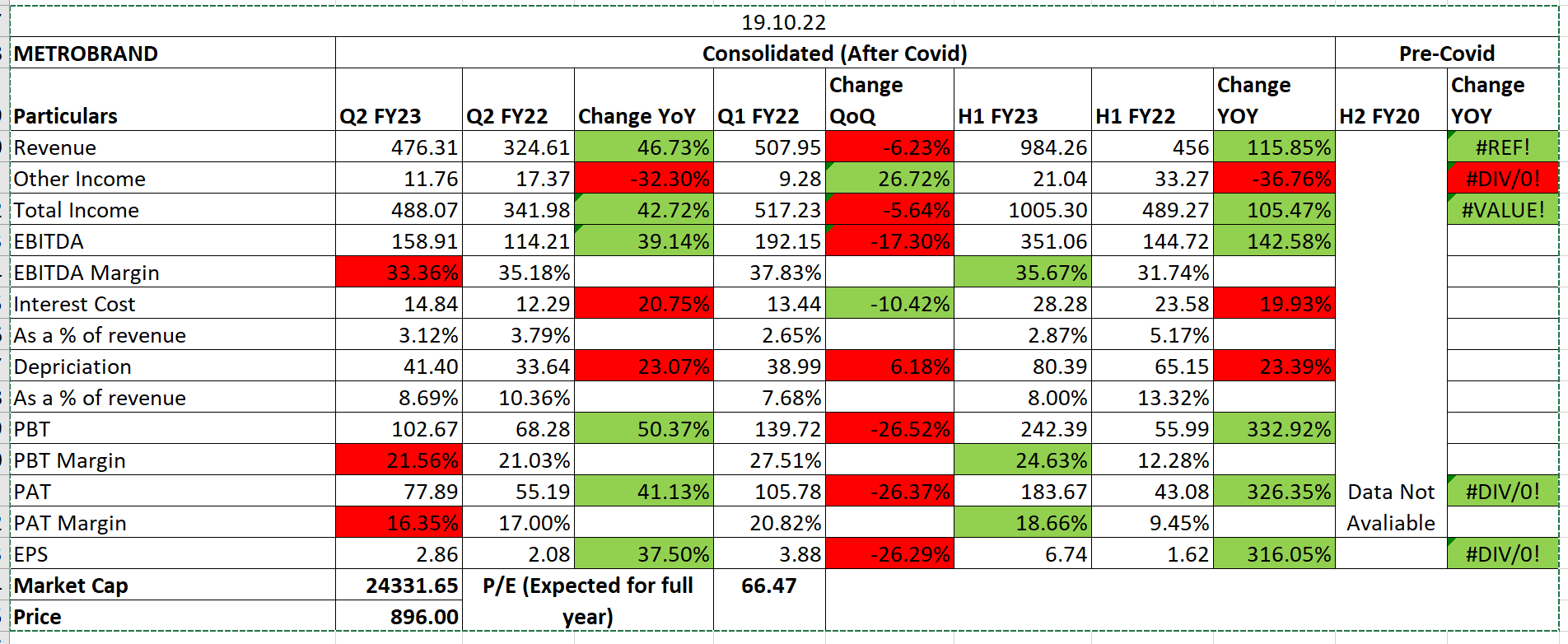

Metro Brands Q2 FY23 Result Update:

- Opened 46 new stores in H1 FY23. Should go up to 80-100 for the full year.

- Q3 demand is meeting expectations. Little pent up demand of covid is still there but it is quite consistent during the wedding season.

- There is good demand seen for the premium brands which cost more than Rs. 3000. Customers are willing to pay more and it is doing well.

- Fila has been acquired. (Sportswear Brand). Will be planning as per what peers are doing.

- EBITDA margin guidance of 30-31%. PAT would be around 15%. Gross Margins to remain between 55-57%.

- Highest ever Quarterly E-commerce selling. Grew 50% YOY.

- Target of opening total 260 stores until FY25 out of which 48 have been opened in H1 FY23.

- Planning to expand e-commerce business.

- Continuous surge seen in volumes and value across all formats and tiers.

- Q1 is generally 25% of the full year revenue. Q2 is 22-23% of the revenue. Q3 is the biggest quarter which 27-28% of the revenue and Q4 is again 25%.

- Gross margins in Q2 & Q4 get affected due to end of season sales.

- Stores for crocs are usually opened before monsoon season as that is biggest for Crocs.

- Costs are a little high this quarter due to salary costs of new stores which will start showing full revenue from Q3 onwards so the salary costs would be absorbed by the revenue. Costs have also increased due to acquisition.

- Price increases are of about 5-7% every year to cover inflation costs and the basket of goods that you’re selling.

| Subscribe To Our Free Newsletter |