[/quote]

I think the stock is undervalued by even by the most conservative estimates. I have shared a sum of parts approach to value the different businesses it is in, that you will find below. Key takeaways [Basis Q2 ’23]:

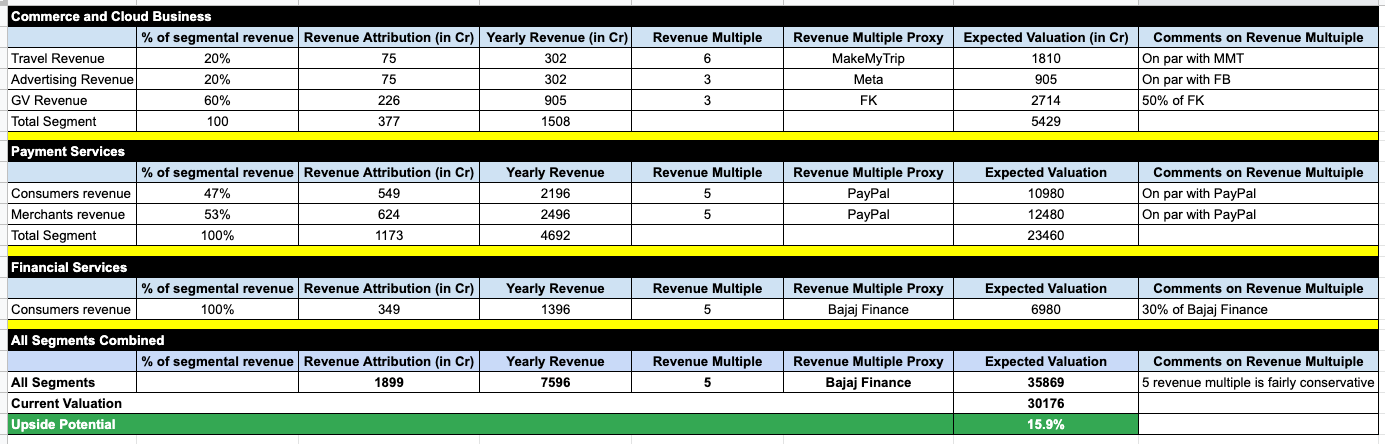

1. Consumer and Cloud Business

a) INR 377 Cr revenue across ticketing, gift vouchers, and advertising.

b) Revenue multiple between 3 and 6 indicated valuation of INR 5400 Cr for this segment [EMT is at 11000 Cr :), and my guess is there business in just ‘ticketing’ is similar to Paytm]

c) The revenue mix will have limited impact (max 20%) on segment valuation, because the highest multiple,6, has been pegged at 20% of this segment

2. Payment Services

a) Despite the much faster growth, revenue multiple of 5, which is on par with PayPal

3. Lending business, without risk (barring Postpaid)!

a) Bajaj Finance is at a revenue multiple of 12.

b) Even at a multiple of 5, it is a screaming buy

Basis this, I intent to start adding positions in Paytm. Even by the most conservative estimate, I think they are undervalued by 15%.

What am I missing?

Disc:

- Ex-Paytm, quit in 2019 (after 3.5 years).

- Looking to invest aggressively below 500 levels

| Subscribe To Our Free Newsletter |