Hi Mudit. Thanks for your interest!

To be honest, I know nothing about PI industry apart from general info which is available everywhere.

My conviction with UPL is due to the international business they have built and slowly increasing their hold in South America wherein just like India, farming is a primary source of income. UPL is a multinational agrochem global brand. (I believe one of the top5 in the world from revenue perspective). Their focus is primarily on Crop Protection solutions and is a technology-driven company. They have many subsidiaries and a very complex corp structure but the growth trajectory from company perspective is poised for good.

The real concern is increasing debt and I have somewhat low confidence in mgmt specially Shroff and family. You know there is something fishy when the promoters are buying yacht through companies in British virgin islands and acquiring real estate in dubai through nested subsidiaries (Src: Pandora Papers).

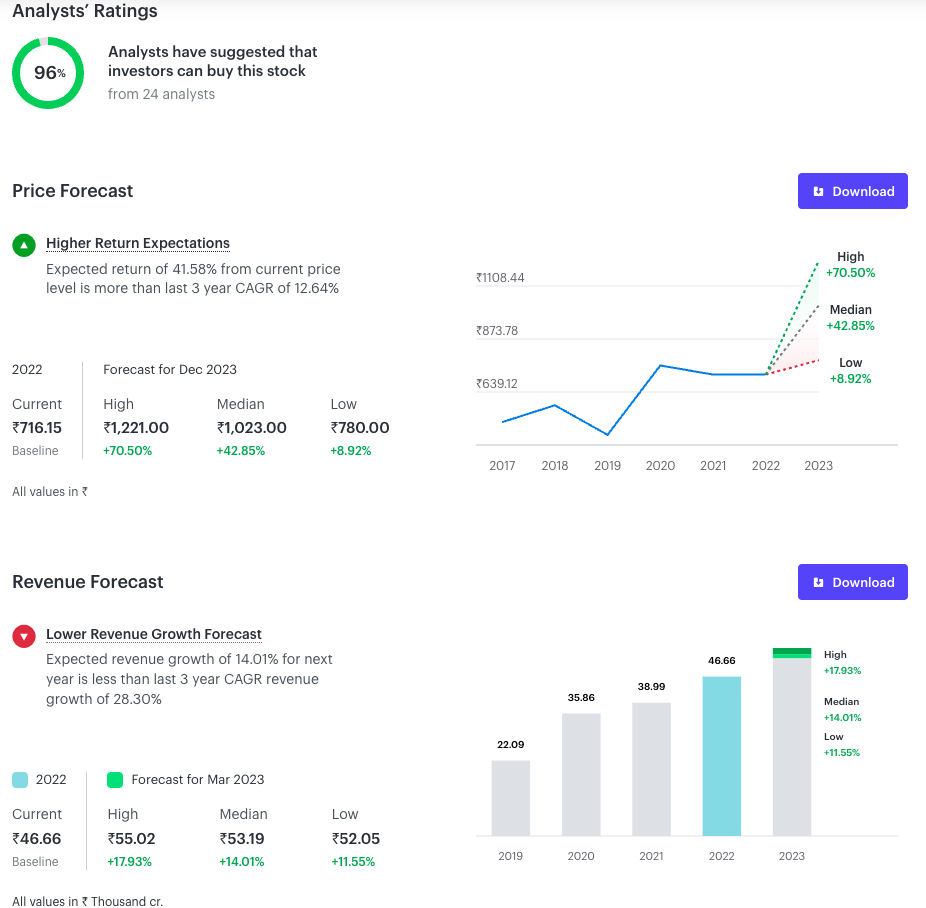

Overall, the above has not affected the company so far and they have above avg dividend payout. Some info from ticker tape for your consideration.

In case anyone has read the latest concal transcripts, plz elaborate what was mgmt narrative on reducing the debt. Thank You!

| Subscribe To Our Free Newsletter |