Some interesting recent updates:

-

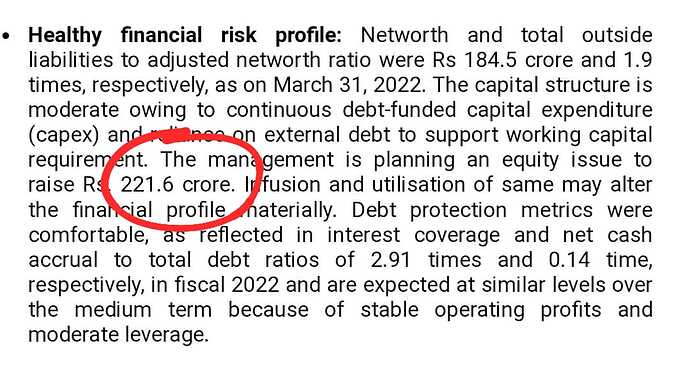

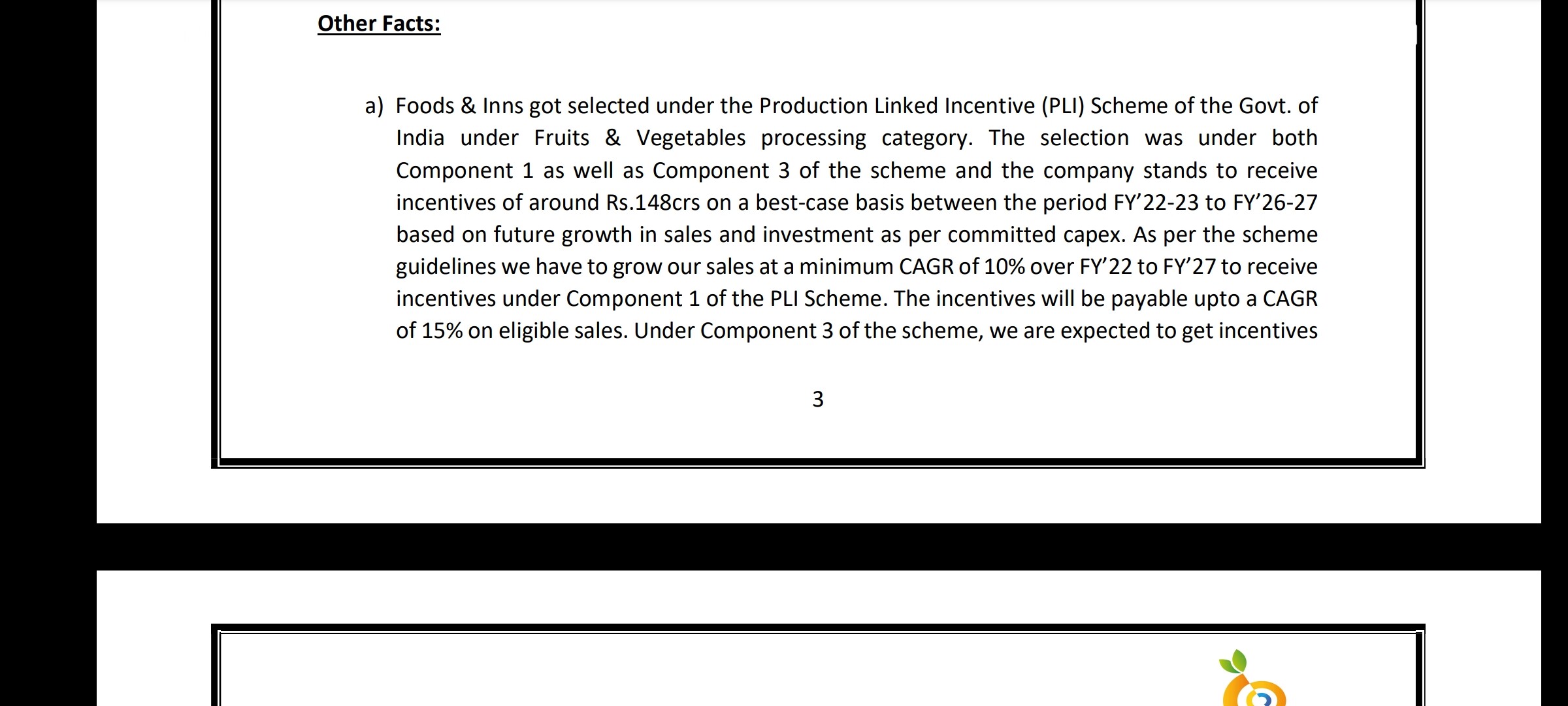

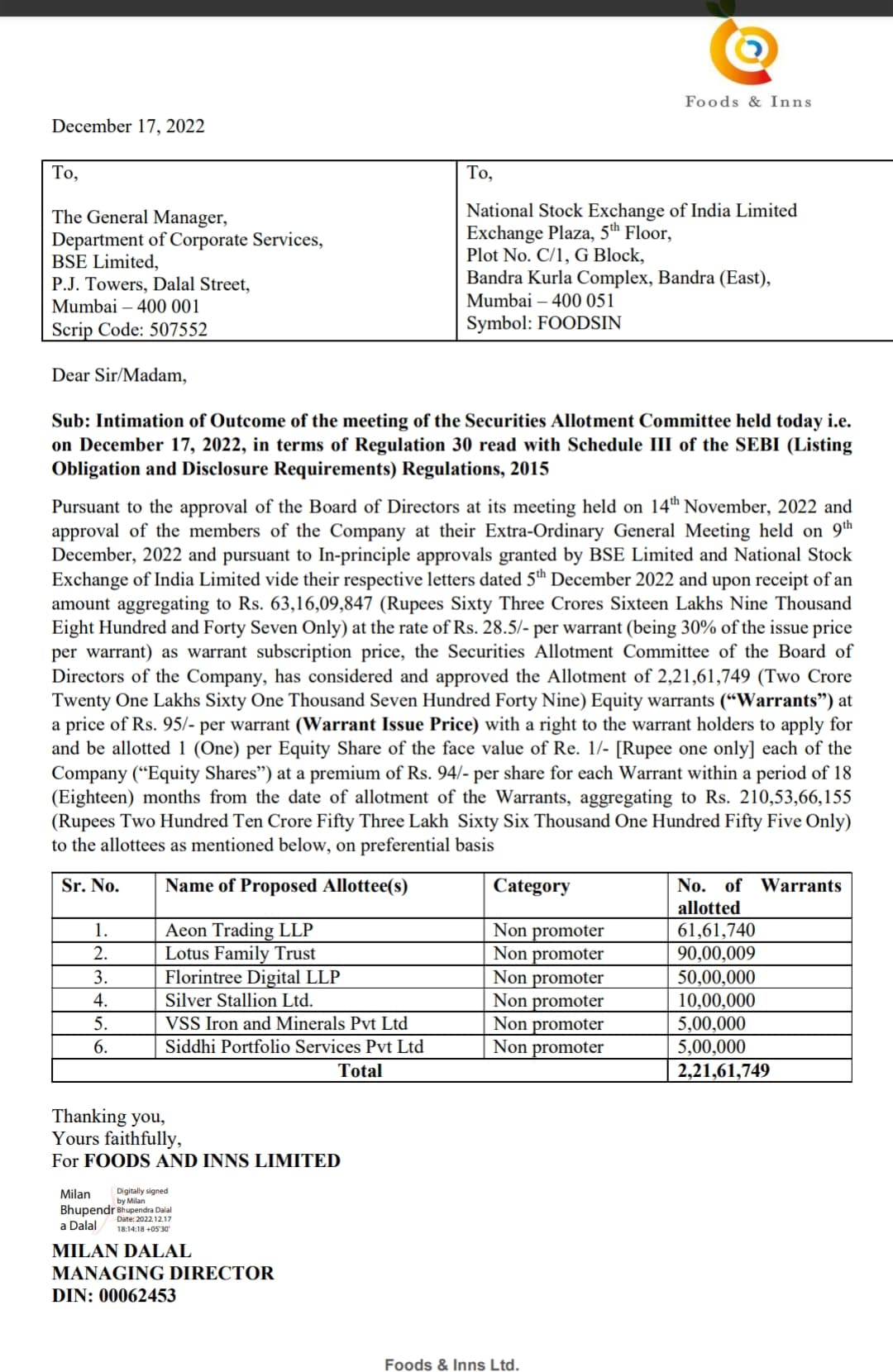

Company is planning to issue warrants and as per their latest credit rating report equity infusion of 221 crore may be infuse in future. EGM has held for the same.

-

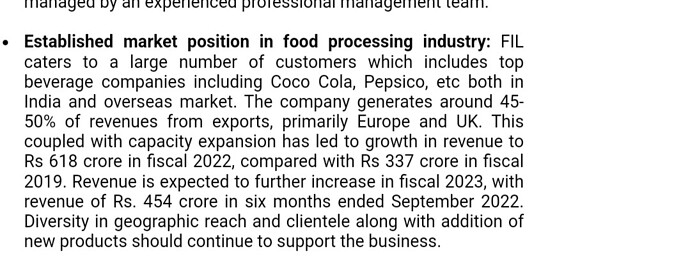

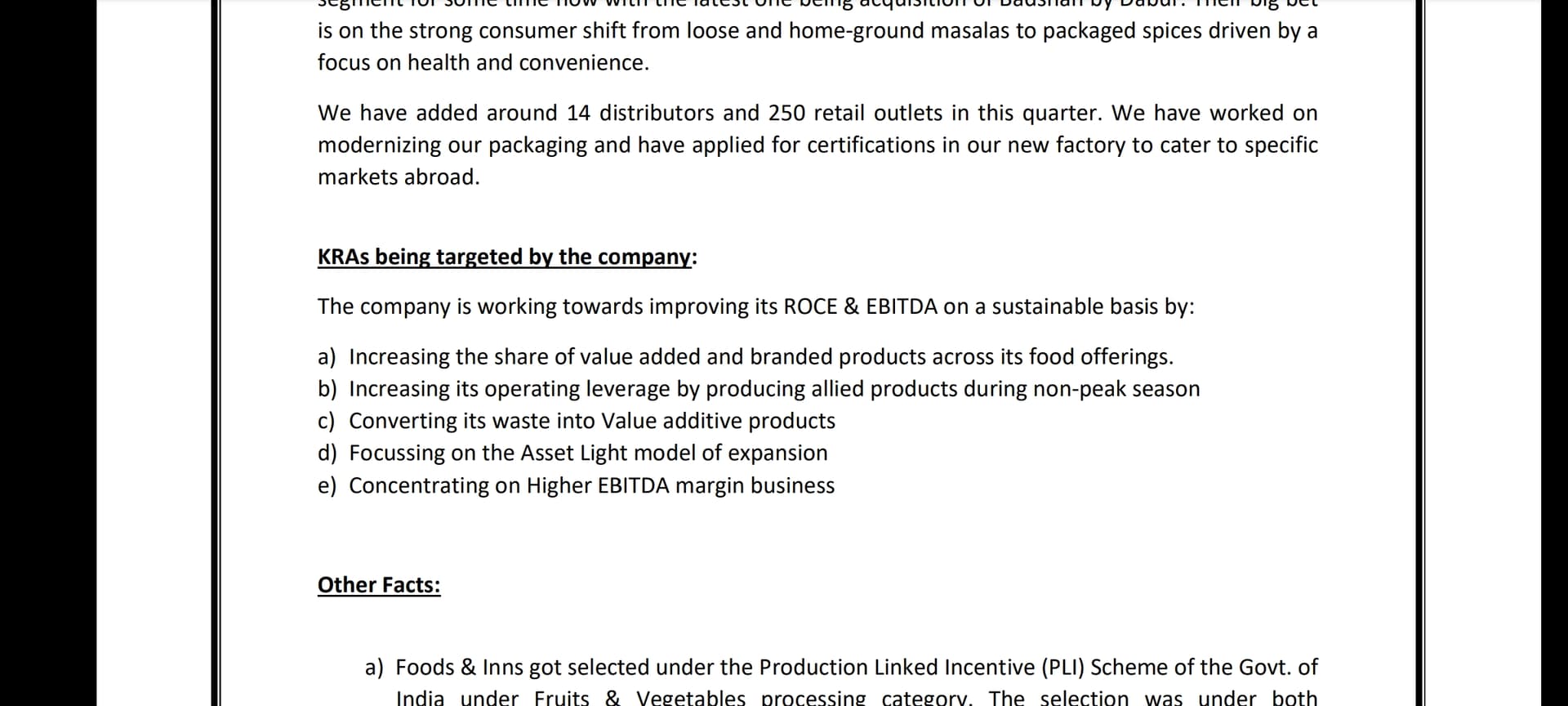

Volume growth is not coming but focusing more on VAP hence margin will shoot up. Perfect proxy to play beverages industry tailwinds, Coco-Cola and Pepsi both are focusing on juice segment to fuel their future growth pulp is main raw material for it and that’s where Food and Inns comes.

-

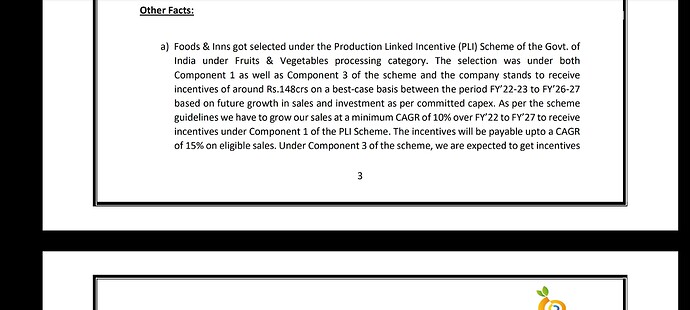

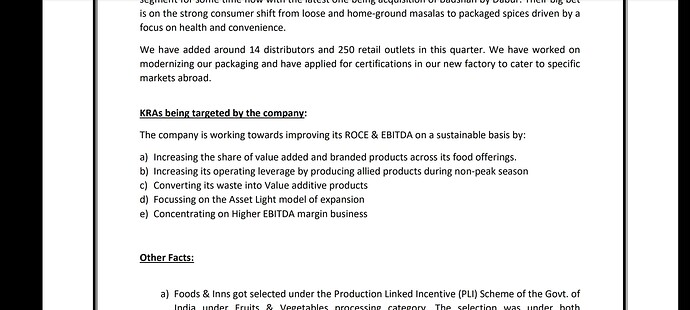

Company does not have pricing power as competition and that’s why margin is in 8-9% in last 2-3 years. But in their latest IP they have hinted for margin expansion due to VAP contribution, focusing on asset light model and focusing on non- peak season products.

-

Interestingly in FY23 they have achieved sales of 454CR in 6 months of FY23, this is expected to increase further with more capacity coming up in future.

Edit:

Preferential allotment has done today to non promoter entities

| Subscribe To Our Free Newsletter |