Hi James,

I’ll offer a very high level thesis of Suryoday.

Three things went wrong for them during covid.

- JLG Defaults – They acquire customers and make collections via joint liability group meetings. During covid, they weren’t able to conduct any group meetings. This was made worse by the fact that people within the JLG who defaulted on loans during covid pressured others into not paying.

-

Small collection team – To keep costs low, they ran a small collection team. This was fine when they conducted group meetings, but when the meetings failed, they did not have enough people to chase customers.

-

Concentration in states worked unfavourably – The states with highest exposure had the lowest collection efficiency during the covid recovery.

What’s changed since?

Two of the issues above have been addressed over the last six quarters by completely re-evaluating their collection strategy, and disbursements away from JLG.

Ultimately, the thesis was that if the macro in the MFI sector was good, they’ll be able to make recoveries from their customers, and these have already been written off.

Given that the NPAs were akin to PSU banks, I did not size more than 2-2.5% of my portfolio. When I bought at a share price of 100, it was at 0.7x book. With the market now chasing after various financials, the worst lenders have been the ones to outperform.

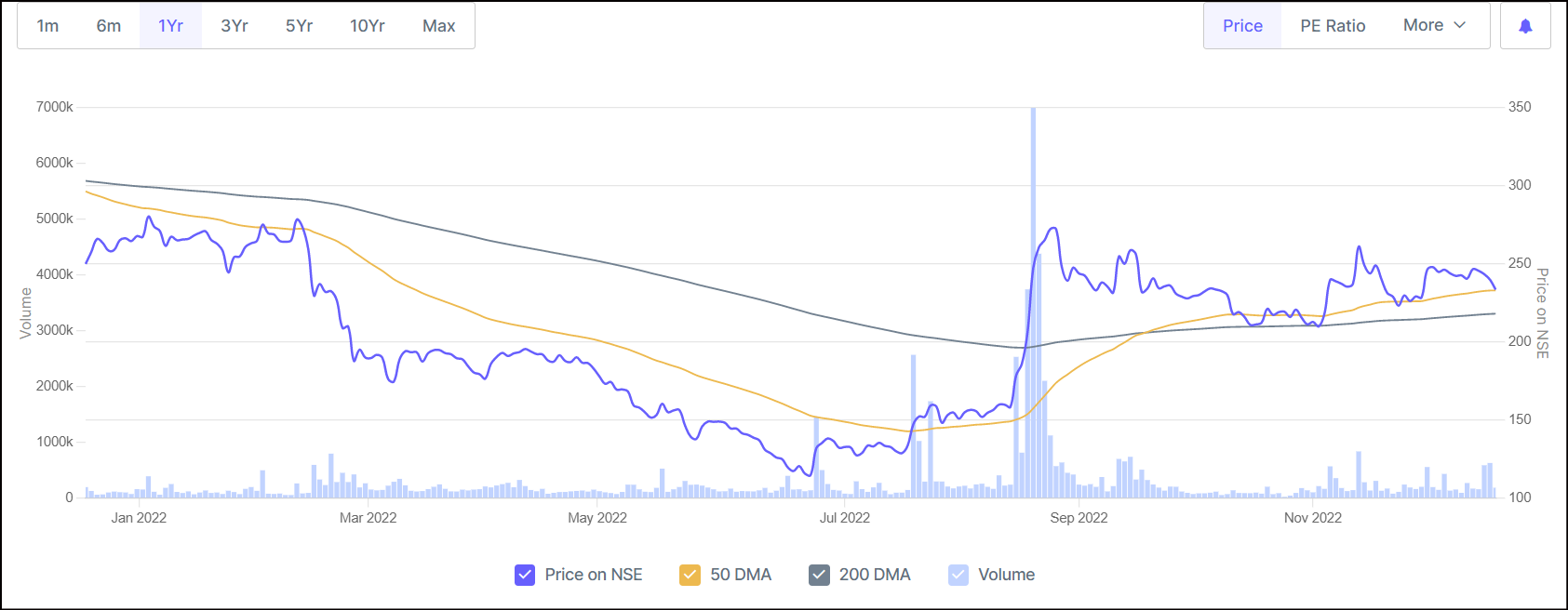

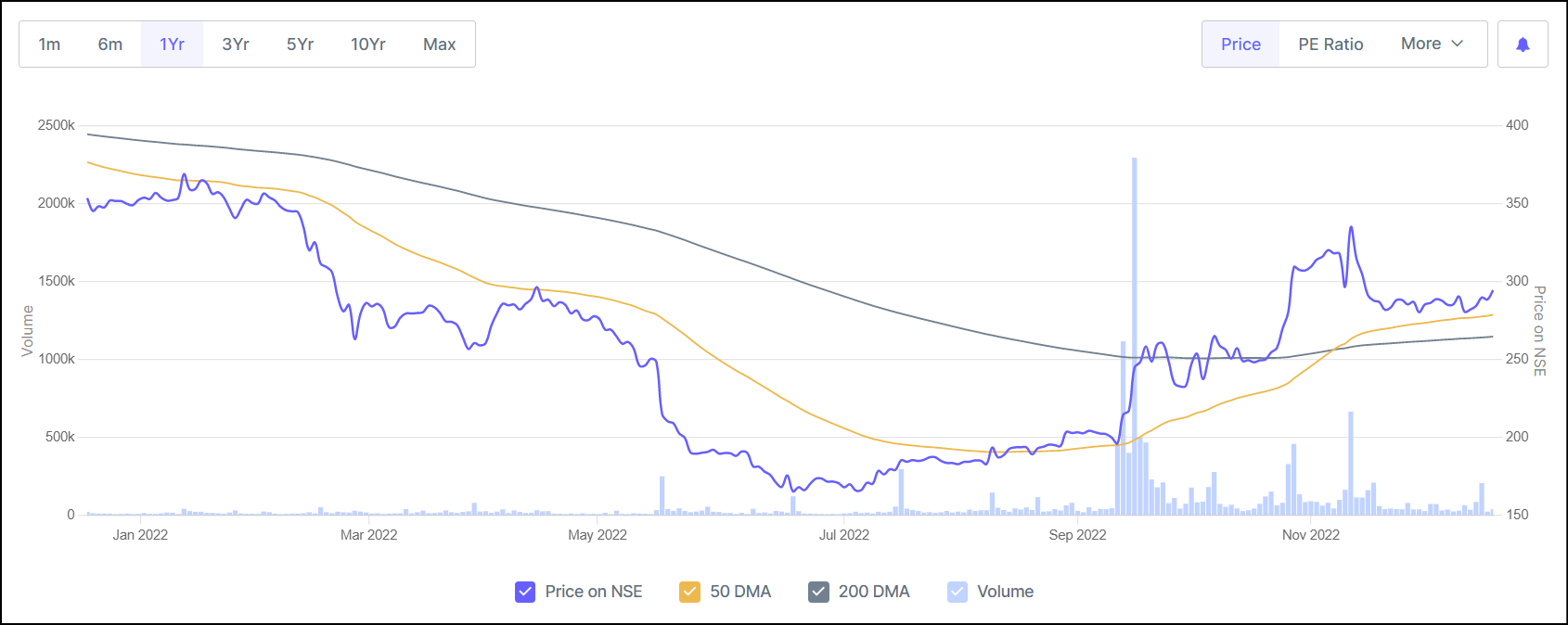

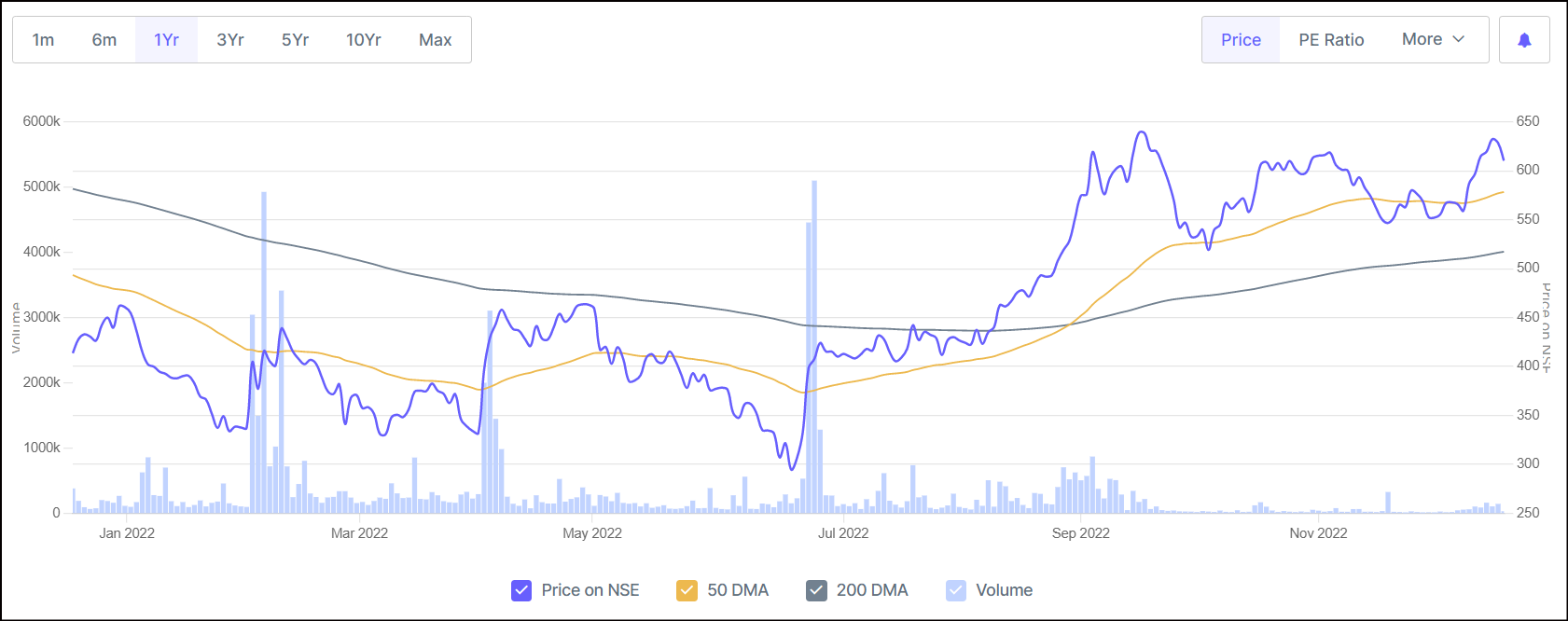

Repco:

Muthoot Capital:

Spandana:

Suryoday was the only one that hadn’t participated in this rally. I sold between 125-130.

I’ve moved my position from Suryoday to CreditAcess. If it falls to 800 or below, I’ll size to 5% of my portfolio.

| Subscribe To Our Free Newsletter |