Hi Guys,

Today I would like to discuss about the demand side of this industry

Let me start with the board level targets thereafter we will go in detail.

-

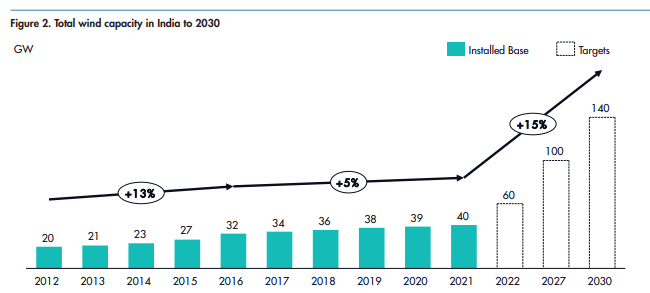

GOI have a target of 140GW of wind capacity by 2030 with 40.4GW of capacity from FY23 beginning.( Please note this 140GW of target includes standalone, hybrid and round the clock wind energy)

-

By 2026 government has a target of 60GW of capacity from a base of 40GW at 2022 January.

-

Our power demand is expected to be at 817GW by 2030 and government has set a target of 50% of this to be catered by renewable energy(all category).

-

With every 7% growth in our GDP our power demand grows at 6%. The co relation between GDP and power demand is high.

-

India has huge potential in wind energy. 127GW in offshore and 695GW in onshore at 120m hub height.

6.Good amount of repowering opportunity especially for suzlon because suzlon was in an expansion phase between 2000 and 2006. Since most of the wind turbine have a life span of 20yrs this creates good amount of repowering opportunity between 2020-2026(Will try to quantify this). Favorable repurchase policy further incentivize developer’s

How realistic are these targets?

Most of the targets revision and policy making was done between 2020-2022 and these two years wind energy has not been able to achieve those targets set by government for the particular year majorly because of covid. So as on today wind energy is lagging against the target set.

These targets being met is completely in the hands of government becasue they are the only customer especially wind (commercial and Industrial share is extremely low). The urgency this government is showing as on date and the policy they are introducing makes me belive that they are achievable. BIASED

One of the big factor for this industry to achieve their targets is BJP coming in to power post 2024.

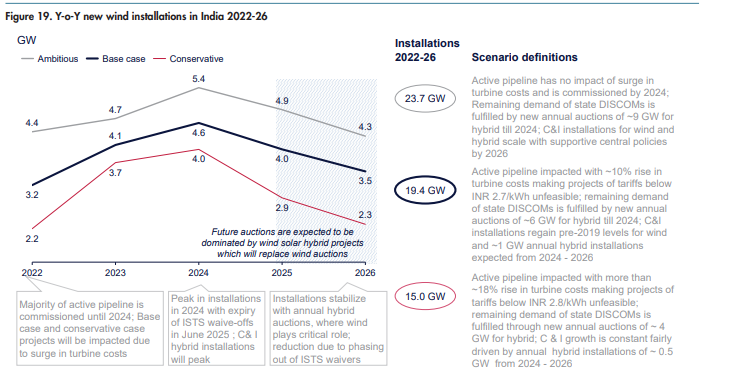

Current pipeline and 2026 target of 60GW(standalone)

This forecast does not include tender from PSU, Round the clock tender and repowering. RTC is expected to dominate post 2025.

Demand has been projected taking 3 scenario because the cost of manufacturing has a big impact on the demand and supply especially wind because the manufactures cannot pass the cost to buyers.(Buyers have bargaining power)

Up to 2026 19.4GW of capacity has to be installed(base case) out of which 14.9GW from central,3.1GW from state and 1.4GW from C&I. (center having 75% share and state having just 16%)

State auction= All previous problems and Central auction= favorable business.

The average power purchasing cost (APPC) across 19 states procuring power from central auctions is reported to be 30-35% higher as compared to standalone wind prices in central auctions. Also, these states have APPC ~50% higher in comparison with hybrid wind projects of central auctions.

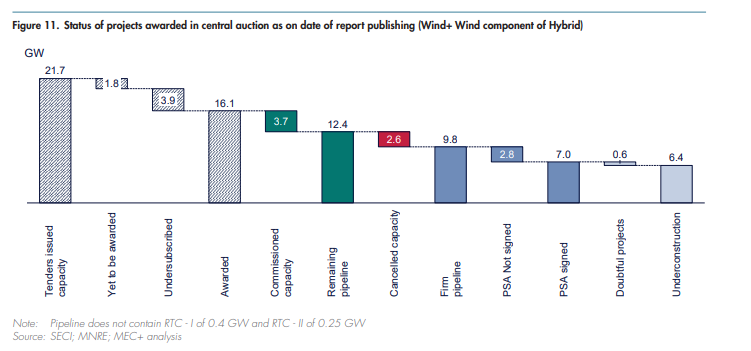

This is one of my favorite charts because this shows how much you start with and what you end with.

1. As of now there is 9.8GW of firm pipeline and further tender of 5.1GW will be issued to meet 14.9GW.(For center)

2. 1.4GW pipeline for state and further tender of 1.7GW will be issued to meet 3.1GW (For state).

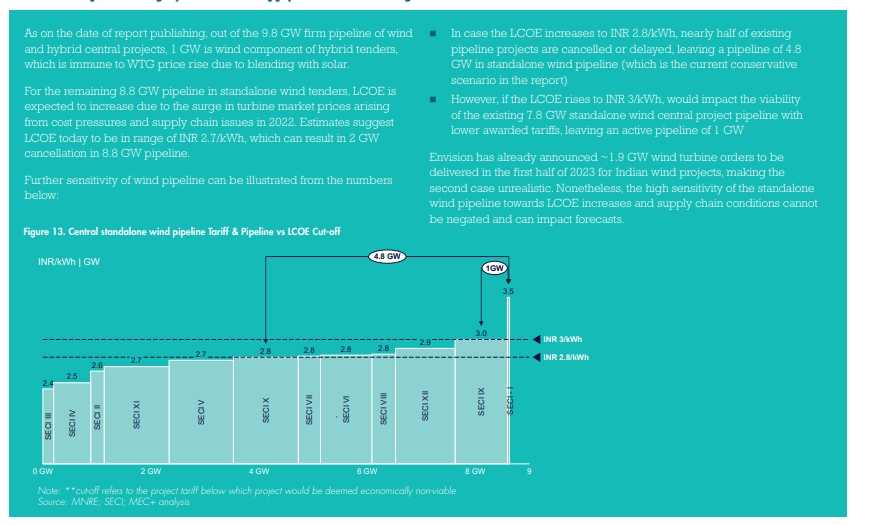

This is the sensitivity analysis for central wind projects.

Future cancelation can be determined form traffic.

With Suzlon having close to 2000cr debt and 500cr of cash and 1GW of order book it looks strong as of now.

Question which I have in my mind for suzloz. Will find asnwer for them.

- What is the brake up of thier oderbook (how much is standlone,hybrid,round the clock).

- Are they just planning to do the wind component of WSH and WSH + storage in future.

- The benefit of debt is completely going to be visible by next quater so how is the company further going to increase efficency.

- What will they do with that cash

- At what quantity fixed cost gets covered and operating leverage kicks in.

The demand and policy looks favourable. I am still understanding suzlon as a company.

In October 2021, Adani Green Energy Ltd. (AGEL) acquired SB Energy India for US$ 3.5 billion to strengthen its position in the renewable energy sector in India.

Suzlon promoter having extremely low stake also open an opportunity for it being acquired in future as the acquisition trend in this industry is extremely strong as of date.

All the numbers and charts have been taken from GWEC(global wind energy council)

report which is free.

thankyou

| Subscribe To Our Free Newsletter |