My Conclusion:

Over the last 12+ years, PPL has built a niche business using acquisitions as the primary tool to fill capability gaps across the drug lifecycle.

- Being vertically integrated and know-how oriented, CHG vertical will continue to gain market share while maintaining the best margins among all the 3 verticals. The established worldwide supply chain will be leveraged to attain higher growth rates by introducing new products.

- Customer centricity (on-Patent drug support at the region of choice), and Capex (constant regulatory upkeep) or Opex (manufacturing presence in the western region) intensity in the CDMO vertical may not allow margins to be as high as that of the CHG vertical. However, relationships (with innovator companies) from this vertical act as a perennial source to find lucrative acquisition targets and to stay well-informed about the latest trends in the pharma industry. Due to its manufacturing presence in both east and west regions aids, PPL is positioned for early-stage client wins and to develop strong processes, which shall mitigate the omnipresent FDA Inspection related risk.

- OTC vertical is almost at a scale where it will start contributing to the operating margins. Ongoing branding by associating the brands with Bollywood actors places OTC products in the FMCG category. With improving awareness among the masses about basic medications, brands from this vertical will build durable customer pull. The last mile pharmacy outlet will be encouraged to keep these products in their stock. Considering India’s demographics, this vertical will have long-lived healthy growth rates.

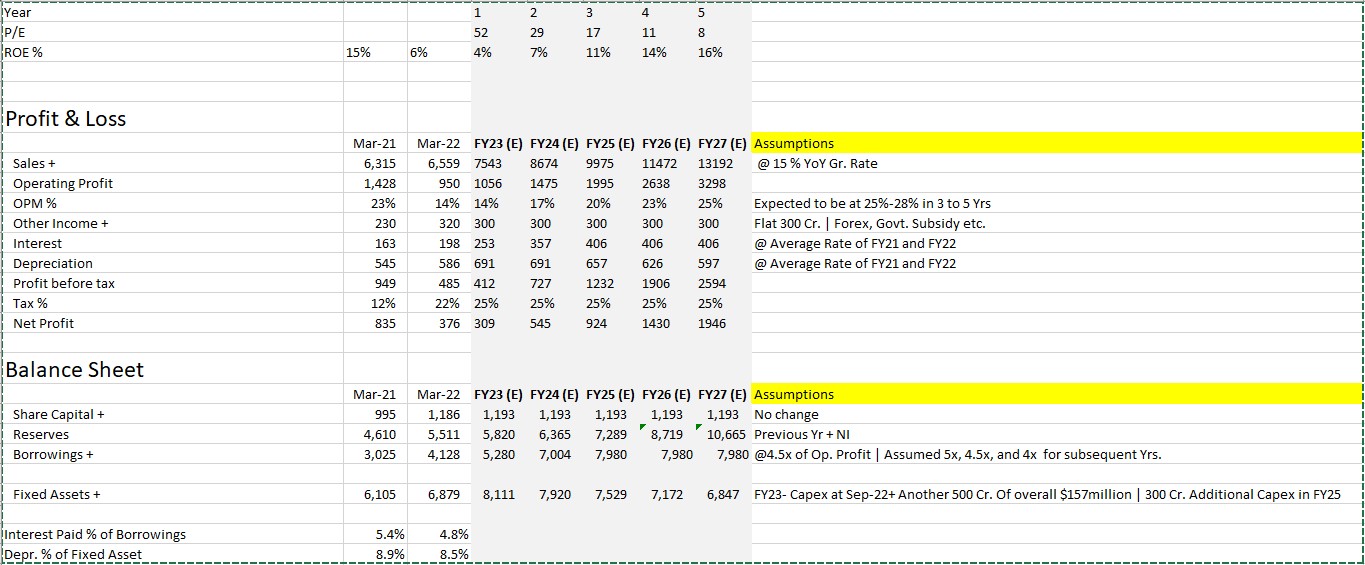

Considering the management’s commentary on the expected revenue growth rate and target operating margins, the stock could be a decent bet for anyone with a horizon of 3~5 years as the ROE would be in the mid-teens compared to below 5% in recent times and PE would be in single digit. The outcome might surprise on the upside in case the revenue growth rate exceeds 15% or targeted margins are achieved at a faster pace. I expect that dividends will also be initiated in the above horizon, considering the promoter’s track record in PEL and the steady nature of the pharma business.

Projections from FY23 till FY27:

Disc: Not Invested. Not a recommendation to buy/Sell. Sharing for collaborative learning and my reference in the future.

| Subscribe To Our Free Newsletter |