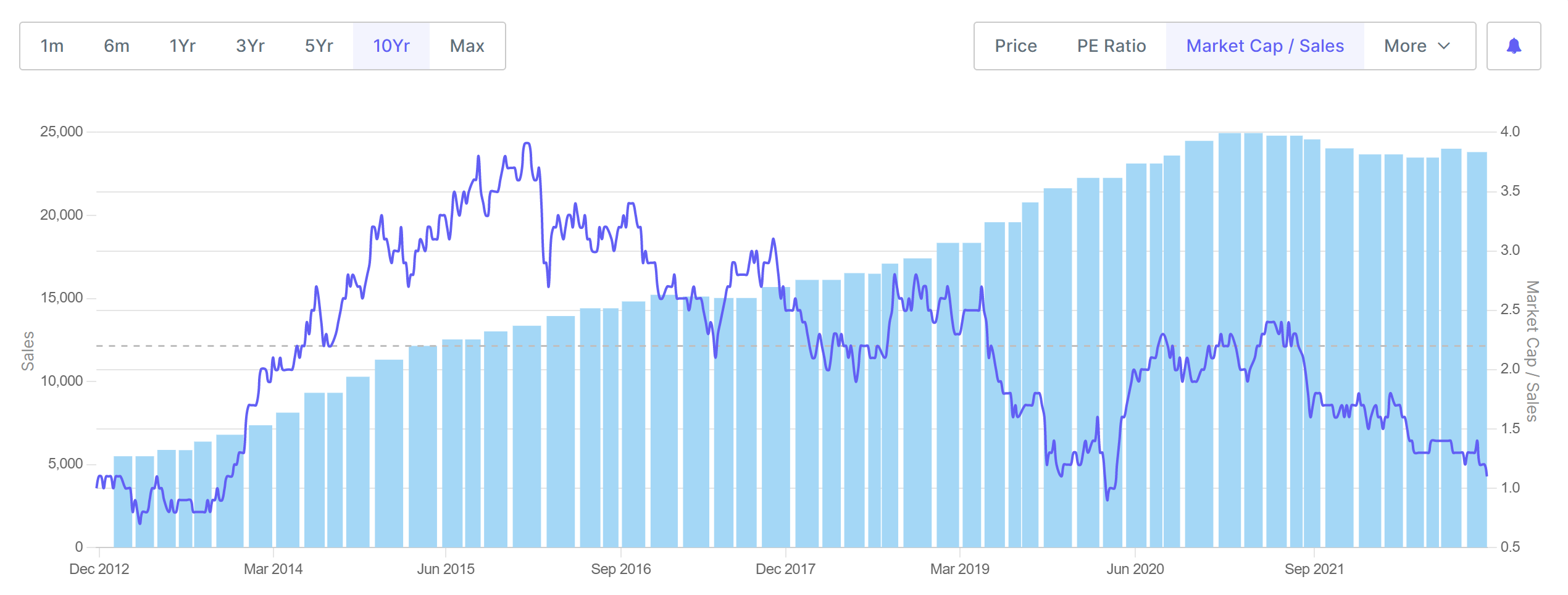

Aurobindo:

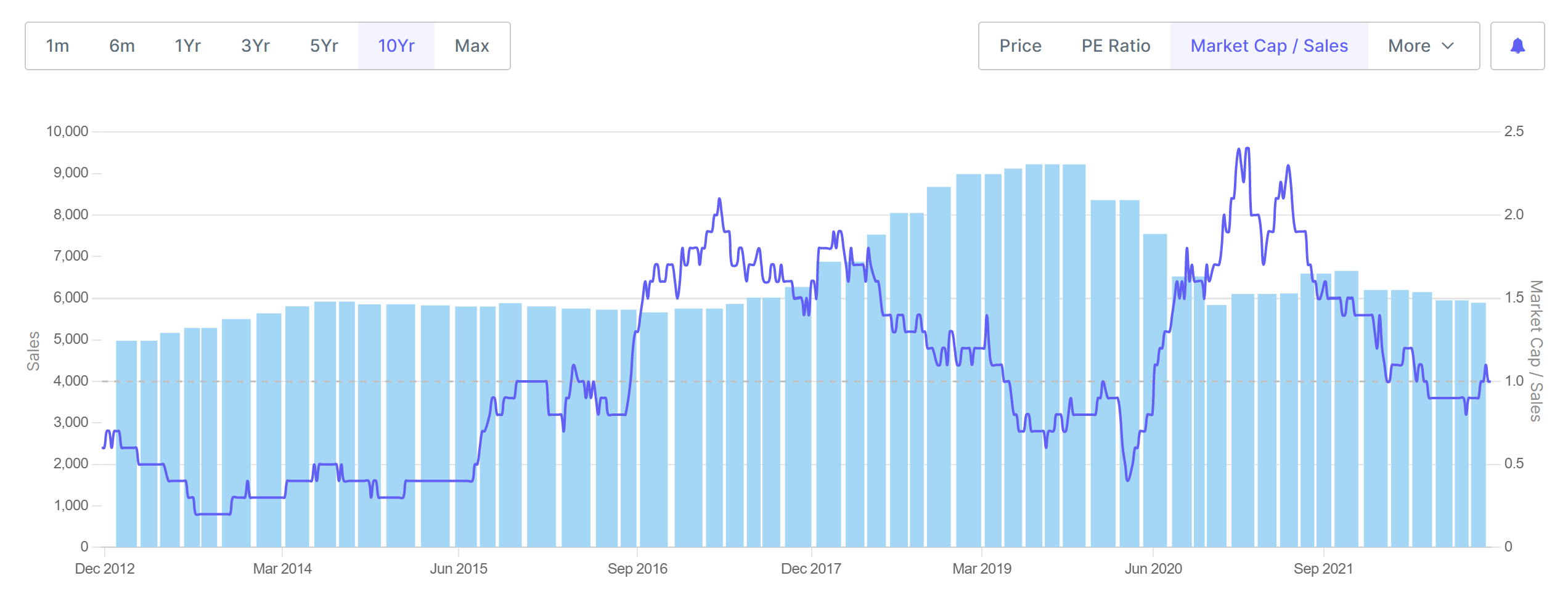

Strides:

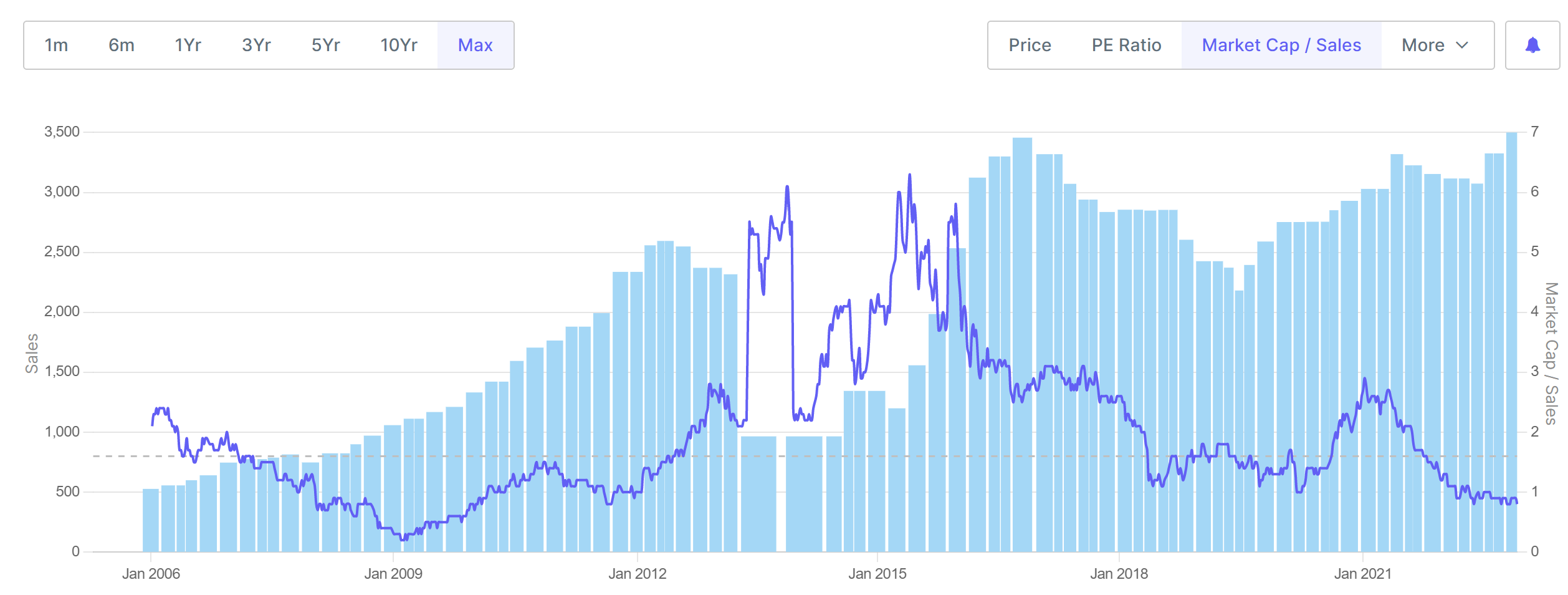

Pharmova still has some way to go:

I’d like to get Strides below 280, Aurobindo below 400, and Pharmova below 300. On the exit side, I don’t think they’ll ever see valuations seen in 2016, but the strategy would never be to hold these for long term, rather churn out as soon as I get a decent exit.

Maybe my earlier answer was too quick. I’m interested in the following sectors due to valuations, and would like to narrow down investment ideas either on quality GARP ideas, or on prices/value.

- Textiles

- China and other emerging markets

- Nasdaq / tech ETFs

- Pipe companies

- US generics

- Dyes/Pigments

- Export facing API companies

PS: this doesn’t take away from wanting to study quality companies and great business models (I’m happy with what I own), rather have a portion of the portfolio allocated to higher churn plays that one can enter and exit without any noise.

| Subscribe To Our Free Newsletter |