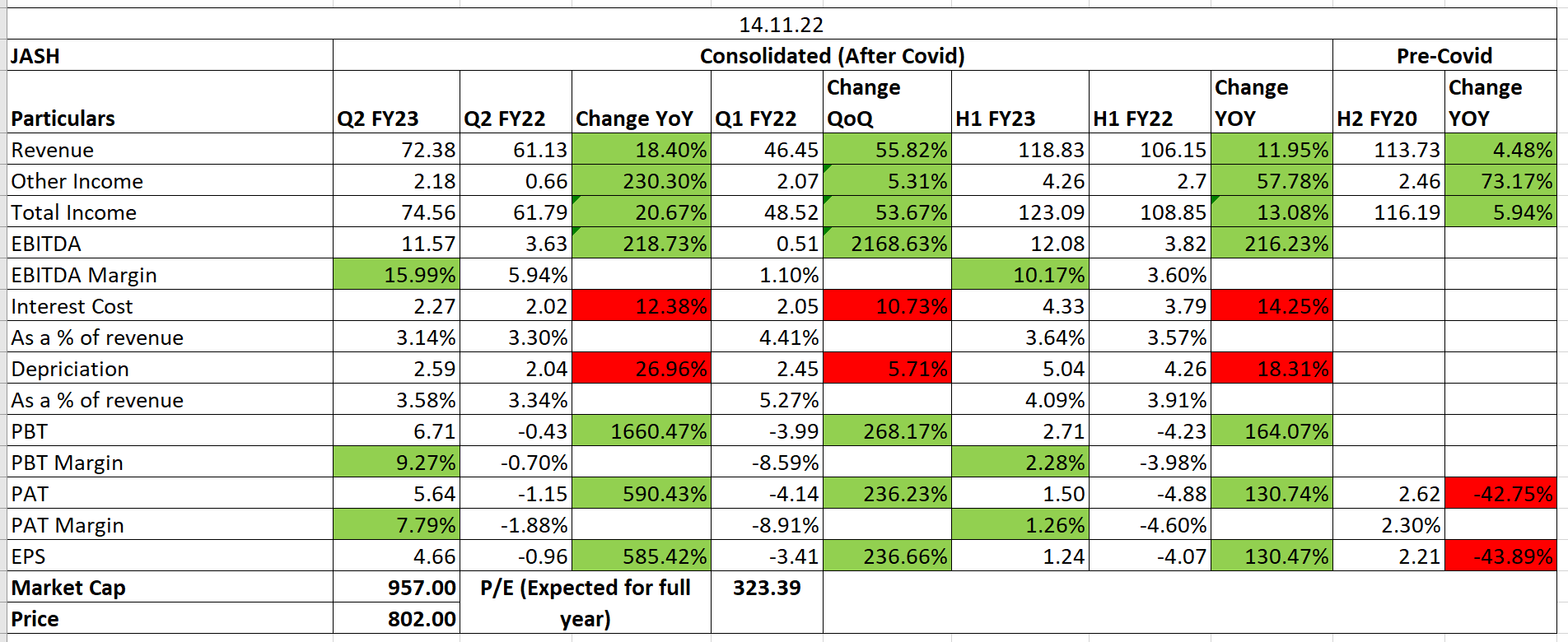

| – | Giving a sales outlook of 430 cr on a consolidated basis for FY22-23. Out of which only 118 cr has been achieved as of H1 FY23. They are very confident in achieving 430 crs of revenue. |

|---|---|

| – | There is growth of 30% in standalone revenue but lower dispatches from subsidiary companies have subdued the 1 st half consolidated results. However looking to the billing already achieved till date we are quite confident of significant jump in Q3 revenue on consolidated basis. |

| – | Improvement in Q2 profitability on standalone basis augers well for annual profitability because in subsequent quarters revenue is expected to grow at a sustained pace. Profitability of subsidiary companies is expected to significantly improve as their Q3 revenue improves. |

| – | Raw material prices are going down which is helping in improving profitability. |

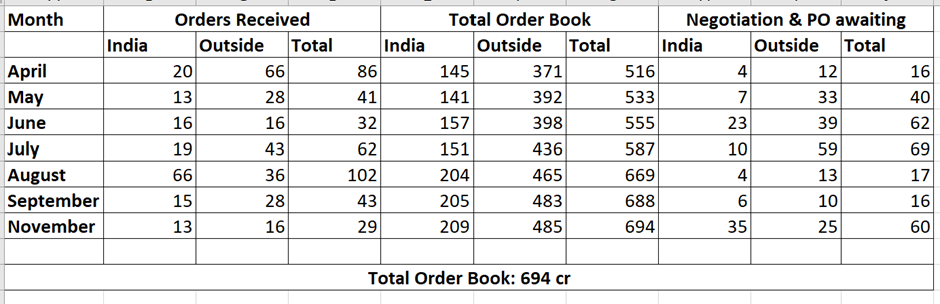

| – | Expecting order booking to get significantly higher in next 4-5 months as lot of contracts are on finalization. |

| – | India & America are the strongest countries for Jash in terms of revenues. |

| – | Margins are likely to be sustainable at current levels if there is no further price rise in raw materials. |

- Order Book is increasing. Negotiation or PO awaited Book is also increasing.

| Subscribe To Our Free Newsletter |