Hi- @richdreamz

Musings on Delhivery:

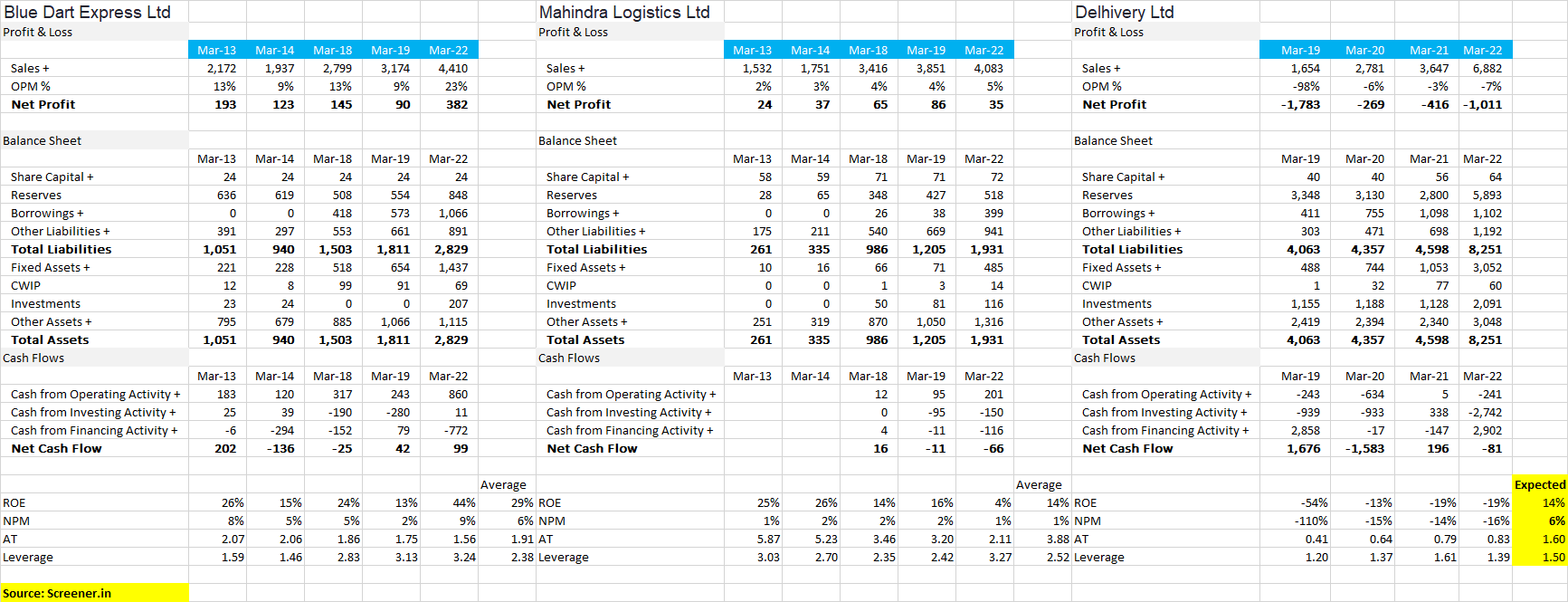

Being a B2B business, the capability to remain the cheapest service provider remains the key sales growth driver after matching speed, accuracy, and real-time tracking. Delhivery’s main and long-standing competitor (Blue Dart) did an average npm of 6% in the last 12 Yrs, details in the below-shown snapshot. I infer that Delhivery will aim to operate below this number due to below reasons:

- Aspiration to grow faster than the Industry/Market leader/GDP. This seems to be the reason why management keeps stating that incremental cost efficiencies will be passed to clients.

- Sales must be doubled for the current size of the balance sheet so that ‘Asset Turns’ double and become closer to the Industry’s average value.

- 60% of revenue comes from the express parcel service that caters to highly cost-sensitive eCom businesses.

With the above context, ROE would be in the mid-teens (assumptions – Yello Colored Data- shown in the below snapshot).

-

Did you come across any reasons that indicate better net margins?

-

What makes Delhivery the cheapest service provider as claimed by management in various calls? Why is the market leader unable to match its cost structure?

-

Acquisitions have been a major source of growth in the last few years. I am skeptical about the health of growth that is based on M&A on a continuous basis. This delays the timeline to achieve bottom-line profitability. What’s your opinion?

note: TAM for Other business lines – Supply Chain Services, Truckload Services, and Cross-Border Services is huge. I anticipate an inorganic route to grow in these service lines as Delhivery is a new/marginal player in all of them.

Request your thoughts. TIA.

| Subscribe To Our Free Newsletter |