Vishay stock price is near 52 wk high – contrast to US markets – this is in line with their performance delivered+ visibility, highest revenue and margin expansion in Q3(CY) 22 numbers. Stock price reflects market optimism in Vishay future prospects – thus visibility for a sizable demand part for Shivalik.

Q3(CY) nos and commentary – note Shivalik shunts are part of resistor family – Higher book to biil ratio and thus backlog continues

-

End segment demand and inventory – shivalik related segments (energy infra, auto- EV etc) demand stays strong – note the tone of EV and charging infra being a future growth driver (shunt application areas)

-

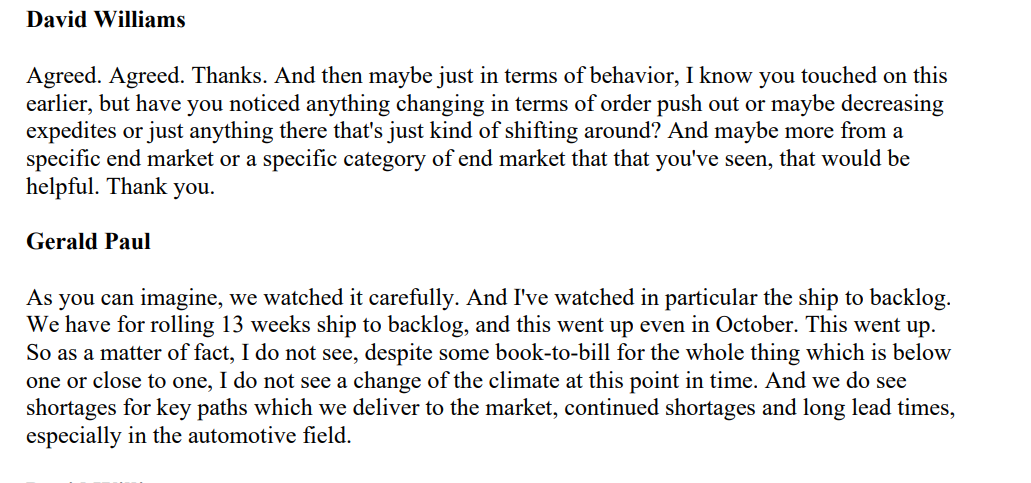

Is demand slowing down for Vishay end customers/order deferment ? doesn’t seem to be the case.

- Additional infrences – growth has healthy contribution of volume + realization. Vishay seem to be emphasizing growth by volumes, thus sustainability.

good read in current mkt context

| Subscribe To Our Free Newsletter |