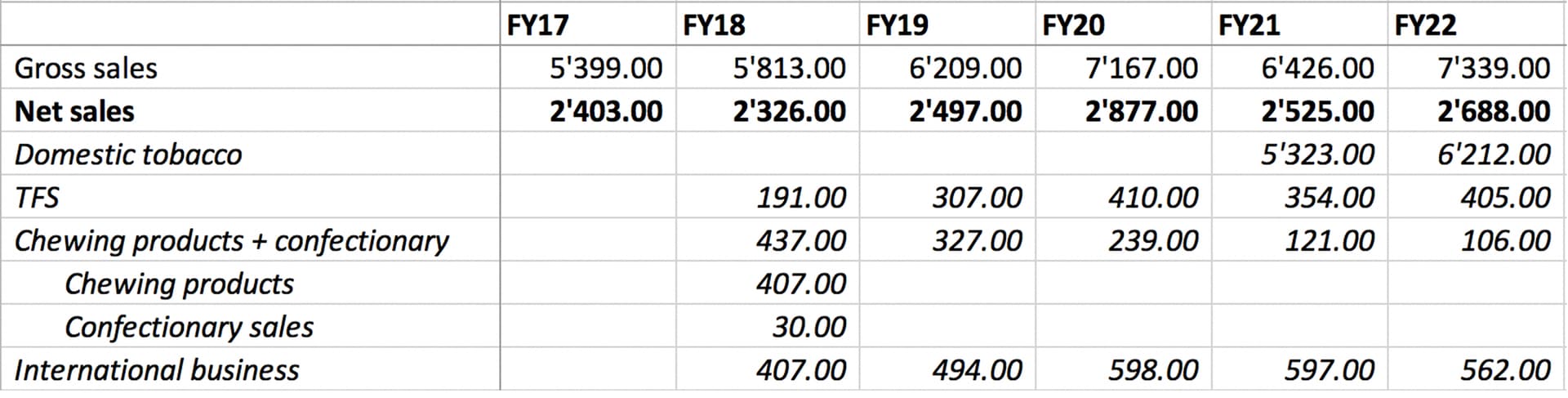

There are three main earnings drivers for Godfrey Phillips:

-

Growth in exports of unprocessed tobacco to Europe due to Ukraine Russia war. Ukraine used to have around 8-9% of global market share in tobacco which has recently gone down. Indian exports have benefitted from this temporary shortage, and is also reflected in Godfrey’s export nos.

-

Revival of domestic business: In domestic markets, growth was coming from TFS (pre-covid). Chewing products business ws struggling and has been recently divested

Now, normal cigaratte volumes have also revived.

So, there is a clear mean reversion in domestic business.

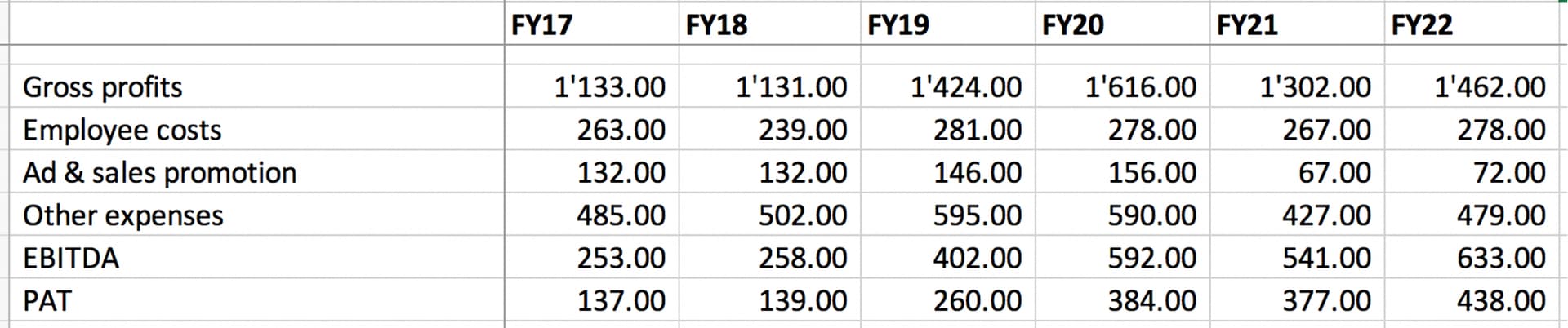

- Reduction in legal and ad expenses resulting in higher margins.

Their annual legal expenses used to be very high at 80-100 cr. which has recently gone down to 30 cr. I dont know why.

Ad expenses for Godfrey used to be very high vs peers (ITC, VST). This has recently been reduced to the industry levels.

I think both these margin benefits are sustainable as they have continued in last 2 quarters as well.

As a result, despite similar gross profits, their EBITDA and PAT has gone up significantly. When gross margins revive, I imagine another jump in profitability.

Summary: Ad & promotions along with legal & professional expenses are now in-line with peers, if this trend carries on then EBITDA margins should expand to 25% levels and may even go up to VST’s margins of 35% as gross margins are at similar levels. Valuations should also go in-line.

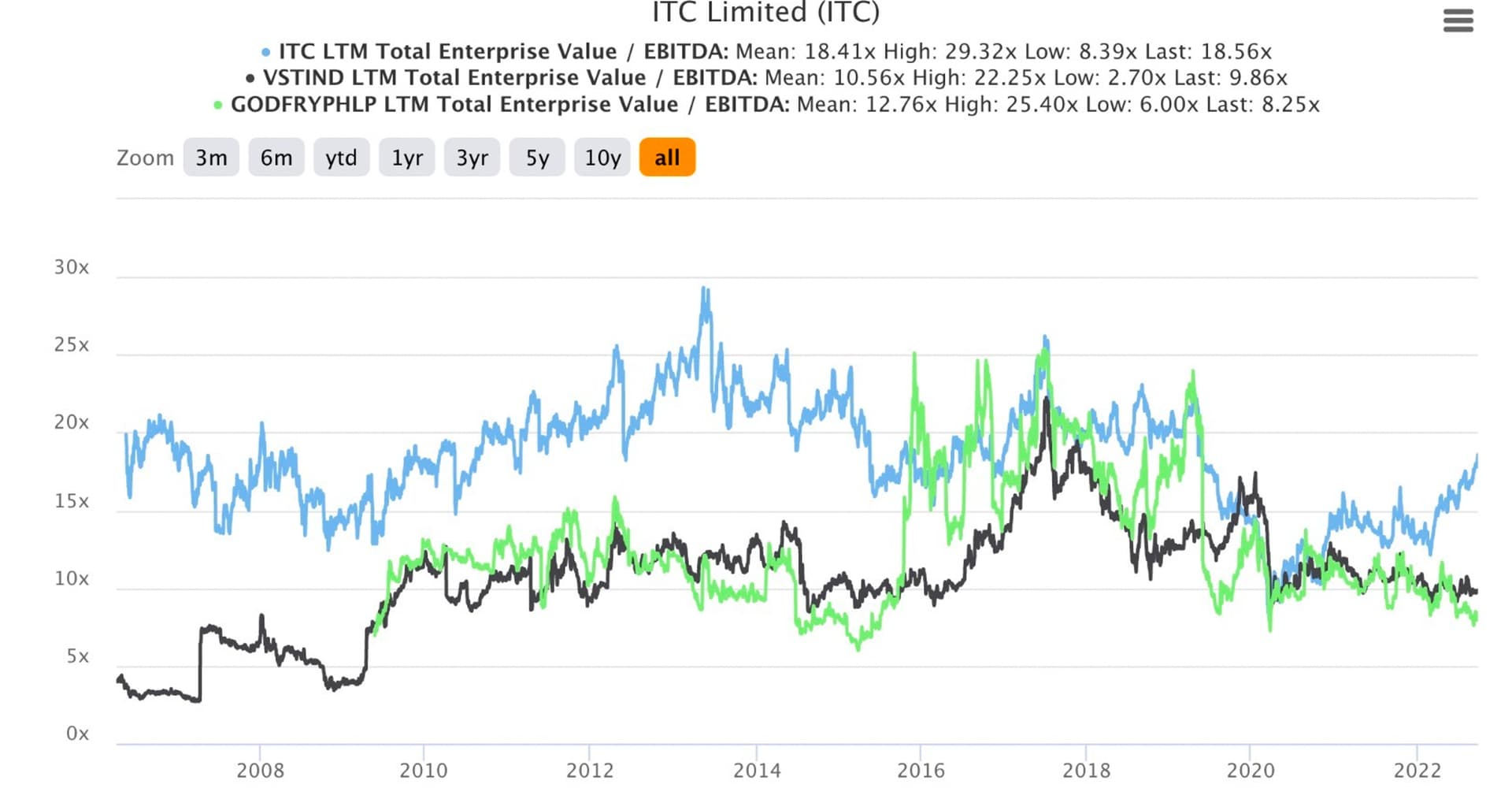

When I started building my position, valuations of Godfrey was the cheapest among peers. With recent move, Godfrey’s valuations have become equal to VST. However, valuations are nowhere close to historical maximum, in the past Godfrey has peaked out at 20x EV/EBITDA. So, Godfrey has now moved from a buy to a hold zone for me.

| Subscribe To Our Free Newsletter |