I have gone through the thread, but one thing I find missing is any mention of some assets which LIC has, which are ignored in our assessment of its value.

As somebody who lives in Delhi, I am familiar with many landmark buildings owned by it in prime of prime area of Delhi. Jeevan Bharti, Jeevan Prakash, Jeevan Tara for example, are located in Connaught Place, Parliament Street, Bikaiji Cama Place, and Nehru Place.

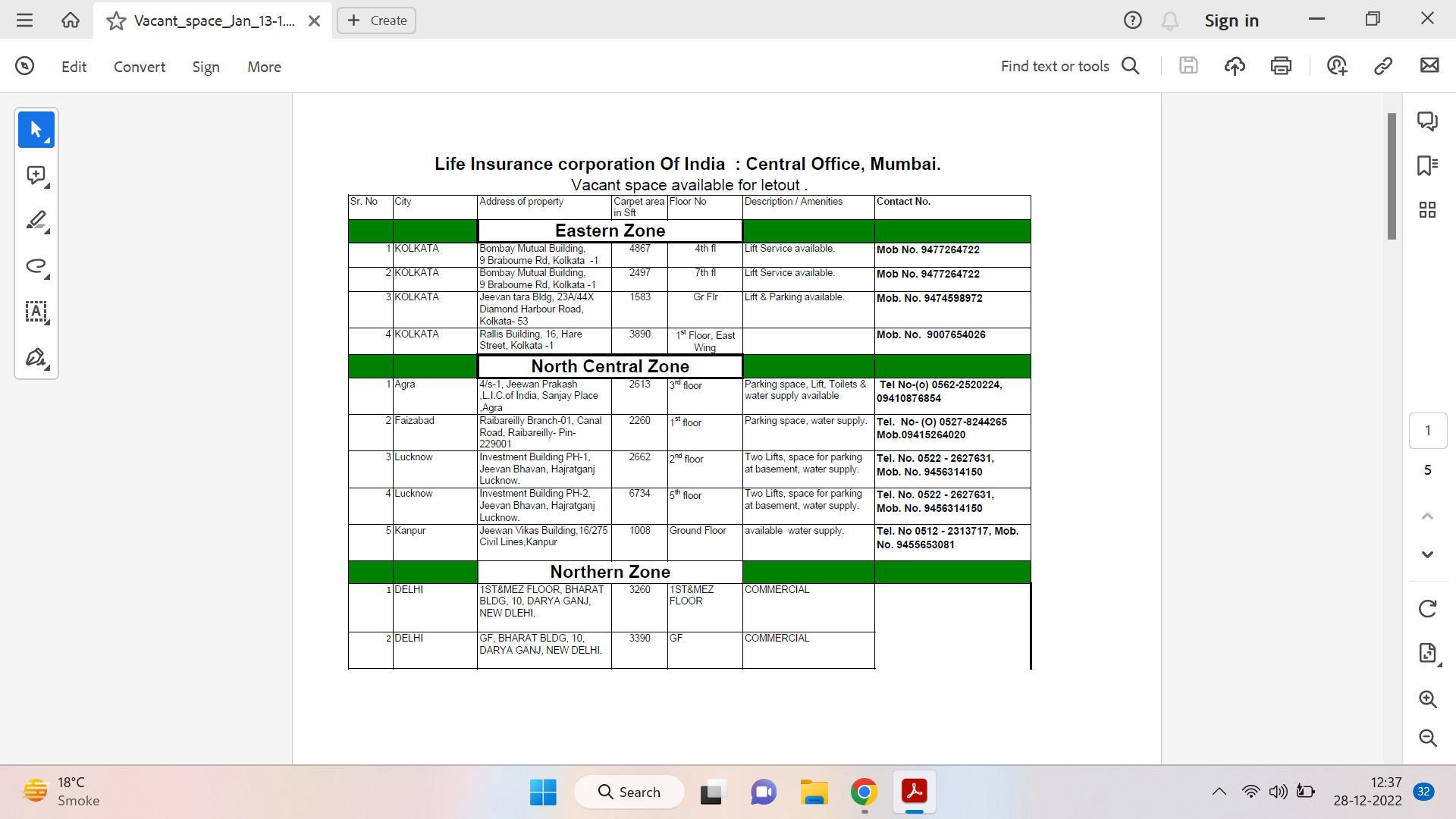

As per the ads put out by LIC, it has buildings not only in Bombay, LIC owns 186 buildings in Mumbai, IPO on track

but in as rather lesser known place like Dholi in Muzaffarpur. They are everywhere, from Srinagar to Portblair.

Bombay needs another mention. It has buildings

Such is the extent of the vast number of buildings they own that even LIC does not have a correct idea of their count.

I have found a very old figure of ₹70,000 crore value put at these buildings.

Many of the buildings were constructed way back in 1950s and 1960s. LIC building in Chennai for example, was the tallest building in Madras of those times. Mind boggles at the multiplication in their value.

Of course, being a PSU, it suffers from the common malaise of inefficiency. This is what have found:

Sources said that the land was purchased to set up an `investment building’ either an IT park or a commercial complex to be rented out. While a large number of the LIC’s old properties are non-performing assets generating rentals of less than Rs 10 per month, new properties are generating decent returns.

Agreeing with LIC’s predicament, a well-known real estate consultant pointed out: “Some of LIC’s existing buildings are lying vacant, for exbut since the buildings are old and lack plug-and-play infrastructure , companies are reluctant to rent them and instead prefer new buildings coming up at Ballygunge, Lower Circular Road and even Salt Lake,” a real estate consultant pointed out.

Currently, LIC owns nearly 1,571 properties in India and some overseas. Of these, some 374-odd LIC real estate portfolios are primarily investment properties. It also has some free-hold lands in metros, a majority of which will be used to house offices or employee families. The surplus may be used to boost the firm’s rental income.

Read more at:

LIC’s turning builder, buys land for commercial development – The Economic Times

In addition, they have paintings, some of them by iconic names like Hussain and Hebbar, bought at throw away prices long back. LIC realised their value only when Hussain wanted to buy them back.

Peter Lynch has this to say in his ‘One up on the Wall Street’:

THE ASSET PLAYS

An asset play is any company that’s sitting on something valuable that you

know about, but that the Wall Street crowd has overlooked. With so many

analysts and corporate raiders snooping around, it doesn’t seem possible that

there are any assets that Wall Street hasn’t noticed, but believe me, there are.

The asset play is where the local edge can be used to greatest advantage.

e asset may be as simple as a pile of cash. Sometimes it’s real estate. I’ve

already mentioned Pebble Beach as a great asset play. Here’s why: At the end of

1976 the stock was selling for 14½ per share, which, with 1.7 million shares

outstanding, meant that the whole company was valued at only $25 million.

Less than three years later (May, 1979), Twentieth Century-Fox bought out

Pebble Beach for $72 million, or 42½ per share. What’s more, a day after

buying the company, Twentieth Century turned around and sold Pebble

Beach’s gravel pit—just one of the company’s many assets—for $30 million. In

other words, the gravel pit alone was worth more than what investors in 1976

paid for the whole company. ose investors got all the adjacent land, the

2,700 acres in Del Monte Forest and the Monterey Peninsula, the 300-year-old

trees, the hotel, and the two golf courses for nothing.

…Hundreds of thousands of California commuters drive by the Newhall

Ranch every day. Insurance appraisers, mortgage bankers, and real estate agents

involved in the various Newhall deals certainly knew of the extent of Newhall’s

holdings and of the general increase in California property values. How many

people owned houses in the areas around the Newhall Ranch and saw the great

escalation in land values, years ahead of any Wall Street analysts? How many of

them considered researching this stock that has been a twenty-bagger from the

early seventies and a fourbagger since 1980? If I’d lived in California, I

wouldn’t have missed it. At least, I hope I wouldn’t have.

…Right now I’m holding on to Liberty Corp., an insurance company whose

TV properties are worth more than the price I paid for the stock. Once you

found out that the TV properties were worth $30 a share, and you saw that the

stock was selling for $30 a share, you could take out your pocket calculator

and subtract $30 from $30. e result was the cost of your investment in a

valuable insurance business—zero.

Was Harshad Mehta right when he talked of replacement value? How much would it cost to build a company like LIC now?

I may be wrong in supposing that the LIC should not be valued for its premia or the investments in stocks but for the large real estate and paintings it holds. Whether it actually monetises them or not may be an issue.

In many cases, its buildings are in bad shape, or in occupation of tenants who pay it a pittance. Government departments for example.

Disclosure: I have a small holding in LIC.

| Subscribe To Our Free Newsletter |