Hi guys,

After discussing all the policies and little bit on demand today I would like to talk on Suzlon and where I see this company in coming years.

Please note that I like to go extremely mathematical and then support those numbers with qualitative aspects.

About Suzlon

- Suzlon is an OEM and they make wind turbine generators. They are the 3rd largest player with 33% market share.

- They have cumulative installed capacity of 19.5GW in 17 countries with almost 14.5GW in Asia.

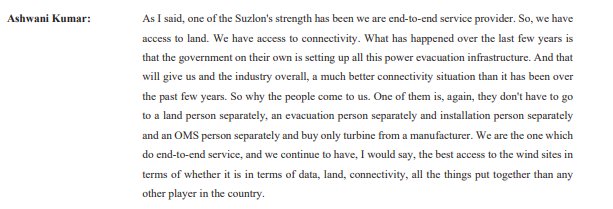

- They are a 25yrs old company and an end to end service provider

What is end to end ?

I think this is one of the major strength of Suzlon

- Last year Suzlon did 807GW of business. Their current year first half is 15% higher than FY22 H1.

- They have a ready capacity, workforce and ability to diliver 3.1GW per year.( this capacity is almost 4 times their FY22 output, this means sales can go 4x without addidional capex)

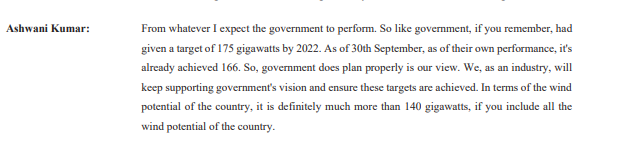

- We have a target of 140GW by 2030 and here is what management has to say on it.

- Suzlon had a debt of 2200cr and there is another 600cr of rights issue due, close to 200cr of cash, 2 assets which is non core to the business which they are planning to sell.

a) 11 acre of land in pune

b) SE Forge 100% subsidary of suzlon

NOTE- (Suzlon has the ability to take their debt level to 1000cr and interest cost to 100cr per year)

Demand analysis.

140GW is a pretty big target and has a lot of time to be achieved. Let us be conservative and try to predict the demand which Suzlon will have.( Please note will take reference from my previous post)

- A total for 8GW of tender will be issued by central and state till 2026. Suzlon can get 2.5GW form this

- As per MNRE there is a repowering need of 25.4GW up to 2030. Suzlon has a possability of 7.5GW from here. Let us take only 2GW up to 2026

- Suzlon as on date has 1GW of order book. Out of this 284MW is from retail/PSU(please see next point)

- PSU and C&I segment is not included in the above prediction where as because of ISTS wavier up 2025 they are aggressively setting up wind farms. 30% of Suzlon current order book is from this segment. This is further going to add to their demand.

As of today we have a 5.5GW of predictable order book this does not include the PSU and C&I which is a big segment.

So for the next 3.5yrs we have 5.5GW of visible demand. Since this is the base case assumption and does not include some big segments I think this is not optimistic at all.

My expectation for Suzlon is 1.5GW of business in FY25 or FY26. This is 85% higher than FY22.

This cost of debt might come to 100cr. I am expecting 1.5 EPS from them(this is extremely conservative because their incremental margin on new sales keeps increasing)

I am expecting 25rs to 30rs by FY25 or FY26.

ADD ON

- They have their AMC business which has been flat form many years because of no new big capacity being set up post 2017.

( If somebody can please quantify this by taking last year AMC revenue divide by their asset under management which is 12GW and multiply this to 5.5GW) - Suzlon is also planning to do AMC business for other turbines which has not been developed by them. This segment has 40% as EBITA margin and is pretty big

Their new prototype is also a big add on which can produce 3.1GW

With favorable policy and huge demand I feel there is a good opportunity for suzlon in the coming years.

I would love to double my qty in this stock below 10rs.

This is 3.5% of portfolio on CMV of my portfolio with 8.25rs as avg price.

| Subscribe To Our Free Newsletter |