Minor updates for disclosures.

- Punjab Chemicals

- After doing some channel checks about the current situation in the UK where Punjab gets a significant portion of its revenue, I have decided to scale down my position to <1%. I have a feeling this quarter may be a difficult one, and would prefer to buy after results.

- PDS Limited

-

For similar reasons, I have scaled down my position in PDS Ltd. to around 1% of my portfolio. They have around 80% of their revenue coming from the UK/EU, and channel checks from friends in the industry suggest a tough time ahead, with retailers having high inventory.

-

PDS is the company I spent almost a year on, so selling was a difficult decision. I would like to re-enter as soon as possible.

- Equitas Small Finance Bank

Having bought at around 43-44 per share, I have sold a majority of my holding at 59-60 per share. It has generated 30% returns for me since, and I think risk reward from here is unfavourable as a trade. (This has absolutely no bearing to anyone who holds Equitas as a core investment.)

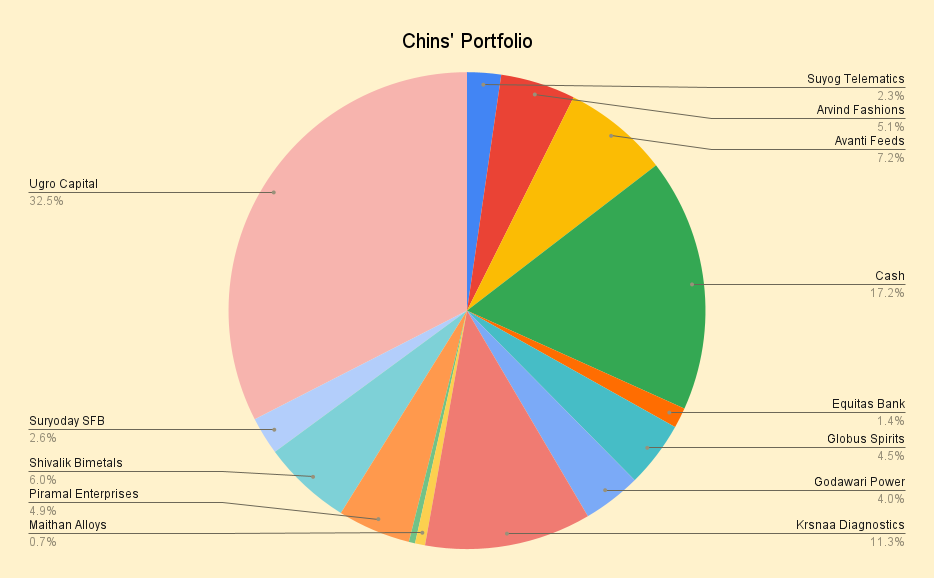

Consequently, I’m now in around 17% cash, and my portfolio looks like this:

Some thoughts on buying headwinds:

- I have tried to identify triggers for the companies I’ve bought going through headwinds. For example on Godawari Power:

-

I got extremely lucky, with the export duty being revoked a couple of days after buying. It has given me 20% returns since. I will exit at around 1.5x book, at around 360-370 per share.

-

On others, if I’m extremely early on buying, the stock can languish for a long time (eating into CAGR) until headwinds recede. I made this mistake with Sandhar last year, and possibly right now with Avanti Feeds. It looks like pain will continue until April 2023, or atleast until there’s good news. There’s a lot plaguing the Indian shrimp industry at present.

-

To avoid this mistake, I was looking to buy Alembic Pharma, but I think the best time would be in a few months, after the plant has received its approval, but once depreciation starts to hit during ramp up. I could be completely wrong, as the valuations are very reasonable.

A few other companies I’m looking at right now include Maithan Alloys, and Caplin Point. I’ve owned the latter in the past, but I’m looking at it through a new lens, after a year of becoming a better investor.

I feel no hurry in deploying cash. Happy with how my portfolio is currently positioned.

| Subscribe To Our Free Newsletter |