Hi guys,

I would like to discuss all the problems faced by RE(wind) and the new policy by GOI to tackle them.

Firstly I would like to discuss what all problems between 2017 – 2021 lead to a decline in this industry.

- Shifting for FIT(free in traffic) to e reverse bidding.

- DICOM not fulfilling their signed PPA

- Wind turbine manufacturing company loosing their PGB(performance bank guarantee) because of not meeting their project requirement on time.

- Poor GRID infrastructure discouraging OEM to participate in tenders.

- Poor land policies which became a huge barrier.

- Increasing GST form 5% to 12% which increased the LCOE (levelized cost of energy)

- DISCOM not doing payment on time because of their poor financial health.

- Increase in price of commodity ( steel a major component, nickel) and logistic cost during covid further added salt to the wound.

After 2020 the cost of conventional source of energy increased and government realized the need for RE energy.

Now I would like to present all government policies introduced to face the above issues.

-

Introduction of RPO (Renewable purchase obligation). The MOP (Ministry of power) has

now introduced RPO for non-solar which was earlier for entire RE.

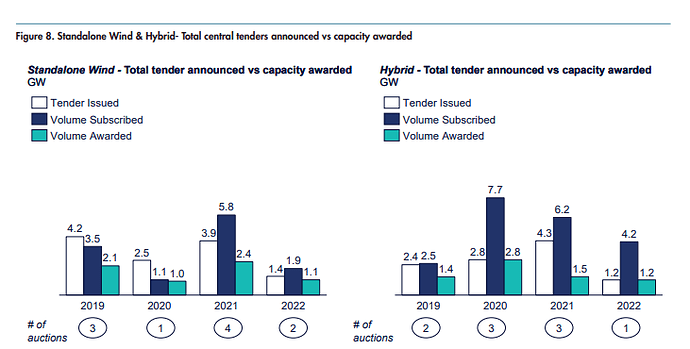

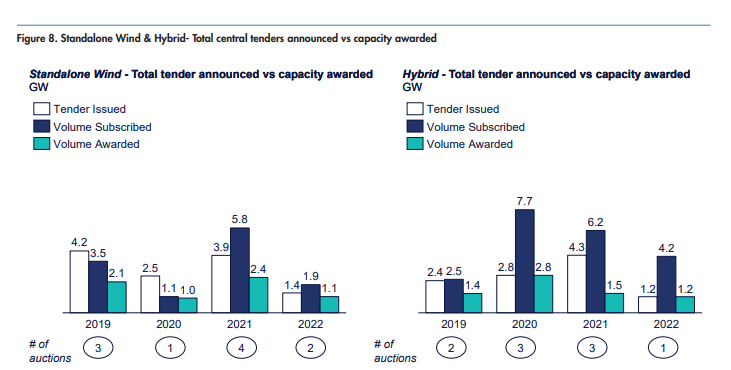

This specifies the power distribution companies to set up minimum capacity over the years.Central tender is expected to have 76% share which is going to decrease the state tender.

This will reduce the problems faced by developers earlier with DISCOM.As per new wind RPO requirement announced by MoP, ~57.5 GW of India’s power demand will be supplied through new wind projects from FY 2023 to FY 2030.This will lead to cumulative wind project installations of ~ 97.5 GW till FY 2030 against a target of ~140 GW set by government. Hybrid and Hybrid+ storage are expected to take this to 140GW target set by GOI.

-

Earlier the PBG were in the range of 8% to 12% which has been reduced to 3% in 2021 which will help in improving the liquidity of the company.

-

Renewed interest in tender auction because of the following evolution ’

**a)**Increasing the transparency to boost developer confidence

**b)**Specifying land and grid details of the delivery point in the tender document before auctions. Also, the projects are in the states of Madhya Pradesh, Maharashtra, and Karnataka to avoid congestion in Gujarat and Tamil Nadu

**c)**The removal of tariff caps had provided relief to developers as price increase from supply chain should be considered in future.Tender subscription volumes between 2017-2019 were 50%-80%. Between 2020 and 2022 we can see it being oversubscribed

.

-

Waiver of ISTS(inter state transmission system) for PPA signed before 30june 2022 for 25yrs and thereafter increase of 25% per year till 2028. This creates an incentive for power distribution companies and developers to sign PPA before 2025.

Waivers to open access(OA) will incentivize third party to directly purchase form developers instead of dicom. Earlier OA was applicable for direct purchase. -

There has been major devolepement in repowering policies which are as follows

a)Repowering in central wind and hybrid auctions before 2021 was restricted to the allotted capacity. During 2021 capacity restrictions for repowering have been removed.

b) Earlier sale of excess generation on repowering of a plant could only be sold to SECI(solar Energy Corporation of India)at 75% of the rate prescribed in the PPA. Now it is allowes to sell to third party as well.

6.To develop an intrastate network**(GRID)**, the central government has announced two phases of Green Energy Corridors(GEC).The first phase is expected to be completed by 2022.It is estimated that ~44 GW of new RE power generation evacuation will be possible through GEC.

24GW from first phase which is due to be completed in 2022 and 20GW from second phase which is yet to be approved.

7.Land policies have been revised and the process is being streamlined in key windy states.Gujarat, Maharashtra, Rajasthan, and Madhya Pradesh have a dedicated land allocation policy for RE.

Karnataka has released a new RE LP in 2022.No land policy update is observed in Tamil Nadu region.

It takes 6-9 months for land allocation process in states where the process is stremlined and 18-24 where process is not streamlined.

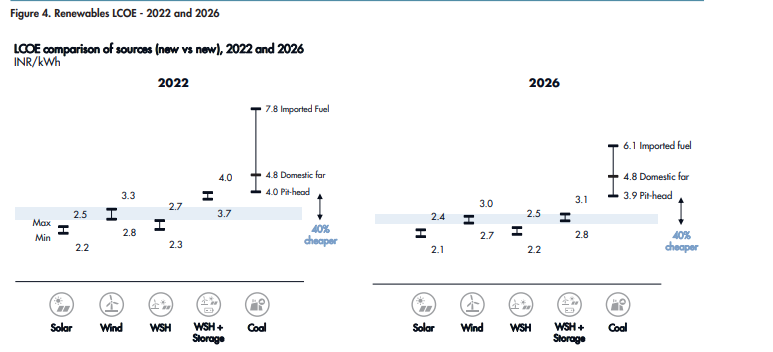

8.Government is aggressively promoting WSH (hybrid) and WSH +storage( round the clock).

DISCOM need 24/7 power supply due to variability in RE they re dependent on conventional source. The cost of storage/battery is expected to fall and increase the demand of WSH+ storage which solves the problem of DISCOM.

WSH increases the efficiency and reduces the cost of power. The HYBRID category is also expected to drive the demand in future.

All the above information has been taken for a detailed industry report below(58pages). I would recommend everybody to go thought as it explains much more than what I have done above.

The report is free and not purchased by me

Click on download report and enter your name, email ,phone no and download

Please read this report if interested in this sector. It is information overload free of cost.

In my next post I would love to present my view on Suzlon and how I feel it has a good opportunity in future.

Government has realized the need of RE between 2020 and 2022 and is aggressively trying to revive this industary from its policies.

Suzlon is a call option on government policy and this industry which I will sell once I see government not showing further interest in it( at least till 2030 I don’t see this happening unless central government changes, their intent is very strong and the future of this industry looks bright.

It is 4% of my portfolio with average price of 8.25.

| Subscribe To Our Free Newsletter |