Accordingly to me, ROCE is a useless matrix for banks. Inherently, banks are highly geared. If their RoA is better than cost of fund, after adjusting for statutory reserves, it is value accretive for shareholders. So, a better matrix to look for is RoE.

If their lending is secured / to high rated clients, there will be lower credit cost (lower provision / write off) which will help in improving PAT and thus RoE. However, this comes at cost of RoA (higher rated customers will give lower RoA).

Consequently, if banks want to earn more RoA (leading to higher NIM), they will have to tap risky customers, increasing there credit cost. In good times, such credit cost (if properly secured against assets), can help improving RoE. But in bad times, it can even lead to bankruptcy.

If their cost of borrowing is lower (e.g. CASA), they can lend at competitive rates to high rated clients and earn better NIM which will improve PAT and RoE.

If lending is spread across multiple borrowers (lower ticket size), there is less risk of asset going bad, thus lower credit cost (lower NPAs). Which is why retail lending is considered safer, compared to wholesale lending.

If lending is secured (with backing of assets), there will be lower losses in case loan goes bad. Thus supporting profitability and RoE. This is why a vehicle financing is more safer than credit card (100% unsecured).

Cost-to-income ratio also play important role, specially for growing bank / NBFC as initial set up cost (incl. fixed cost) is higher, which will generate steady income only in future.

As Warren Buffett says ” Banking is good business, unless you do dumb things”.

Banking is very simple (and boring). you borrowing at lower cost and lend at higher rate, thereby earning the spread (NIM in industry parlance). But greed (of banking employees) make them do dumb things (like risky lending), which back fires and hurt badly.

@meekinvestor With all due respect, I would suggest please enroll for some banking course to understand the basics. You can learn from various threads here. You can also explore Youtube.

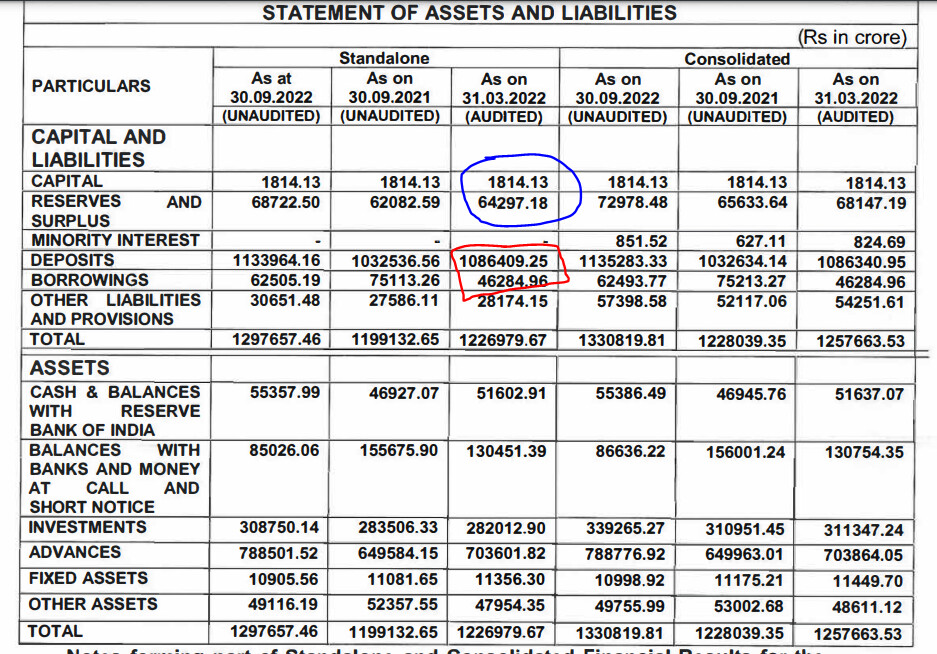

To answer your question, leverage is found on the balance. Below is the latest BS of Canara Bank. On an equity base of Rs. 66111 cr, they have borrowing of Rs. 11,32,694 cr. i.e. leverage of 17x. Part of this borrowing is CASA which is the best form of borrowing for banks.

NPA (Non Performance Assets) are the loan given out to customer but now highly unlikely to be collected. So, as per RBI guidelines, such loans are classified as NPAs. GNPA is gross amount which is unlikely to be collected. NNPA is the net amount after adjusting for provision. A higher provision means lower net NPA (which is good), but lower profitability to show (which is bad). So, NPA pertains to asset side of BS (Asset going bad). leverage pertains to liability side.

| Subscribe To Our Free Newsletter |