Hi Sodhi,

Thanks for sharing this new story. I have been tracking this Company from past one week. Don’t know much about the Company but read its latest annual report.

Some of the important extracts from the Annual Report are the following:

Following are some of the important links:

http://www.skipperlimited.com/pdf/Skipper%20Concall%20Q1’FY%2016.pdf

http://www.careratings.com/upload/CompanyFiles/PR/SKIPPER%20LIMITED-09-02-2015.pdf

The Company has become the manufacturing partner of Sekisui a Japanese Company which is one of the world’s leading manufacturers of CPVC compound, for manufacturing premium quality CPVC pipes.

Secondly the Company has entered into tie up with WAVIN, a Netherland based Company, which is one of the world’s most renowned plumbing technology companies, for launching in India, the most advanced plumbing systems in the world. With these the Company is hopeful of becoming a Pan India brand in the PVC piping space in the near future.

The Annual Report seems to be of Standard Quality and carries the following vision statement:

“To be a billion dollar company by 2020 that is focused on producing industrialised, market oriented and finished products and services, with an increasing affinity to customer-centricity.”

Important Points Noticed:

1) 1600+ Employees as on date and growing;

2) Largest player in eastern India with unrivalled leadership for all T&D projects announced by the Government of India for east and northeast India.

3) 30 years+ Domain knowledge across towers and pipes industry.

4) OUR MANUFACTURING FACILITIES We have three state-of-the-art manufacturing facilities – two at NH-6, Jalan Complex, Jangalpur, Howrah and a major one at NH-6, Uluberia, Howrah.

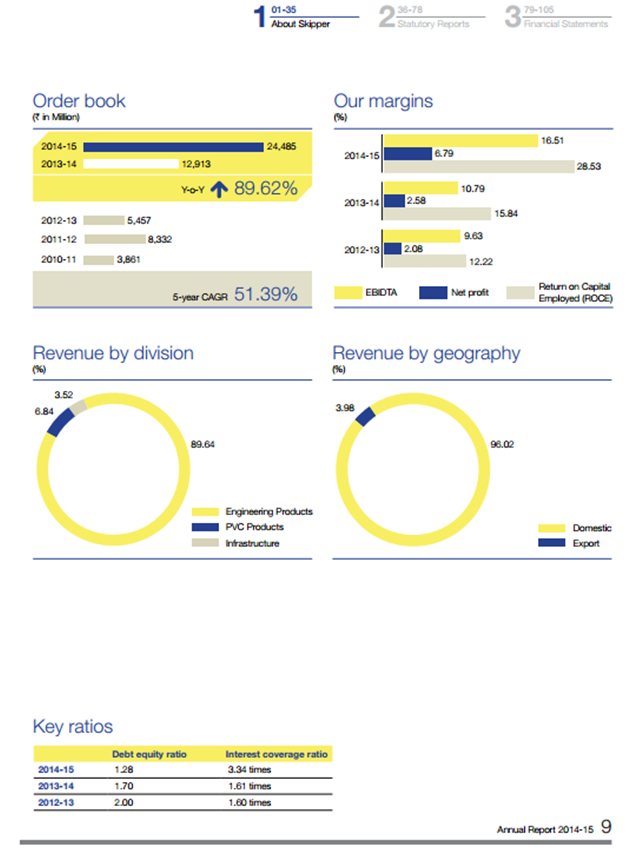

5) 51.39% 5-year CAGR

6) Trading and Deliverable Data indicates that day in and day out the deliverable of total shares are > 75% coupled with rise of share price is really noticeable for such small cap Company (Please verify with the link and search- http://www.bseindia.com/markets/equity/EQReports/StockPrcHistori.aspx?flag=0&expandable=7)

Positives (Views)

1) Numbers and Margins are improving year after year;

2) Huge deficit in India for Power and opportunity to tap with New Government (The per capita consumption of power in India is around 90 kVA per person, compared to the global per capita consumption of 313 kVA per person and China’s 447 kVA per person);

Negatives (Views)

1) Power Sector is highly regulated in India and it is not very often that we see multibagger in this sector;

2) High Debt sitting in Balance Sheet.

Questions:

1) In the Annual Report “asset-light approach” is mentioned . Unable to get to know about the dynamics and model.

2) Does anybody have any idea about the promoters? Basically want to know about integrity and shareholder friendliness of the promoters?

Lets discuss this Company in detail, this might be a great story in the making which will truly unfold as time progresses.

Disc: Not invested yet but tempted.

Regards,

Gaurav

| Subscribe To Our Free Newsletter |